Citibank 2012 Annual Report Download - page 145

Download and view the complete annual report

Please find page 145 of the 2012 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

|

|

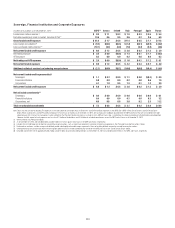

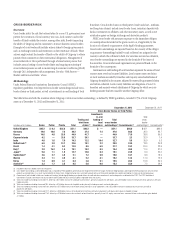

123

FAIR VALUE ADJUSTMENTS FOR DERIVATIVES AND STRUCTURED DEBT

The following discussion relates to the derivative obligor information and

the fair valuation for derivatives and structured debt. See Note 23 to the

Consolidated Financial Statements for additional information on Citi’s

derivative activities.

Fair Valuation Adjustments for Derivatives

The fair value adjustments applied by Citigroup to its derivative carrying

values consist of the following items:

• Liquidity adjustments are applied to items in Level 2 or Level 3 of the fair-

value hierarchy (see Note 25 to the Consolidated Financial Statements

for more details) to ensure that the fair value reflects the price at which

the net open risk position could be liquidated. The liquidity reserve is

based on the bid/offer spread for an instrument. When Citi has elected to

measure certain portfolios of financial investments, such as derivatives,

on the basis of the net open risk position, the liquidity reserve is adjusted

to take into account the size of the position.

• Credit valuation adjustments (CVA) are applied to over-the-counter

derivative instruments, in which the base valuation generally discounts

expected cash flows using the relevant base interest rate curves. Because

not all counterparties have the same credit risk as that implied by the

relevant base curve, a CVA is necessary to incorporate the market view of

both counterparty credit risk and Citi’s own credit risk in the valuation.

Citi’s CVA methodology is composed of two steps. First, the exposure

profile for each counterparty is determined using the terms of all individual

derivative positions and a Monte Carlo simulation or other quantitative

analysis to generate a series of expected cash flows at future points in time.

The calculation of this exposure profile considers the effect of credit risk

mitigants, including pledged cash or other collateral and any legal right

of offset that exists with a counterparty through arrangements such as

netting agreements. Individual derivative contracts that are subject to an

enforceable master netting agreement with a counterparty are aggregated

for this purpose, since it is those aggregate net cash flows that are subject to

nonperformance risk. This process identifies specific, point-in-time future

cash flows that are subject to nonperformance risk, rather than using the

current recognized net asset or liability as a basis to measure the CVA.

Second, market-based views of default probabilities derived from

observed credit spreads in the credit default swap (CDS) market are applied

to the expected future cash flows determined in step one. Citi’s own-credit

CVA is determined using Citi-specific CDS spreads for the relevant tenor.

Generally, counterparty CVA is determined using CDS spread indices for each

credit rating and tenor. For certain identified netting sets where individual

analysis is practicable (e.g., exposures to counterparties with liquid CDS),

counterparty-specific CDS spreads are used.

The CVA adjustment is designed to incorporate a market view of the credit

risk inherent in the derivative portfolio. However, most derivative instruments

are negotiated bilateral contracts and are not commonly transferred to

third parties. Derivative instruments are normally settled contractually or, if

terminated early, are terminated at a value negotiated bilaterally between the

counterparties. Therefore, the CVA (both counterparty and own-credit) may

not be realized upon a settlement or termination in the normal course of

business. In addition, all or a portion of the CVA may be reversed or otherwise

adjusted in future periods in the event of changes in the credit risk of Citi or

its counterparties, or changes in the credit mitigants (collateral and netting

agreements) associated with the derivative instruments.

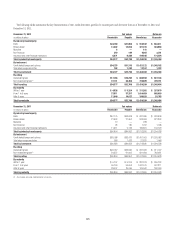

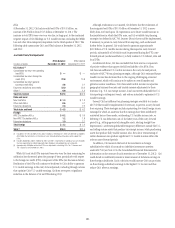

The table below summarizes the CVA applied to the fair value of derivative

instruments for the periods indicated:

Credit valuation adjustment

contra-liability (contra-asset)

In millions of dollars

December 31,

2012

December 31,

2011

Non-monoline counterparties $(2,971) $(5,392)

Citigroup (own) 918 2,176

Total CVA—derivative instruments $(2,053) $(3,216)

Own Debt Valuation Adjustments for Structured Debt

Own debt valuation adjustments (DVA) are recognized on Citi’s debt

liabilities for which the fair value option (FVO) has been elected using Citi’s

credit spreads observed in the bond market. Accordingly, the fair value of debt

liabilities for which the fair value option has been elected (other than non-

recourse and similar liabilities) is impacted by the narrowing or widening of

Citi’s credit spreads. Changes in fair value resulting from changes in Citi’s

instrument-specific credit risk are estimated by incorporating Citi’s current

credit spreads observable in the bond market into the relevant valuation

technique used to value each liability.

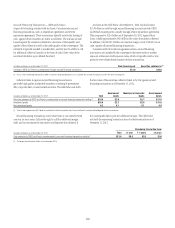

The table below summarizes pretax gains (losses) related to changes in

CVA on derivative instruments, net of hedges, and DVA on own FVO debt for

the periods indicated:

Credit/debt valuation

adjustment gain

(loss)

In millions of dollars 2012 2011

Derivative counterparty CVA, excluding monolines $ 805 $ (830)

Derivative own-credit CVA (1,126) 863

Total CVA—derivative instruments (1) $ (321) $ 33

DVA related to own FVO debt $(2,009) $1,773

Total CVA and DVA excluding monolines $(2,330) $1,806

CVA related to monoline counterparties 2179

Total CVA and DVA $(2,328) $1,985

(1) Net of hedges

The CVA and DVA amounts shown in the table above do not include the

effect of counterparty credit risk embedded in non-derivative instruments.

Losses on non-derivative instruments, such as bonds and loans, related to

counterparty credit risk are also not included in the table above.