Citibank 2009 Annual Report Download - page 222

Download and view the complete annual report

Please find page 222 of the 2009 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

212

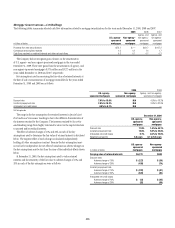

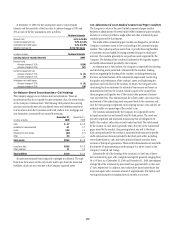

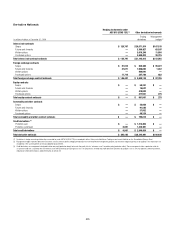

The following table summarizes selected cash flow information related to

asset-based financing for the years ended December 31, 2009, 2008 and 2007:

In billions of dollars 2009 2008 2007

Cash flows received on retained interests

and other net cash flows $2.7 $1.7 $—

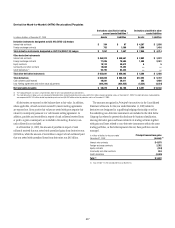

The effect of two negative changes in discount rates used to determine the

fair value of retained interests is disclosed below.

In millions of dollars

Asset-based

financing

Carrying value of retained interests $ 6,981

Value of underlying portfolio

Adverse change of 10% $ —

Adverse change of 20% (265)

Municipal Securities Tender Option Bond (TOB) Trusts

The Company sponsors TOB trusts that hold fixed- and floating-rate,

tax-exempt securities issued by state or local municipalities. The trusts are

typically single-issuer trusts whose assets are purchased from the Company

and from the secondary market. The trusts issue long-term senior floating

rate notes (Floaters) and junior residual securities (Residuals). The Floaters

have a long-term rating based on the long-term rating of the underlying

municipal bond and a short-term rating based on that of the liquidity

provider to the trust. The Residuals are generally rated based on the long-

term rating of the underlying municipal bond and entitle the holder to the

residual cash flows from the issuing trust.

The Company sponsors three kinds of TOB trusts: customer TOB trusts,

proprietary TOB trusts and QSPE TOB trusts.

Customer TOB trusts• are trusts through which customers finance

investments in municipal securities and are not consolidated by the

Company. Proprietary and QSPE TOB trusts, on the other hand, provide

the Company with the ability to finance its own investments in municipal

securities.

Proprietary TOB trusts• are generally consolidated, in which case the

financing (the Floaters) is recognized on the Company’s balance sheet as

a liability. However, certain proprietary TOB trusts are not consolidated

by the Company, where the Residuals are held by hedge funds that are

consolidated and managed by the Company. The assets and the associated

liabilities of these TOB trusts are not consolidated by the hedge funds

(and, thus, are not consolidated by the Company) under the application

of ASC 946, Financial Service—Investment Companies, which

precludes consolidation of owned investments. The Company consolidates

the hedge funds, because the Company holds controlling financial

interests in the hedge funds. Certain of the Company’s equity investments

in the hedge funds are hedged with derivatives transactions executed by

the Company with third parties referencing the returns of the hedge fund.

QSPE TOB trusts• provide the Company with the same exposure as

proprietary TOB trusts and are not consolidated by the Company.

Credit rating distribution is based on the external rating of the municipal

bonds within the TOB trusts, including any credit enhancement provided by

monoline insurance companies or the Company in the primary or secondary

markets, as discussed below. The total assets for proprietary TOB Trusts

(consolidated and non-consolidated) includes $0.7 billion of assets where the

Residuals are held by a hedge fund that is consolidated and managed by the

Company.

The TOB trusts fund the purchase of their assets by issuing Floaters along

with Residuals, which are frequently less than 1% of a trust’s total funding.

The tenor of the Floaters matches the maturity of the TOB trust and is equal

to or shorter than the tenor of the municipal bond held by the trust, and the

Floaters bear interest rates that are typically reset weekly to a new market rate

(based on the SIFMA index). Floater holders have an option to tender the

Floaters they hold back to the trust periodically. Customer TOB trusts issue

the Floaters and Residuals to third parties. Proprietary and QSPE TOB trusts

issue the Floaters to third parties and the Residuals are held by the Company.

Approximately $2.2 billion of the municipal bonds owned by TOB trusts

have an additional credit guarantee provided by the Company. In all other

cases, the assets are either unenhanced or are insured with a monoline

insurance provider in the primary market or in the secondary market.

While the trusts have not encountered any adverse credit events as defined

in the underlying trust agreements, certain monoline insurance companies

have experienced downgrades. In these cases, the Company has proactively

managed the TOB programs by applying additional secondary market

insurance on the assets or proceeding with orderly unwinds of the trusts.

The Company, in its capacity as remarketing agent, facilitates the sale

of the Floaters to third parties at inception of the trust and facilitates the

reset of the Floater coupon and tenders of Floaters. If Floaters are tendered

and the Company (in its role as remarketing agent) is unable to find a new

investor within a specified period of time, it can declare a failed remarketing

(in which case the trust is unwound) or may choose to buy the Floaters

into its own inventory and may continue to try to sell it to a third-party

investor. While the level of the Company’s inventory of Floaters fluctuates,

the Company held none of the Floater inventory related to the customer,

proprietary and QSPE TOB programs as of December 31, 2009.

If a trust is unwound early due to an event other than a credit event

on the underlying municipal bond, the underlying municipal bond is

sold in the secondary market. If there is an accompanying shortfall in the

trust’s cash flows to fund the redemption of the Floaters after the sale of

the underlying municipal bond, the trust draws on a liquidity agreement

in an amount equal to the shortfall. Liquidity agreements are generally

provided to the trust directly by the Company. For customer TOBs where

the Residual is less than 25% of the trust’s capital structure, the Company