Citibank 2009 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2009 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

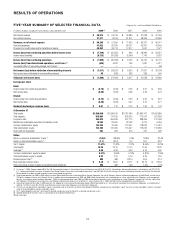

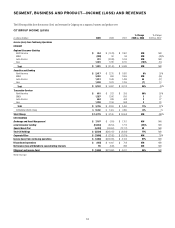

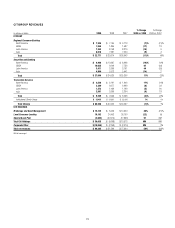

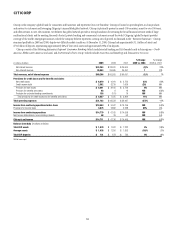

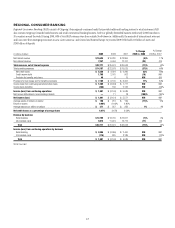

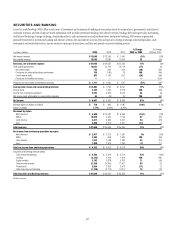

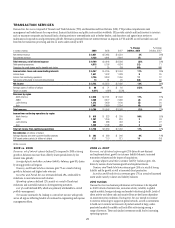

21

2008 vs. 2007

Revenues, net of interest expense increased 18% due to growth in the size

of the portfolio across Central and Eastern Europe and the Middle East.

Investment sales declined by 39% with assets under management declining

by 42% as a result of market conditions in the second half of 2008.

Net interest revenue was 31% higher than the prior year due to growth

in the size of the portfolio across Central and Eastern Europe and the Middle

East and growth in revolving balances. Average loans for retail banking were

up 26%, cards were up 49% and average deposits were up 22%.

Non-interest revenue decreased by 4% due to reduced investment revenue

as a result of market conditions.

Operating expenses increased 19%, reflecting growth in the portfolio and

repositioning charges.

Provisions for loan losses increased 49% to $312 million. Net credit

losses increased from $113 million to $237 million, while the Loan loss

reserve build decreased by 22% to $75 million. Credit costs increased as a

result of market conditions driving deterioration in the portfolio.

2010 Outlook

During 2010, EMEA RCB businesses are expected to operate in an

environment of continued challenging economic and credit conditions.

While key business drivers, including deposits, investment sales and card

purchase sales, began to show some signs of improvement during the

latter part of 2009, continued positive developments, if any, will depend

on the success of EMEA RCB’s strategy of concentrated focus on larger

urban markets. Credit quality is currently anticipated to improve modestly

with remedial programs and tighter origination standards reducing both

delinquencies and credit losses, with some continued pockets of weakness

in Poland and Hungary. Loan and card volume growth will continue to be

controlled, driven by tighter origination standards.