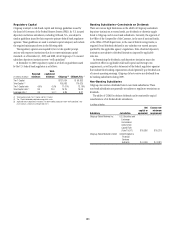

Citibank 2009 Annual Report Download - page 205

Download and view the complete annual report

Please find page 205 of the 2009 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

195

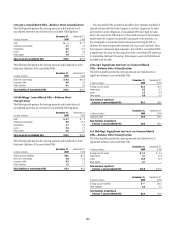

23. SECURITIZATIONS AND VARIABLE INTEREST

ENTITIES

Overview

Citigroup and its subsidiaries are involved with several types of off-balance-

sheet arrangements, including special purpose entities (SPEs). See Note 1

to the Consolidated Financial Statements for a discussion of impending

accounting changes to the accounting for transfers and servicing of

financial assets and Consolidation of Variable Interest Entities, including the

elimination of Qualifying SPEs.

Uses of SPEs

An SPE is an entity designed to fulfill a specific limited need of the company

that organized it.

The principal uses of SPEs are to obtain liquidity and favorable capital

treatment by securitizing certain of Citigroup’s financial assets, to assist

clients in securitizing their financial assets, and to create investment

products for clients. SPEs may be organized in many legal forms including

trusts, partnerships or corporations. In a securitization, the company

transferring assets to an SPE converts those assets into cash before they

would have been realized in the normal course of business, through the

SPE’s issuance of debt and equity instruments, certificates, commercial

paper and other notes of indebtedness, which are recorded on the balance

sheet of the SPE and not reflected on the transferring company’s balance

sheet, assuming applicable accounting requirements are satisfied. Investors

usually have recourse to the assets in the SPE and often benefit from other

credit enhancements, such as a collateral account or over-collateralization

in the form of excess assets in the SPE, or from a liquidity facility, such as

a line of credit, liquidity put option or asset purchase agreement. The SPE

can typically obtain a more favorable credit rating from rating agencies

than the transferor could obtain for its own debt issuances, resulting in less

expensive financing costs. The SPE may also enter into derivative contracts

in order to convert the yield or currency of the underlying assets to match

the needs of the SPE investors or to limit or change the credit risk of the SPE.

Citigroup may be the provider of certain credit enhancements as well as the

counterparty to any related derivative contracts.

SPEs may be Qualifying SPEs (QSPEs) or Variable Interest Entities (VIEs)

or neither.

Qualifying SPEs

QSPEs are a special class of SPEs that have significant limitations on the

types of assets and derivative instruments they may own or enter into and

the types and extent of activities and decision-making they may engage in.

Generally, QSPEs are passive entities designed to purchase assets and pass

through the cash flows from those assets to the investors in the QSPE. QSPEs

may not actively manage their assets through discretionary sales and are

generally limited to making decisions inherent in servicing activities and

issuance of liabilities. QSPEs are generally exempt from consolidation by the

transferor of assets to the QSPE and any investor or counterparty.

Variable interest entities

VIEs are entities that have either a total equity investment that is insufficient

to permit the entity to finance its activities without additional subordinated

financial support or whose equity investors lack the characteristics of a

controlling financial interest (i.e., ability to make significant decisions

through voting rights, right to receive the expected residual returns of the

entity and obligation to absorb the expected losses of the entity). Investors

that finance the VIE through debt or equity interests or other counterparties

that provide other forms of support, such as guarantees, subordinated fee

arrangements, or certain types of derivative contracts, are variable interest

holders in the entity. The variable interest holder, if any, that will absorb

a majority of the entity’s expected losses, receive a majority of the entity’s

expected residual returns, or both, is deemed to be the primary beneficiary

and must consolidate the VIE. Consolidation of a VIE is determined based

primarily on variability generated in scenarios that are considered most

likely to occur, rather than based on scenarios that are considered more

remote. Certain variable interests may absorb significant amounts of losses

or residual returns contractually, but if those scenarios are considered very

unlikely to occur, they may not lead to consolidation of the VIE.

All of these facts and circumstances are taken into consideration when

determining whether the Company has variable interests that would deem

it the primary beneficiary and, therefore, require consolidation of the

related VIE or otherwise rise to the level where disclosure would provide

useful information to the users of the Company’s financial statements. In

some cases, it is qualitatively clear based on the extent of the Company’s

involvement or the seniority of its investments that the Company is not

the primary beneficiary of the VIE. In other cases, a more detailed and

quantitative analysis is required to make such a determination.

The Company generally considers the following types of involvement to be

significant:

assisting in the structuring of a transaction and retaining any amount •

of debt financing (e.g., loans, notes, bonds or other debt instruments)

or an equity investment (e.g., common shares, partnership interests or

warrants);

writing a “liquidity put” or other liquidity facility to support the issuance •

of short-term notes;

writing credit protection (e.g., guarantees, letters of credit, credit default •

swaps or total return swaps where the Company receives the total return or

risk on the assets held by the VIE); or

certain transactions where the Company is the investment manager and •

receives variable fees for services.

In various other transactions, the Company may act as a derivative

counterparty (for example, interest rate swap, cross-currency swap, or

purchaser of credit protection under a credit default swap or total return

swap where the Company pays the total return on certain assets to the SPE);

may act as underwriter or placement agent; may provide administrative,

trustee, or other services; or may make a market in debt securities or

other instruments issued by VIEs. The Company generally considers such

involvement, by itself, “not significant.”