Citibank 2009 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2009 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

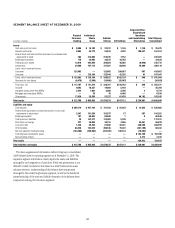

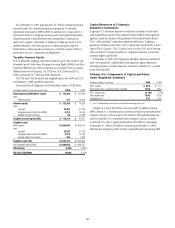

50

Liquidity management is overseen by the Board of Directors through

its Risk Management and Finance Committee and by senior management

through Citigroup’s Finance and Asset and Liability Committee (FinALCO).

One of the objectives of the Risk Management and Finance Committee of

Citigroup’s Board of Directors as well as the FinALCO is to monitor and review

overall liquidity policies and practices as well as the liquidity and balance

sheet positions of Citigroup and its principal subsidiaries. Additionally,

oversight of liquidity is provided by Citigroup’s Global Asset and Liability

Committee. Asset and Liability Committees are also established for each

region, country and/or major line of business.

MONITORING LIQUIDITY

Funding and Liquidity Plans

Each principal operating subsidiary and/or country must prepare a Funding

and Liquidity Plan for approval by the Treasurer and independent risk

management. For significant entities, as defined by balance sheet size and

the liquidity risk position, the Funding and Liquidity Plan is prepared and

approved on an annual basis. The Funding and Liquidity Plan addresses

strategic liquidity issues and establishes the parameters for identifying,

measuring, monitoring and limiting liquidity risk and sets forth key

assumptions for liquidity risk management. The Funding and Liquidity Plan

includes analysis of the balance sheet, as well as the economic and business

conditions impacting, or potentially impacting, the liquidity of the major

operating subsidiary and/or country. As part of the Funding and Liquidity

Plan, liquidity limits, liquidity ratios, market triggers, and assumptions for

periodic stress tests are established and approved.

Risk Tolerance

Citigroup establishes its key risk tolerances based on stress tests and a cash

capital ratio (as described in “Liquidity Ratios” below). This framework

requires that entities be self-sufficient or net providers of liquidity in their

designated stress tests and have excess cash capital. Aggregate self sufficiency

targets have been established for the banking subsidiaries, Citigroup, the

parent holding company, and CGMHI as well as for individual entities as part

of their Funding and Liquidity Plans. In addition, an important benchmark

for the combined Citigroup, the parent holding company, and CGMHI is to

maintain sufficient liquidity to meet all maturing obligations for a one-year

period without access to the unsecured wholesale markets.

Within this context, there are a series of tools used to monitor Citigroup’s

liquidity position. These include liquidity gaps and associated limits, liquidity

ratios, stress testing and market triggers, as described below.

Liquidity Gaps and Limits

Citigroup uses a monitoring tool that measures potential funding gaps over

various time horizons in a standard operating environment. The gap for

any given funding need represents the potential market access required,

or placements to the market (internal or external) over designated tenors.

Limits establish risk appetite for potential market access in standard

operating conditions and are monitored against the liquidity position

on a daily basis. Limits are established based on evaluation of available

contingent actions and liquidity vulnerabilities under designated stress

scenarios. While the contingent capacity places a cap on the limits, the limits

are also evaluated based on the structural liquidity of the balance sheet,

stability of liabilities, liquidity of assets, depth of markets, the experience

of management, size of the balance sheet, historical utilization, and an

evaluation of expected business and funding strategy. Limits are established

such that in stress scenarios, entities are self-funded or net providers of

liquidity. Thus, the risk tolerance for liquidity funding gaps is limited based

on the capacity to cover the position in a stressed environment. These limits

are the key daily risk-management tool for Citigroup, the parent holding

company, and its banking subsidiaries.

Liquidity Ratios

A series of standard corporate-wide liquidity ratios has been established

to monitor the structural elements of Citigroup’s liquidity. One of the

key structural liquidity measures is the cash capital ratio. Cash capital is

a broader measure of the ability to fund the structurally illiquid portion

of Citigroup’s balance sheet than traditional measures such as deposits

to loans or core deposits to loans. Cash capital measures the amount of

long-term funding (>1 year) available to fund illiquid assets. Long-term

funding includes core customer deposits, long-term debt and equity. Illiquid

assets include loans (net of liquidity adjustments), illiquid securities,

securities haircuts and other assets (i.e., goodwill, intangibles, fixed assets,

receivables, etc.). Cash capital targets are established for Citigroup, the

parent holding company, CGMHI and Citigroup’s aggregate banking

subsidiaries. In addition, each entity is required to calculate a cash capital

ratio on a monthly basis. Benchmarks must be established and approved for

the cash capital ratio as part of the entities’ Funding and Liquidity plan. At

December 31, 2009, the combined Citigroup, the parent holding company,

and CGMHI, as well as the aggregate banking subsidiaries had an excess of

cash capital. In addition, as of December 31, 2009 the combined Citigroup,

the parent holding company, and CGMHI maintained liquidity to meet all

maturing obligations significantly in excess of a one-year period without

access to the unsecured wholesale markets.