Citibank 2009 Annual Report Download - page 233

Download and view the complete annual report

Please find page 233 of the 2009 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

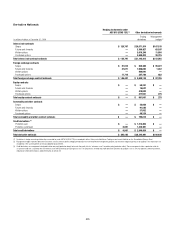

223

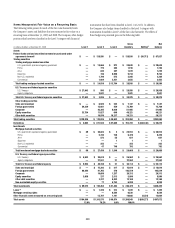

25. CONCENTRATIONS OF CREDIT RISK

Concentrations of credit risk exist when changes in economic, industry or

geographic factors similarly affect groups of counterparties whose aggregate

credit exposure is material in relation to Citigroup’s total credit exposure.

Although Citigroup’s portfolio of financial instruments is broadly diversified

along industry, product, and geographic lines, material transactions are

completed with other financial institutions, particularly in the securities

trading, derivatives, and foreign exchange businesses.

In connection with the Company’s efforts to maintain a diversified

portfolio, the Company limits its exposure to any one geographic region,

country or individual creditor and monitors this exposure on a continuous

basis. At December 31, 2009, Citigroup’s most significant concentration of

credit risk was with the U.S. government and its agencies. The Company’s

exposure, which primarily results from trading assets and investments

issued by the U.S. government and its agencies, amounted to $126.6

billion and $93.7 billion at December 31, 2009 and 2008, respectively. The

Mexican and Japanese governments and their agencies are the next largest

exposures, which are rated investment grade by both Moody’s and S&P. The

Company’s exposure to Mexico amounted to $41.4 billion and $35.0 billion

at December 31, 2009 and 2008, respectively, and is composed of investment

securities, loans and trading assets. The Company’s exposure to Japan

amounted to $31.8 billion and $29.1 billion at December 31, 2009 and 2008,

respectively, and is composed of investment securities, loans and trading

assets.

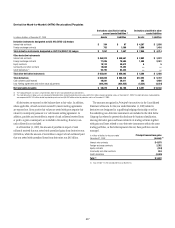

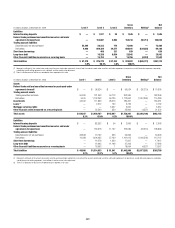

26. FAIR VALUE MEASUREMENT

Effective January 1, 2007, the Company adopted SFAS 157 (now ASC

820-10), which defines fair value, establishes a consistent framework for

measuring fair value and expands disclosure requirements about fair value

measurements. Among other things, the standard requires the Company to

maximize the use of observable inputs and minimize the use of unobservable

inputs when measuring fair value. In addition, it precludes the use of

block discounts when measuring the fair value of instruments traded in an

active market; such discounts were previously applied to large holdings of

publicly traded equity securities. It also requires recognition of trade-date

gains related to certain derivative transactions whose fair value has been

determined using unobservable market inputs. This guidance supersedes the

guidance in Emerging Issues Task Force Issue No. 02-3, “Issues Involved in

Accounting for Derivative Contracts Held for Trading Purposes and Contracts

Involved in Energy Trading and Risk Management Activities” (EITF

Issue 02-3), which prohibited the recognition of trade-date gains for such

derivative transactions when determining the fair value of instruments not

traded in an active market.

As a result of the adoption of the standard, the Company made

amendments to the techniques used in measuring the fair value of derivative

and other positions. These amendments change the way that the probability

of default of a counterparty is factored into the valuation of derivative

positions, include for the first time the impact of Citigroup’s own credit risk

on derivatives and other liabilities measured at fair value, and also eliminate

the portfolio servicing adjustment that is no longer necessary.

Fair Value Hierarchy

ASC 820-10 also specifies a hierarchy of valuation techniques based

on whether the inputs to those valuation techniques are observable

or unobservable. Observable inputs reflect market data obtained from

independent sources, while unobservable inputs reflect the Company’s

market assumptions. These two types of inputs have created the following

fair-value hierarchy:

Level 1• : Quoted prices for identical instruments in active markets.

Level 2• : Quoted prices for similar instruments in active markets; quoted

prices for identical or similar instruments in markets that are not

active; and model-derived valuations in which all significant inputs and

significant value drivers are observable in active markets.

Level 3• : Valuations derived from valuation techniques in which one or

more significant inputs or significant value drivers are unobservable.

This hierarchy requires the use of observable market data when available.

The Company considers relevant and observable market prices in its

valuations where possible. The frequency of transactions, the size of the bid-

ask spread and the amount of adjustment necessary when comparing similar

transactions are all factors in determining the liquidity of markets and the

relevance of observed prices in those markets.