Citibank 2012 Annual Report Download - page 230

Download and view the complete annual report

Please find page 230 of the 2012 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

|

|

208

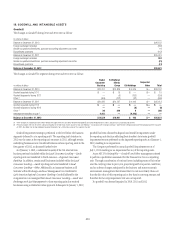

Citigroup has a risk management process to monitor, evaluate and

manage the principal risks associated with its Corporate loan portfolio. As

part of its risk management process, Citi assigns numeric risk ratings to its

Corporate loan facilities based on quantitative and qualitative assessments

of the obligor and facility. These risk ratings are reviewed at least annually

or more often if material events related to the obligor or facility warrant.

Factors considered in assigning the risk ratings include: financial condition

of the obligor, qualitative assessment of management and strategy, amount

and sources of repayment, amount and type of collateral and guarantee

arrangements, amount and type of any contingencies associated with the

obligor, and the obligor’s industry and geography.

The obligor risk ratings are defined by ranges of default probabilities. The

facility risk ratings are defined by ranges of loss norms, which are the product

of the probability of default and the loss given default. The investment grade

rating categories are similar to the category BBB-/Baa3 and above as defined

by S&P and Moody’s. Loans classified according to the bank regulatory

definitions as special mention, substandard and doubtful will have risk

ratings within the non-investment grade categories.

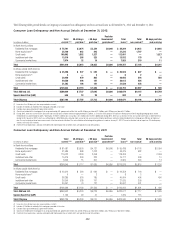

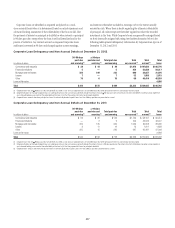

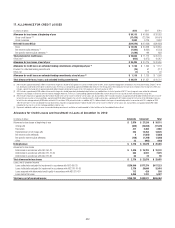

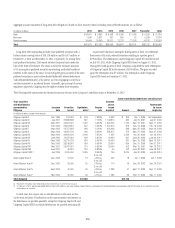

Corporate Loans Credit Quality Indicators at

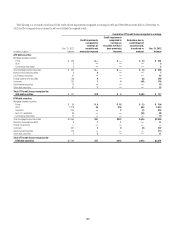

December 31, 2012 and December 31, 2011

Recorded investment in loans (1)

In millions of dollars

December 31,

2012

December 31,

2011

Investment grade (2)

Commercial and industrial $ 73,822 $ 67,282

Financial institutions 43,895 35,159

Mortgage and real estate 12,587 10,729

Leases 1,404 1,161

Other 42,575 42,428

Total investment grade $174,283 $156,759

Non-investment grade (2)

Accrual

Commercial and industrial $ 33,876 $ 30,998

Financial institutions 9,968 7,485

Mortgage and real estate 2,858 3,812

Leases 559 664

Other 3,915 4,293

Non-accrual

Commercial and industrial 1,078 1,134

Financial institutions 454 763

Mortgage and real estate 680 1,039

Leases 52 13

Other 69 287

Total non-investment grade $ 53,509 $ 50,488

Private Banking loans managed on a

delinquency basis (2) $ 14,945 $ 12,716

Loans at fair value 4,056 3,939

Corporate loans, net of unearned income $246,793 $223,902

(1) Recorded investment in a loan includes net deferred loan fees and costs, unamortized premium or

discount, less any direct write-downs.

(2) Held-for-investment loans accounted for on an amortized cost basis.

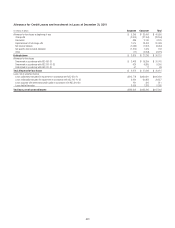

Corporate loans and leases identified as impaired and placed on

non-accrual status are written down to the extent that principal is judged

to be uncollectible. Impaired collateral-dependent loans and leases, where

repayment is expected to be provided solely by the sale of the underlying

collateral and there are no other available and reliable sources of repayment,

are written down to the lower of cost or collateral value, less cost to sell.

Cash-basis loans are returned to an accrual status when all contractual

principal and interest amounts are reasonably assured of repayment and

there is a sustained period of repayment performance, generally six months,

in accordance with the contractual terms of the loan.