Citibank 2012 Annual Report Download - page 297

Download and view the complete annual report

Please find page 297 of the 2012 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

287 -

288

288 -

289

289 -

290

290 -

291

291 -

292

292 -

293

293 -

294

294 -

295

295 -

296

296 -

297

297 -

298

298 -

299

299 -

300

300 -

301

301 -

302

302 -

303

303 -

304

304 -

305

305 -

306

306 -

307

307 -

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

|

|

275

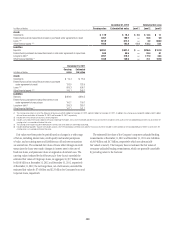

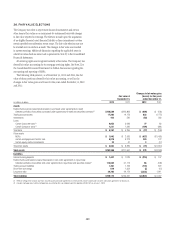

Maximum potential amount of future payments

In billions of dollars at December 31, 2011 except carrying value in millions

Expire within

1 year

Expire after

1 year

Total amount

outstanding

Carrying value

(in millions of dollars)

Financial standby letters of credit $ 25.2 $ 79.5 $ 104.7 $ 417.5

Performance guarantees 7.8 4.5 12.3 43.9

Derivative instruments considered to be guarantees 9.8 40.0 49.8 2,686.1

Loans sold with recourse — 0.4 0.4 89.6

Securities lending indemnifications (1) 90.9 — 90.9 —

Credit card merchant processing (1) 70.2 — 70.2 —

Custody indemnifications and other — 40.0 40.0 30.7

Total $ 203.9 $ 164.4 $ 368.3 $ 3,267.8

(1) The carrying values of securities lending indemnifications and credit card merchant processing are not material, as the Company has determined that the amount and probability of potential liabilities arising from these

guarantees are not significant.

Financial standby letters of credit

Citigroup issues standby letters of credit which substitute its own credit

for that of the borrower. If a letter of credit is drawn down, the borrower is

obligated to repay Citigroup. Standby letters of credit protect a third party

from defaults on contractual obligations. Financial standby letters of credit

include guarantees of payment of insurance premiums and reinsurance risks

that support industrial revenue bond underwriting and settlement of payment

obligations to clearing houses, and also support options and purchases of

securities or are in lieu of escrow deposit accounts. Financial standbys also

backstop loans, credit facilities, promissory notes and trade acceptances.

Performance guarantees

Performance guarantees and letters of credit are issued to guarantee a

customer’s tender bid on a construction or systems-installation project or to

guarantee completion of such projects in accordance with contract terms.

They are also issued to support a customer’s obligation to supply specified

products, commodities, or maintenance or warranty services to a third party.

Derivative instruments considered to be guarantees

Derivatives are financial instruments whose cash flows are based on a

notional amount and an underlying instrument, where there is little or

no initial investment, and whose terms require or permit net settlement.

Derivatives may be used for a variety of reasons, including risk management,

or to enhance returns. Financial institutions often act as intermediaries for

their clients, helping clients reduce their risks. However, derivatives may also

be used to take a risk position.

The derivative instruments considered to be guarantees, which are

presented in the tables above, include only those instruments that require Citi

to make payments to the counterparty based on changes in an underlying

instrument that is related to an asset, a liability, or an equity security held by

the guaranteed party. More specifically, derivative instruments considered to

be guarantees include certain over-the-counter written put options where the

counterparty is not a bank, hedge fund or broker-dealer (such counterparties

are considered to be dealers in these markets and may, therefore, not hold

the underlying instruments). However, credit derivatives sold by the Company

are excluded from the tables above as they are disclosed separately in Note 23

to the Consolidated Financial Statements. In addition, non-credit derivative

contracts that are cash settled and for which the Company is unable to assert

that it is probable the counterparty held the underlying instrument at the

inception of the contract also are excluded from the tables above.

In instances where the Company’s maximum potential future payment is

unlimited, the notional amount of the contract is disclosed.

Loans sold with recourse

Loans sold with recourse represent the Company’s obligations to reimburse

the buyers for loan losses under certain circumstances. Recourse refers to the

clause in a sales agreement under which a lender will fully reimburse the

buyer/investor for any losses resulting from the purchased loans. This may be

accomplished by the seller taking back any loans that become delinquent.

In addition to the amounts shown in the tables above, Citi has recorded

a mortgage repurchase reserve for its potential repurchases or make-whole

liability regarding representation and warranty claims. The repurchase

reserve was $1,565 million and $1,188 million at December 31, 2012 and

December 31, 2011, respectively, and these amounts are included in Other

liabilities on the Consolidated Balance Sheet.

Repurchase Reserve—Whole Loan Sales

The repurchase reserve estimation process for potential residential mortgage

whole loan representation and warranty claims is based on various

assumptions which are primarily based on Citi’s historical repurchase

activity with the GSEs. The assumptions used to calculate this repurchase

reserve include numerous estimates and judgments and thus contain a level

of uncertainty and risk that, if different from actual results, could have a

material impact on the reserve amounts.

As of December 31, 2012, Citi estimates that the range of reasonably

possible loss for whole loan sale representation and warranty claims in excess

of amounts accrued could be up to $0.6 billion. This estimate was derived

by modifying the key assumptions discussed above to reflect management’s

judgment regarding reasonably possible adverse changes to those

assumptions. Citi’s estimate of reasonably possible loss is based on currently

available information, significant judgment and numerous assumptions that

are subject to change.