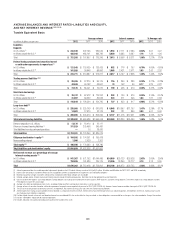

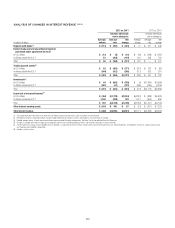

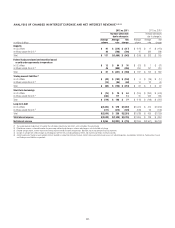

Citibank 2012 Annual Report Download - page 141

Download and view the complete annual report

Please find page 141 of the 2012 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

|

|

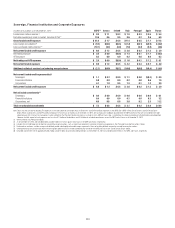

119

Redenomination and Devaluation Risk

As referenced above, the ongoing Eurozone debt crisis and other

developments in the European Monetary Union (EMU) could lead to the

withdrawal of one or more countries from the EMU or a partial or complete

break-up of the EMU. See also “Risk Factors—Market and Economic Risks.”

If one or more countries were to leave the EMU, certain obligations relating

to the exiting country could be redenominated from the Euro to a new

country currency. While alternative scenarios could develop, redenomination

could be accompanied by immediate devaluation of the new currency as

compared to the Euro and the U.S. dollar.

Citi, like other financial institutions with substantial operations in

the EMU, is exposed to potential redenomination and devaluation risks

arising from (i) Euro-denominated assets and/or liabilities located or held

within the exiting country that are governed by local country law (“local

exposures”), as well as (ii) other Euro-denominated assets and liabilities,

such as loans, securitized products or derivatives, between entities outside of

the exiting country and a client within the country that are governed by local

country law (“offshore exposures”). However, the actual assets and liabilities

that could be subject to redenomination and devaluation risk are subject to

substantial legal and other uncertainty.

Citi has been, and will continue to be, engaged in contingency planning

for such events, particularly with respect to Greece, Ireland, Italy, Portugal

and Spain. Generally, to the extent that Citi’s local and offshore assets

are approximately equal to its liabilities within the exiting country, and

assuming both assets and liabilities are symmetrically redenominated and

devalued, Citi believes that its risk of loss as a result of a redenomination

and devaluation event would not be material. However, to the extent its local

and offshore assets and liabilities are not equal, or there is asymmetrical

redenomination of assets versus liabilities, Citi could be exposed to losses

in the event of a redenomination and devaluation. Moreover, a number of

events that could accompany a redenomination and devaluation, including

a drawdown of unfunded commitments or “deposit flight,” could exacerbate

any mismatch of assets and liabilities within the exiting country.

Citi’s redenomination and devaluation exposures to the GIIPS as of

December 31, 2012 are not additive to its credit risk exposures to such

countries as described under “Credit Risk” above. Rather, Citi’s credit risk

exposures in the affected country would generally be reduced to the extent of

any redenomination and devaluation of assets.

As of December 31, 2012, Citi estimates that it had net asset exposure

subject to redenomination and devaluation in Italy, principally relating to

derivatives contracts. Citi also estimates that, as of such date, it had net asset

exposure subject to redenomination and devaluation in Spain, principally

related to offshore exposures related to held-to-maturity securitized retail

assets (primarily mortgage-backed securities) and exposures to Private Bank

customers (see “GIIPS—Retail, Small Business and Citi Private Bank”

above). However, as of December 31, 2012, Citi’s estimated redenomination

and devaluation exposure to Italy was less than Citi’s net current funded

credit exposure to Italy (before purchased credit protection) as reflected

under “Credit Risk” above. Further, as of December 31, 2012, Citi’s estimated

redenomination and devaluation exposure to Spain was less than Citi’s net

current funded credit exposure to Spain (before purchased credit protection),

as reflected under “Credit Risk” above. As of December 31, 2012, Citi had a

net liability position in each of Greece, Ireland and Portugal.

As referenced above, Citi’s estimated redenomination and devaluation

exposure does not include purchased credit protection. As described under

“Credit Risk” above, Citi has purchased credit protection primarily from

investment grade, global financial institutions predominantly outside of

the GIIPS. To the extent the purchased credit protection is available in

a redenomination/devaluation event, any redenomination/devaluation

exposure could be reduced.

Any estimates of redenomination/devaluation exposure are subject to

ongoing review and necessarily involve numerous assumptions, including

which assets and liabilities would be subject to redenomination in any given

case, the availability of purchased credit protection and the extent of any

utilization of unfunded commitments, each as referenced above. In addition,

other events outside of Citi’s control— such as the extent of any deposit

flight and devaluation, the imposition of exchange and/or capital controls,

the requirement by U.S. regulators of mandatory loan loss and other reserve

requirements or any required timing of functional currency changes and

the accounting impact thereof —could further negatively impact Citi in

such an event. Accordingly, in an actual redenomination and devaluation

scenario, Citi’s exposures could vary considerably based on the specific facts

and circumstances.