Citibank 2009 Annual Report Download - page 139

Download and view the complete annual report

Please find page 139 of the 2009 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

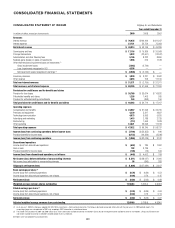

129

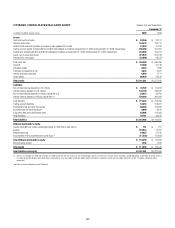

Corporate loans

Corporate loans represent loans and leases managed by ICG or the Special

Asset Pool. Corporate loans are identified as impaired and placed on a cash

(non-accrual) basis when it is determined that the payment of interest or

principal is doubtful or when interest or principal is 90 days past due, except

when the loan is well collateralized and in the process of collection. Any

interest accrued on impaired corporate loans and leases is reversed at 90 days

and charged against current earnings, and interest is thereafter included in

earnings only to the extent actually received in cash. When there is doubt

regarding the ultimate collectability of principal, all cash receipts are

thereafter applied to reduce the recorded investment in the loan.

Impaired corporate loans and leases are written down to the extent

that principal is judged to be uncollectible. Impaired collateral-dependent

loans and leases, where repayment is expected to be provided solely by

the sale of the underlying collateral and there are no other available and

reliable sources of repayment, are written down to the lower of cost or

collateral value. Cash-basis loans are returned to an accrual status when

all contractual principal and interest amounts are reasonably assured of

repayment and there is a sustained period of repayment performance in

accordance with the contractual terms.

Loans Held-for-Sale

Corporate and consumer loans that have been identified for sale are classified

as loans held-for-sale included in Other assets. With the exception of certain

mortgage loans for which the fair value option has been elected, these loans

are accounted for at the lower of cost or market value (LOCOM), with any

write-downs or subsequent recoveries charged to Other revenue.

Allowance for Loan Losses

Allowance for loan losses represents management’s best estimate of probable

losses inherent in the portfolio, as well as probable losses related to large

individually evaluated impaired loans and troubled debt restructurings.

Attribution of the allowance is made for analytical purposes only, and

the entire allowance is available to absorb probable credit losses inherent

in the overall portfolio. Additions to the allowance are made through the

provision for credit losses. Credit losses are deducted from the allowance, and

subsequent recoveries are added. Securities received in exchange for loan

claims in debt restructurings are initially recorded at fair value, with any

gain or loss reflected as a recovery or charge-off to the allowance, and are

subsequently accounted for as securities available-for-sale.

Corporate loans

In the Corporate portfolios, the allowance for loan losses includes an

asset-specific component and a statistically-based component. The asset

specific component is calculated under ASC 310-10-35, Receivables—

Subsequent Measurement (formerly SFAS 114) on an individual basis for

larger-balance, non-homogeneous loans, which are considered impaired.

An asset-specific allowance is established when the discounted cash flows,

collateral value (less disposal costs), or observable market price of the

impaired loan is lower than its carrying value. This allowance considers

the borrower’s overall financial condition, resources, and payment record,

the prospects for support from any financially responsible guarantors

and, if appropriate, the realizable value of any collateral. The asset

specific component of the allowance for smaller balance impaired loans

is calculated on a pool basis considering historical loss experience. The

allowance for the remainder of the loan portfolio is calculated under ASC

450, Contingencies (formerly SFAS 5) using a statistical methodology,

supplemented by management judgment. The statistical analysis considers

the portfolio’s size, remaining tenor, and credit quality as measured by

internal risk ratings assigned to individual credit facilities, which reflect

probability of default and loss given default. The statistical analysis considers

historical default rates and historical loss severity in the event of default,

including historical average levels and historical variability. The result is

an estimated range for inherent losses. The best estimate within the range is

then determined by management’s quantitative and qualitative assessment

of current conditions, including general economic conditions, specific

industry and geographic trends, and internal factors including portfolio

concentrations, trends in internal credit quality indicators, and current and

past underwriting standards.

Consumer loans

For Consumer loans, each portfolio of smaller-balance, homogeneous

loans—including consumer mortgage, installment, revolving credit, and

most other consumer loans—is independently evaluated for impairment. The

allowance for loan losses attributed to these loans is established via a process

that estimates the probable losses inherent in the specific portfolio based

upon various analyses. These include migration analysis, in which historical

delinquency and credit loss experience is applied to the current aging of the

portfolio, together with analyses that reflect current trends and conditions.

Management also considers overall portfolio indicators, including

historical credit losses, delinquent, non-performing, and classified loans,

trends in volumes and terms of loans, an evaluation of overall credit quality,

the credit process, including lending policies and procedures, and economic,

geographical, product and other environmental factors.

In addition, valuation allowances are determined for impaired smaller-

balance homogeneous loans whose terms have been modified due to the

borrowers’ financial difficulties and where it has been determined that a

concession will be granted to the borrower. Such modifications may include

interest rate reductions, principal forgiveness and/or term extensions. Where

long-term concessions have been granted, such modifications are accounted for