Citibank 2009 Annual Report Download - page 231

Download and view the complete annual report

Please find page 231 of the 2009 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

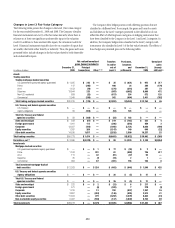

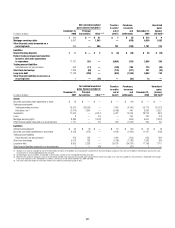

221

related to the forward-rate component of the foreign-currency forward

contracts and the time-value of foreign-currency options, are recorded in

the foreign-currency Cumulative translation adjustment account. For

foreign-currency denominated debt instruments that are designated as

hedges of net investments, the translation gain or loss that is recorded in

the foreign-currency translation adjustment account is based on the spot

exchange rate between the functional currency of the respective subsidiary

and the U.S. dollar, which is the functional currency of Citigroup. To the

extent the notional amount of the hedging instrument exactly matches the

hedged net investment and the underlying exchange rate of the derivative

hedging instrument relates to the exchange rate between the functional

currency of the net investment and Citigroup’s functional currency

(or, in the case of a non-derivative debt instrument, such instrument

is denominated in the functional currency of the net investment), no

ineffectiveness is recorded in earnings.

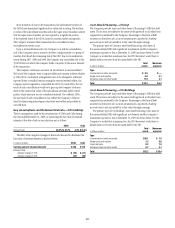

The pretax loss recorded in foreign-currency translation adjustment

within Accumulated other comprehensive income (loss), related to the

effective portion of the net investment hedges, is $4,560 million during the

year ended December 31, 2009.

Credit Derivatives

A credit derivative is a bilateral contract between a buyer and a seller

under which the seller agrees to provide protection to the buyer against the

credit risk of a particular entity (“reference entity” or “reference credit”).

Credit derivatives generally require that the seller of credit protection make

payments to the buyer upon the occurrence of predefined credit events

(commonly referred to as “settlement triggers”). These settlement triggers

are defined by the form of the derivative and the reference credit and are

generally limited to the market standard of failure to pay on indebtedness

and bankruptcy of the reference credit and, in a more limited range of

transactions, debt restructuring. Credit derivative transactions referring to

emerging market reference credits will also typically include additional

settlement triggers to cover the acceleration of indebtedness and the risk of

repudiation or a payment moratorium. In certain transactions, protection

may be provided on a portfolio of referenced credits or asset-backed securities.

The seller of such protection may not be required to make payment until a

specified amount of losses has occurred with respect to the portfolio and/or

may only be required to pay for losses up to a specified amount.

The Company makes markets in and trades a range of credit derivatives,

both on behalf of clients as well as for its own account. Through these

contracts, the Company either purchases or writes protection on either a

single name or a portfolio of reference credits. The Company uses credit

derivatives to help mitigate credit risk in its corporate and consumer loan

portfolio and other cash positions, to take proprietary trading positions, and

to facilitate client transactions.

The range of credit derivatives sold includes credit default swaps, total

return swaps and credit options.

A credit default swap is a contract in which, for a fee, a protection seller

agrees to reimburse a protection buyer for any losses that occur due to

a credit event on a reference entity. If there is no credit default event or

settlement trigger, as defined by the specific derivative contract, then the

protection seller makes no payments to the protection buyer and receives only

the contractually specified fee. However, if a credit event occurs as defined in

the specific derivative contract sold, the protection seller will be required to

make a payment to the protection buyer.

A total return swap transfers the total economic performance of a

reference asset, which includes all associated cash flows, as well as capital

appreciation or depreciation. The protection buyer receives a floating rate

of interest and any depreciation on the reference asset from the protection

seller and, in return, the protection seller receives the cash flows associated

with the reference asset plus any appreciation. Thus, according to the total

return swap agreement, the protection seller will be obligated to make a

payment anytime the floating interest rate payment and any depreciation

of the reference asset exceed the cash flows associated with the underlying

asset. A total return swap may terminate upon a default of the reference asset

subject to the provisions of the related total return swap agreement between

the protection seller and the protection buyer.

A credit option is a credit derivative that allows investors to trade or hedge

changes in the credit quality of the reference asset. For example, in a credit

spread option, the option writer assumes the obligation to purchase or sell the

reference asset at a specified “strike” spread level. The option purchaser buys

the right to sell the reference asset to, or purchase it from, the option writer at

the strike spread level. The payments on credit spread options depend either

on a particular credit spread or the price of the underlying credit-sensitive

asset. The options usually terminate if the underlying assets default.

A credit-linked note is a form of credit derivative structured as a debt

security with an embedded credit default swap. The purchaser of the note

writes credit protection to the issuer, and receives a return which will be

negatively affected by credit events on the underlying reference credit. If

the reference entity defaults, the purchaser of the credit-linked note may

assume the long position in the debt security and any future cash flows

from it, but will lose the amount paid to the issuer of the credit-linked note.

Thus the maximum amount of the exposure is the carrying amount of the

credit-linked note. As of December 31, 2009 and December 31, 2008, the

amount of credit-linked notes held by the Company in trading inventory was

immaterial.