Citibank 2009 Annual Report Download - page 214

Download and view the complete annual report

Please find page 214 of the 2009 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

204

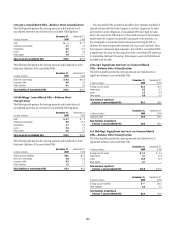

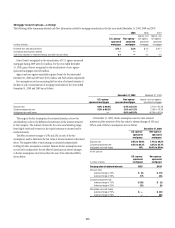

Citibank (South Dakota), N.A. is the sole provider of full liquidity facilities

to the commercial paper programs of the Master and Omni Trusts. Both

of these facilities, which represent contractual obligations on the part of

Citibank (South Dakota), N.A. to provide liquidity for the issued commercial

paper, are made available on market terms to each of the trusts. The liquidity

facilities require Citibank (South Dakota), N.A. to purchase the commercial

paper issued by each trust at maturity, if the commercial paper does not

roll over, as long as there are available credit enhancements outstanding,

typically in the form of subordinated notes. The liquidity commitment

related to the Omni Trust commercial paper programs amounted to $4.4

billion at December 31, 2009 and $8.5 billion at December 31, 2008. The

liquidity commitment related to the Master Trust commercial paper program

amounted to $14.5 billion at December 31, 2009 and $11.0 billion at

December 31, 2008. As of December 31, 2009 and December 31, 2008, none

of the Master Trust or Omni Trust liquidity commitments were drawn.

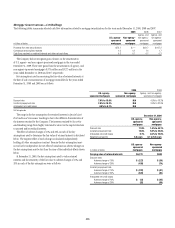

In addition, Citibank (South Dakota), N.A. provides liquidity to a third-

party, non-consolidated multi-seller commercial paper conduit, which is

not a VIE. The commercial paper conduit has acquired notes issued by the

Omni Trust. Citibank (South Dakota), N.A. provides the liquidity facility

on market terms. Citibank (South Dakota), N.A. will be required to act

in its capacity as liquidity provider as long as there are available credit

enhancements outstanding and if: (1) the conduit is unable to roll over its

maturing commercial paper; or (2) Citibank (South Dakota), N.A. loses its

A-1/P-1 credit rating. The liquidity commitment to the third-party conduit

was $2.5 billion at December 31, 2009 and $3.6 billion at December 31, 2008.

As of December 31, 2009 and December 31, 2008, none of this liquidity

commitment was drawn.

During the first half of 2009, all three of Citigroup’s primary credit card

securitization trusts—Master Trust, Omni Trust, and Broadway Trust—had

bonds placed on ratings watch with negative implications by rating agencies.

As a result of the ratings watch status, certain actions were taken by Citi with

respect to each of the trusts. In general, the actions subordinated certain

senior interests in the trust assets that were retained by Citi, which effectively

placed these interests below investor interests in terms of priority of payment.

As a result of these actions, based on the applicable regulatory capital

rules, Citigroup began including the sold assets for all three of the credit card

securitization trusts in its risk-weighted assets for purposes of calculating

its risk-based capital ratios during 2009. The increase in risk-weighted

assets occurred in the quarter during 2009 in which the respective actions

took place. The effect of these changes increased Citigroup’s risk-weighted

assets by approximately $82 billion, and decreased Citigroup’s Tier 1 Capital

ratio by approximately 100 basis points each as of March 31, 2009, with

respect to the Master and Omni Trusts. The inclusion of the Broadway Trust

increased Citigroup’s risk-weighted assets by an additional approximately

$900 million at June 30, 2009. All bond ratings for each of the trusts have

been affirmed by the rating agencies, and no downgrades have occurred as

of December 31, 2009.

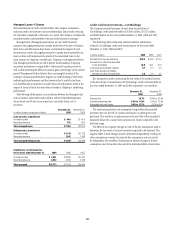

Mortgage Securitizations

The Company provides a wide range of mortgage loan products to a diverse

customer base. In connection with the securitization of these loans, the

Company’s U.S. Consumer mortgage business retains the servicing rights,

which entitles the Company to a future stream of cash flows based on the

outstanding principal balances of the loans and the contractual servicing fee.

Failure to service the loans in accordance with contractual requirements may

lead to a termination of the servicing rights and the loss of future servicing

fees. In non-recourse servicing, the principal credit risk to the Company is

the cost of temporary advances of funds. In recourse servicing, the servicer

agrees to share credit risk with the owner of the mortgage loans, such as

FNMA or FHLMC, or with a private investor, insurer or guarantor. Losses

on recourse servicing occur primarily when foreclosure sale proceeds of the

property underlying a defaulted mortgage loan are less than the outstanding

principal balance and accrued interest of the loan and the cost of holding

and disposing of the underlying property. The Company’s mortgage loan

securitizations are primarily non-recourse, thereby effectively transferring

the risk of future credit losses to the purchasers of the securities issued by the

trust. Securities and Banking and Special Asset Pool retain servicing for a

limited number of their mortgage securitizations.

The Company’s Consumer business provides a wide range of mortgage

loan products to its customers. Once originated, the Company often

securitizes these loans through the use of QSPEs. These QSPEs are funded

through the issuance of Trust Certificates backed solely by the transferred

assets. These certificates have the same average life as the transferred assets.

In addition to providing a source of liquidity and less expensive funding,

securitizing these assets also reduces the Company’s credit exposure to the

borrowers. These mortgage loan securitizations are primarily non-recourse.

However, the Company generally retains the servicing rights and in certain

instances retains investment securities, interest-only strips and residual

interests in future cash flows from the trusts.