Citibank 2012 Annual Report Download - page 109

Download and view the complete annual report

Please find page 109 of the 2012 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

|

|

87

Moreover, Citi’s servicing agreements associated with its sales of mortgage

loans to the GSEs generally provide the GSEs with a high level of servicing

oversight, including, among other things, timelines in which foreclosures

or modification activities are to be completed. The agreements allow for the

GSEs to take action against a servicer for violation of the timelines, which

includes imposing compensatory fees. While the GSEs have not historically

exercised their rights to impose compensatory fees, they have begun to do so

on a regular basis. To date, the imposition of compensatory fees, as a result

of the extended foreclosure timelines or otherwise, has not had a material

impact on Citi.

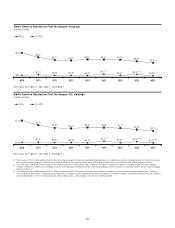

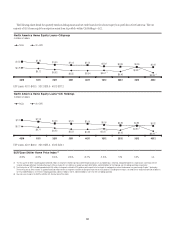

North America Consumer Mortgage Quarterly Credit Trends—

Delinquencies and Net Credit Losses—Home Equity Loans

Citi’s home equity loan portfolio consists of both fixed-rate home equity

loans and loans extended under home equity lines of credit. Fixed-rate

home equity loans are fully amortizing. Home equity lines of credit allow

for amounts to be drawn for a period of time with the payment of interest

only and then, at the end of the draw period, the then-outstanding amount

is converted to an amortizing loan (the interest-only payment feature during

the revolving period is standard for this product across the industry). Prior

to June 2010, Citi’s originations of home equity lines of credit typically had

a 10-year draw period. Beginning in June 2010, Citi’s originations of home

equity lines of credit typically have a five-year draw period as Citi changed

these terms to mitigate risk. After conversion, the home equity loans typically

have a 20-year amortization period.

As of December 31, 2012, Citi’s home equity loan portfolio of $37.2 billion

included approximately $22.0 billion of home equity lines of credit that are

still within their revolving period and have not commenced amortization, or

“reset.” During the period 2009–2012, approximately only 3% of Citi’s home

equity loan portfolio commenced amortization; approximately 75% of Citi’s

home equity loans extended under lines of credit as of December 31, 2012

will contractually begin to amortize during the period 2015–2017. Based

on this limited sample of home equity loans that has begun amortization,

Citi has experienced marginally higher delinquency rates in its amortizing

home equity loan portfolio as compared to its non-amortizing loan portfolio.

However, these resets have occurred during a period of declining interest

rates, which Citi believes has likely reduced the overall “payment shock” to

the borrower. Citi will continue to monitor this reset risk closely, particularly

as it approaches 2015, and Citi will continue to consider the impact in

determining its allowance for loan loss reserves accordingly. In addition,

management is reviewing additional actions to offset potential reset risk,

such as extending offers to non-amortizing home equity loan borrowers to

convert the non-amortizing home equity loan to a fixed-rate loan.

As of December 31, 2012, the percentage of U.S. home equity loans in

a junior lien position where Citi also owned or serviced the first lien was

approximately 30%. However, for all home equity loans (regardless of

whether Citi owns or services the first lien), Citi manages its home equity

loan account strategy through obtaining and reviewing refreshed credit

bureau scores (which reflect the borrower’s performance on all of its debts,

including a first lien, if any), refreshed LTV ratios and other borrower credit-

related information. Historically, the default and delinquency statistics for

junior liens where Citi also owns or services the first lien have been better

than for those where Citi does not own or service the first lien. Citi believes

this is generally attributable to origination channels and better credit

characteristics of the portfolio, including FICO and LTV, for those junior liens

where Citi also owns or services the first lien.