Citibank 2009 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2009 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

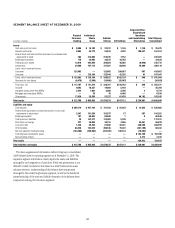

43

CAPITAL RESOURCES AND LIQUIDITY

CAPITAL RESOURCES

Overview

Capital has historically been generated by earnings from Citi’s operating

businesses. Citi may also augment its capital through issuances of common

stock, convertible preferred stock, preferred stock, equity issued through

awards under employee benefit plans, and, in the case of regulatory capital,

through the issuance of subordinated debt underlying trust preferred

securities. In addition, the impact of future events on Citi’s business results,

such as corporate and asset dispositions, as well as changes in accounting

standards, also affect Citi’s capital levels.

Generally, capital is used primarily to support assets in Citi’s businesses

and to absorb market, credit, or operational losses. While capital may be used

for other purposes, such as to pay dividends or repurchase common stock,

Citi’s ability to utilize its capital for these purposes is currently restricted

due to its agreements with the U.S. government, generally for so long as the

U.S. government continues to hold Citi’s common stock or trust preferred

securities. See also “Supervision and Regulation” below.

Citigroup’s capital management framework is designed to ensure that

Citigroup and its principal subsidiaries maintain sufficient capital consistent

with Citi’s risk profile and all applicable regulatory standards and guidelines,

as well as external rating agency considerations. The capital management

process is centrally overseen by senior management and is reviewed at the

consolidated, legal entity, and country level.

Senior management is responsible for the capital management process

mainly through Citigroup’s Finance and Asset and Liability Committee

(FinALCO), with oversight from the Risk Management and Finance

Committee of Citigroup’s Board of Directors. The FinALCO is composed

of the senior-most management of Citigroup for the purpose of engaging

management in decision-making and related discussions on capital

and liquidity matters. Among other things, FinALCO’s responsibilities

include: determining the financial structure of Citigroup and its principal

subsidiaries; ensuring that Citigroup and its regulated entities are adequately

capitalized in consultation with its regulators; determining appropriate asset

levels and return hurdles for Citigroup and individual businesses; reviewing

the funding and capital markets plan for Citigroup; and monitoring interest

rate risk, corporate and bank liquidity, and the impact of currency translation

on non-U.S. earnings and capital.

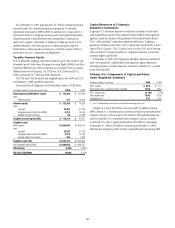

Capital Ratios

Citigroup is subject to the risk-based capital guidelines issued by the Federal

Reserve Board. Historically, capital adequacy has been measured, in part,

based on two risk-based capital ratios, the Tier 1 Capital and Total Capital

(Tier 1 Capital + Tier 2 Capital) ratios. Tier 1 Capital consists of the sum of

“core capital elements,” such as qualifying common stockholders’ equity,

as adjusted, qualifying noncontrolling interests, and qualifying mandatorily

redeemable securities of subsidiary trusts, principally reduced by goodwill,

other disallowed intangible assets, and disallowed deferred tax assets. Total

Capital also includes “supplementary” Tier 2 Capital elements, such as

qualifying subordinated debt and a limited portion of the allowance for

credit losses. Both measures of capital adequacy are stated as a percentage

of risk-weighted assets. Further, in conjunction with the conduct of the 2009

Supervisory Capital Assessment Program (SCAP), U.S. banking regulators

developed a new measure of capital termed “Tier 1 Common,” which

has been defined as Tier 1 Capital less non-common elements, including

qualifying perpetual preferred stock, qualifying noncontrolling interests, and

qualifying mandatorily redeemable securities of subsidiary trusts.

Citigroup’s risk-weighted assets are principally derived from application

of the risk-based capital guidelines related to the measurement of credit

risk. Pursuant to these guidelines, on-balance-sheet assets and the credit

equivalent amount of certain off-balance-sheet exposures (such as

financial guarantees, unfunded lending commitments, letters of credit, and

derivatives) are assigned to one of several prescribed risk-weight categories

based upon the perceived credit risk associated with the obligor, or if relevant,

the guarantor, the nature of the collateral, or external credit ratings.

Risk-weighted assets also incorporate a measure for market risk on covered

trading account positions and all foreign exchange and commodity positions

whether or not carried in the trading account. Excluded from risk-weighted

assets are any assets, such as goodwill and deferred tax assets, to the extent

required to be deducted from regulatory capital. See “Components of Capital

Under Regulatory Guidelines” below.

Citigroup is also subject to a Leverage ratio requirement, a non-risk-based

measure of capital adequacy, which is defined as Tier 1 Capital as a percentage

of quarterly adjusted average total assets.

To be “well capitalized” under federal bank regulatory agency definitions,

a bank holding company must have a Tier 1 Capital ratio of at least 6%, a

Total Capital ratio of at least 10%, and a Leverage ratio of at least 3%, and

not be subject to a Federal Reserve Board directive to maintain higher capital

levels. The following table sets forth Citigroup’s regulatory capital ratios as of

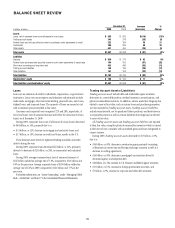

December 31, 2009 and December 31, 2008.

Citigroup Regulatory Capital Ratios

At year end 2009 2008

Tier 1 Common 9.60% 2.30%

Tier 1 Capital 11.67 11.92

Total Capital (Tier 1 Capital and Tier 2 Capital) 15.25 15.70

Leverage 6.89 6.08

As noted in the table above, Citigroup was “well capitalized” under the

federal bank regulatory agency definitions at year end for both 2009 and 2008.