Citibank 2012 Annual Report Download - page 129

Download and view the complete annual report

Please find page 129 of the 2012 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

|

|

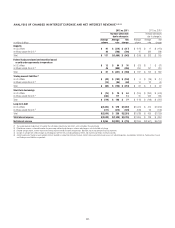

107

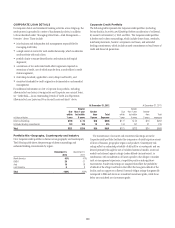

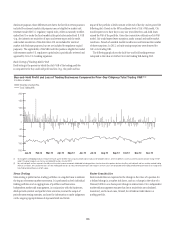

Average Rates

-

Interest Revenue, Interest Expense and Net Interest Margin

INTEREST REVENUE/EXPENSE AND YIELDS

Interest Revenue-Average Rate

Interest Expense-Average Rate

Net Interest Margin

1.34%

1.43%

1.51%

1.57%

1.59%

1.62%

1.69%

1.62%

1.60%

1.62%1.61%1.61%

3.32%

4.76% 4.59% 4.50% 4.36% 4.31% 4.29% 4.23% 4.26% 4.23% 4.07% 4.05% 4.04%

3.15% 3.06% 2.95% 2.88% 2.82% 2.83% 2.90% 2.90% 2.81% 2.86% 2.93%

1Q10 2Q10

2010: 3.12%

2011: 2.86% 2012: 2.88%

3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

5.50%

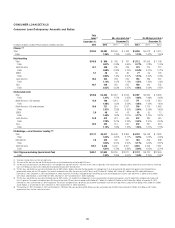

In millions of dollars, except as otherwise noted 2012 2011 2010

Change

2012 vs. 2011

Change

2011 vs. 2010

Interest revenue (1) $68,680 $73,201 $79,801 (6)% (8)%

Interest expense (2) 20,484 24,229 25,096 (15) (3)

Net interest revenue (3) $48,196 $48,972 $54,705 (2)% (10)%

Interest revenue—average rate 4.10% 4.27% 4.55% (17 ) bps (28) bps

Interest expense—average rate 1.46 1.63 1.61 (17) bps 2 bps

Net interest margin 2.88 2.86 3.12 2 bps (26) bps

Interest-rate benchmarks

Two-year U.S. Treasury note—average rate 0.28% 0.45% 0.70% (17) bps (25) bps

10-year U.S. Treasury note—average rate 1.80 2.78 3.21 (98) bps (43) bps

10-year vs. two-year spread 152 bps 233 bps 251 bps

(1) Interest revenue includes the taxable equivalent adjustments (based on the U.S. federal statutory tax rate of 35%) of $542 million, $520 million, and $519 million for 2012, 2011 and 2010, respectively.

(2) Interest expense includes the taxable equivalent adjustments (based on the U.S. federal statutory tax rate of 35%) of $51 million, $5 million and $0 million for 2012, 2011 and 2010, respectively.

(3) Excludes expenses associated with certain hybrid financial instruments. These obligations are classified as Long-term debt and accounted for at fair value with changes recorded in Principal transactions.

A significant portion of Citi’s business activities are based upon gathering

deposits and borrowing money and then lending or investing those funds,

or participating in market-making activities in tradable securities. Citi’s net

interest margin (NIM) is calculated by dividing gross interest revenue less

gross interest expense by average interest earning assets.

During 2012, Citi’s NIM remained relatively stable as compared to the

prior year at 288 basis points. Citi continued to experience pressure on its

loan and investment portfolio yields reflecting the low rate environment. In

aggregate, this pressure negatively impacted NIM by approximately 17 basis

points in 2012 versus the prior year. Ongoing pressure from the low rate

environment was offset by the pay-downs of higher-cost long-term debt and

redemptions of trust preferred securities during the year, which positively

impacted NIM by approximately 10 basis points in 2012. In addition, as

discussed under “Capital Resources and Liquidity—Funding and Liquidity”

above, during 2012, Citi reduced its deposit funding costs, partially through

increasing the share of non-interest bearing deposits, which contributed

approximately 10 basis points of NIM benefit in 2012. Decreased deposit costs

and lower outstanding long-term debt, as well as an increase in Citi’s trading

book portfolio yields, contributed to the increase in NIM quarter-over-quarter.

Absent any significant changes or events, Citi expects its NIM will likely

continue to reflect the pressure of a low interest rate environment and

subsequent changes in its portfolios, including its trading book portfolio,

although continued improvement in Citi’s cost of funds and lower levels of

outstanding long-term debt will both continue to positively impact NIM. As

such, Citi currently believes that its 2013 NIM should be relatively stable to its

full-year 2012 level, with some quarterly fluctuations.