Citibank 2009 Annual Report Download - page 203

Download and view the complete annual report

Please find page 203 of the 2009 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

193

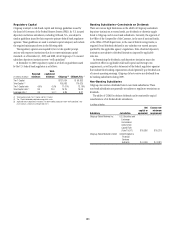

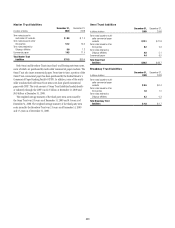

Regulatory Capital

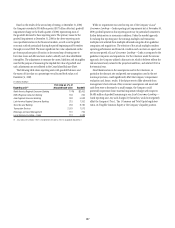

Citigroup is subject to risk based capital and leverage guidelines issued by

the Board of Governors of the Federal Reserve System (FRB). Its U.S. insured

depository institution subsidiaries, including Citibank, N.A., are subject to

similar guidelines issued by their respective primary federal bank regulatory

agencies. These guidelines are used to evaluate capital adequacy and include

the required minimums shown in the following table.

The regulatory agencies are required by law to take specific prompt

actions with respect to institutions that do not meet minimum capital

standards. As of December 31, 2009 and 2008, all of Citigroup’s U.S. insured

subsidiary depository institutions were “well capitalized.”

At December 31, 2009, regulatory capital as set forth in guidelines issued

by the U.S. federal bank regulators is as follows:

In millions of dollars

Required

minimum

Well-

capitalized

minimum Citigroup (3) Citibank, N.A. (3)

Tier 1 Capital $127,034 $ 96,833

Total Capital (1) 165,983 110,625

Tier 1 Capital ratio 4.0 % 6.0% 11.67% 13.16%

Total Capital ratio (1) 8.0 10.0 15.25 15.03

Leverage ratio (2) 3.0 5.0 (3) 6.89 8.31

(1) Total Capital includes Tier 1 Capital and Tier 2 Capital.

(2) Tier 1 Capital divided by adjusted average total assets.

(3) Applicable only to depository institutions. For bank holding companies to be “well capitalized,” they

must maintain a minimum Leverage ratio of 3%.

Banking Subsidiaries—Constraints on Dividends

There are various legal limitations on the ability of Citigroup’s subsidiary

depository institutions to extend credit, pay dividends or otherwise supply

funds to Citigroup and its non-bank subsidiaries. Currently, the approval of

the Office of the Comptroller of the Currency, in the case of national banks,

or the Office of Thrift Supervision, in the case of federal savings banks, is

required if total dividends declared in any calendar year exceed amounts

specified by the applicable agency’s regulations. State-chartered depository

institutions are subject to dividend limitations imposed by applicable

state law.

In determining the dividends, each depository institution must also

consider its effect on applicable risk-based capital and leverage ratio

requirements, as well as policy statements of the federal regulatory agencies

that indicate that banking organizations should generally pay dividends out

of current operating earnings. Citigroup did not receive any dividends from

its banking subsidiaries during 2009.

Non-Banking Subsidiaries

Citigroup also receives dividends from its non-bank subsidiaries. These

non-bank subsidiaries are generally not subject to regulatory restrictions on

dividends.

The ability of CGMHI to declare dividends can be restricted by capital

considerations of its broker-dealer subsidiaries.

In millions of dollars

Subsidiary Jurisdiction

Net

capital or

equivalent

Excess over

minimum

requirement

Citigroup Global Markets Inc. U.S. Securities and

Exchange

Commission

Uniform Net

Capital Rule

(Rule 15c3-1) $10,886 $10,218

Citigroup Global Markets Limited United Kingdom’s

Financial

Services

Authority $ 6,409 $ 3,081