Citibank 2009 Annual Report Download - page 101

Download and view the complete annual report

Please find page 101 of the 2009 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

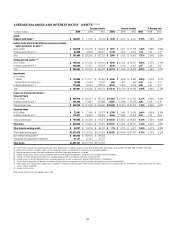

91

Trading Portfolios

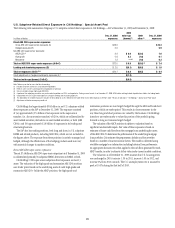

Price risk in trading portfolios is monitored using a series of measures, including:

factor sensitivities; •

value-at-risk (VAR); and •

stress testing. •

Factor sensitivities are expressed as the change in the value of a position

for a defined change in a market risk factor, such as a change in the value

of a Treasury bill for a one-basis-point change in interest rates. Citigroup’s

independent market risk management ensures that factor sensitivities are

calculated, monitored and, in most cases, limited, for all relevant risks taken

in a trading portfolio.

VAR estimates the potential decline in the value of a position or a portfolio

under normal market conditions. The VAR method incorporates the factor

sensitivities of the trading portfolio with the volatilities and correlations of

those factors and is expressed as the risk to Citigroup over a one-day holding

period, at a 99% confidence level. Citigroup’s VAR is based on the volatilities

of and correlations among a multitude of market risk factors as well as

factors that track the specific issuer risk in debt and equity securities.

Stress testing is performed on trading portfolios on a regular basis to

estimate the impact of extreme market movements. It is performed on

both individual trading portfolios, and on aggregations of portfolios and

businesses. Independent market risk management, in conjunction with the

businesses, develops stress scenarios, reviews the output of periodic stress-

testing exercises, and uses the information to make judgments as to the

ongoing appropriateness of exposure levels and limits.

Each trading portfolio has its own market risk limit framework

encompassing these measures and other controls, including permitted

product lists and a new product approval process for complex products.

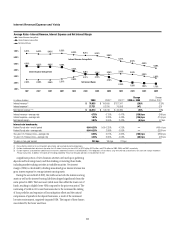

Total revenues of the trading business consist of:

customer revenue, which includes spreads from customer flow and •

positions taken to facilitate customer orders;

proprietary trading activities in both cash and derivative transactions; and •

net interest revenue.•

All trading positions are marked-to-market, with the result reflected in

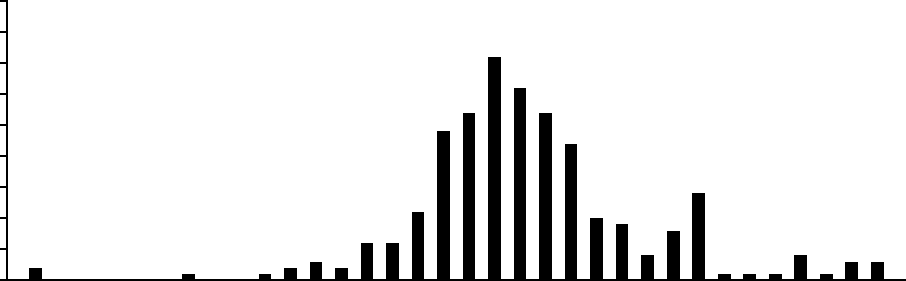

earnings. In 2009, negative trading-related revenue (net losses) was recorded

for 58 of 260 trading days. Of the 58 days on which negative revenue (net

losses) was recorded, two days were greater than $400 million. The following

histogram of total daily revenue or loss captures trading volatility and shows

the number of days in which Citigroup’s trading-related revenues fell within

particular ranges.

0

5

10

15

20

25

30

35

40

45

(300) to (275)

Revenues (in millions of dollars)

(650) to (400)

(25) to 0

(50) to (25)

(75) to (50)

(100) to (75)

(125) to (100)

(150) to (125)

(175) to (150)

(200) to (175)

(225) to (200)

(250) to (225)

(275) to (250)

(325) to (300)

(350) to (325)

(375) to (350)

(400) to (375)

0 to 25

25 to 50

50 to 75

75 to 100

100 to 125

125 to 150

150 to 175

175 to 200

200 to 225

225 to 250

250 to 275

275 to 300

300 to 325

325 to 350

350 to 375

375 to 400

400 to 550

Number of Trading Days

Histogram of Daily-Trading Related Revenue—12 Months Ended December 31, 2009

Citigroup periodically performs extensive back-testing of many hypothetical

test portfolios as one check of the accuracy of its VAR. Back-testing is the

process in which the daily VAR of a portfolio is compared to the actual daily

change in the market value of its transactions. Back-testing is conducted

to confirm that the daily market value losses in excess of a 99% confidence

level occur, on average, only 1% of the time. The VAR calculation for the

hypothetical test portfolios, with different degrees of risk concentration, meets

this statistical criteria.