Citibank 2009 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2009 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

81

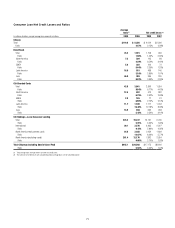

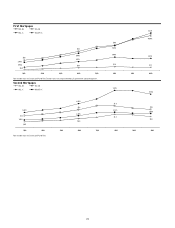

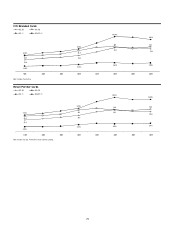

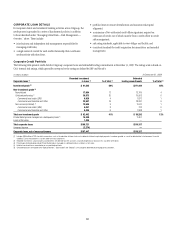

Interest Rate Risk Associated with Consumer Mortgage

Lending Activity

Citigroup originates and funds mortgage loans. As with all other lending

activity, this exposes Citigroup to several risks, including credit, liquidity and

interest rate risks. To manage credit and liquidity risk, Citigroup sells most

of the mortgage loans it originates, but retains the servicing rights. These

sale transactions create an intangible asset referred to as mortgage servicing

rights (MSRs). The fair value of this asset is primarily affected by changes

in prepayments that result from shifts in mortgage interest rates. Thus,

by retaining the servicing rights of sold mortgage loans, Citigroup is still

exposed to interest rate risk.

In managing this risk, Citigroup hedges a significant portion of the value

of its MSRs through the use of interest rate derivative contracts, forward

purchase commitments of mortgage-backed securities, and purchased

securities classified as trading (primarily mortgage-backed securities

including principal-only strips).

Since the change in the value of these hedging instruments does not

perfectly match the change in the value of the MSRs, Citigroup is still

exposed to what is commonly referred to as “basis risk.” Citigroup manages

this risk by reviewing the mix of the various hedging instruments referred to

above on a daily basis.

Citigroup’s MSRs totaled $6.530 billion and $5.657 billion at

December 31, 2009 and December 31, 2008, respectively. For additional

information on Citi’s MSRs, see Notes 19 and 23 to the Consolidated

Financial Statements.

As part of the mortgage lending activity, Citigroup commonly enters into

purchase commitments to fund residential mortgage loans at specific interest

rates within a given period of time, generally up to 60 days after the rate has

been set. If the resulting loans from these commitments will be classified as

loans held-for-sale, Citigroup accounts for the commitments as derivatives.

Accordingly, the initial and subsequent changes in the fair value of these

commitments, which are driven by changes in mortgage interest rates, are

recognized in current earnings after taking into consideration the likelihood

that the commitment will be funded.

Citigroup hedges its exposure to the change in the value of these

commitments by utilizing hedging instruments similar to those referred

to above.