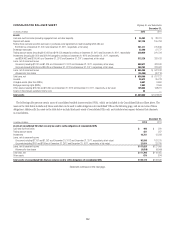

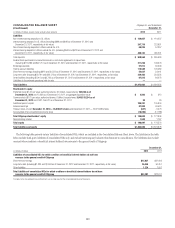

Citibank 2012 Annual Report Download - page 174

Download and view the complete annual report

Please find page 174 of the 2012 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

|

|

152

Statistically calculated losses inherent in the classifiably managed

portfolio for performing and de minimis non-performing exposures.

The calculation is based upon: (i) Citigroup’s internal system of credit-risk

ratings, which are analogous to the risk ratings of the major rating agencies;

and (ii) historical default and loss data, including rating agency information

regarding default rates from 1983 to 2010 and internal data dating to the

early 1970s on severity of losses in the event of default. Adjustments may

be made to this data. Such adjustments include: (i) statistically calculated

estimates to cover the historical fluctuation of the default rates over the credit

cycle, the historical variability of loss severity among defaulted loans, and the

degree to which there are large obligor concentrations in the global portfolio;

and (ii) adjustments made for specific known items, such as current

environmental factors and credit trends.

In addition, representatives from each of the risk management and

finance staffs that cover business areas with delinquency-managed portfolios

containing smaller-balance homogeneous loans present their recommended

reserve balances based upon leading credit indicators, including loan

delinquencies and changes in portfolio size as well as economic trends,

including current and future housing prices, unemployment, length of time

in foreclosure, costs to sell and GDP. This methodology is applied separately

for each individual product within each geographic region in which these

portfolios exist.

This evaluation process is subject to numerous estimates and judgments.

The frequency of default, risk ratings, loss recovery rates, the size and

diversity of individual large credits, and the ability of borrowers with foreign

currency obligations to obtain the foreign currency necessary for orderly debt

servicing, among other things, are all taken into account during this review.

Changes in these estimates could have a direct impact on the credit costs in

any period and could result in a change in the allowance.

Allowance for Unfunded Lending Commitments

A similar approach to the allowance for loan losses is used for calculating

a reserve for the expected losses related to unfunded loan commitments

and standby letters of credit. This reserve is classified on the balance

sheet in Other liabilities. Changes to the allowance for unfunded

lending commitments are recorded in the Provision for unfunded

lending commitments.

Mortgage Servicing Rights

Mortgage servicing rights (MSRs) are recognized as intangible assets

when purchased or when the Company sells or securitizes loans acquired

through purchase or origination and retains the right to service the loans.

Mortgage servicing rights are accounted for at fair value, with changes in

value recorded in Other revenue in the Company’s Consolidated Statement

of Income.

Additional information on the Company’s MSRs can be found in Note 22

to the Consolidated Financial Statements.

Citigroup Residential Mortgages—Representations

and Warranties

Overview

In connection with Citi’s sales of residential mortgage loans to the U.S.

government-sponsored entities (GSEs) and, in most cases, other mortgage

loan sales and private-label securitizations, Citi makes representations

and warranties that the loans sold meet certain requirements. The specific

representations and warranties made by Citi in any particular transaction

depend on, among other things, the nature of the transaction and the

requirements of the investor (e.g., whole loan sale to the GSEs versus loans

sold through securitization transactions), as well as the credit quality of the

loan (e.g., prime, Alt-A or subprime).

These sales expose Citi to potential claims for breaches of its

representations and warranties. In the event of a breach of its representations

and warranties, Citi could be required either to repurchase the mortgage

loans with the identified defects (generally at unpaid principal balance plus

accrued interest) or to indemnify (make-whole) the investors for their losses

on these loans. To the extent Citi made representation and warranties on

loans it purchased from third-party sellers that remain financially viable,

Citi may have the right to seek recovery of repurchase losses or make-whole

payments from the third party based on representations and warranties made

by the third party to Citi (a back-to-back claim).

Whole Loan Sales

Citi is exposed to representation and warranty repurchase claims primarily

as a result of its whole loan sales to the GSEs and, to a lesser extent, private

investors, through its Consumer business in CitiMortgage. When selling a

loan to these investors, Citi makes various representations and warranties to,

among other things, the following:

• Citi’s ownership of the loan;

• the validity of the lien securing the loan;

• the absence of delinquent taxes or liens against the property securing

the loan;

• the effectiveness of title insurance on the property securing the loan;

• the process used in selecting the loans for inclusion in a transaction;

• the loan’s compliance with any applicable loan criteria established by the

buyer; and

• the loan’s compliance with applicable local, state and federal laws.

In the case of a repurchase, Citi will bear any subsequent credit loss on the

mortgage loan and the loan is typically considered a credit-impaired loan

and accounted for under SOP 03-3, “Accounting for Certain Loans and

Debt Securities Acquired in a Transfer” (now incorporated into ASC 310-30,

Receivables—Loans and Debt Securities Acquired with Deteriorated

Credit Quality) (SOP 03-3). These repurchases have not had a material

impact on Citi’s non-performing loan statistics because credit-impaired

purchased SOP 03-3 loans are not included in non-accrual loans, since they

generally continue to accrue interest until write-off. Citi’s repurchases have

primarily been due to GSE repurchase claims.