Citibank 2008 Annual Report Download - page 98

Download and view the complete annual report

Please find page 98 of the 2008 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

future cash flows determined in step one. Own-credit CVA is determined

using Citi-specific CDS spreads for the relevant tenor. Generally, counterparty

CVA is determined using CDS spread indices for each credit rating and tenor.

For certain identified facilities where individual analysis is practicable (for

example, exposures to monoline counterparties) counterparty-specific CDS

spreads are used.

The CVA adjustment is designed to incorporate a market view of the credit

risk inherent in the derivative portfolio as required by SFAS 157. However,

most derivative instruments are negotiated bilateral contracts and are not

commonly transferred to third parties. Derivative instruments are normally

settled contractually, or if terminated early, are terminated at a value

negotiated bilaterally between the counterparties. Therefore, the CVA (both

counterparty and own-credit) may not be realized upon a settlement or

termination in the normal course of business. In addition, all or a portion of

the credit valuation adjustments may be reversed or otherwise adjusted in

future periods in the event of changes in the credit risk of Citi or its

counterparties, or changes in the credit mitigants (collateral and netting

agreements) associated with the derivative instruments. Historically,

Citigroup’s credit spreads have moved in tandem with general counterparty

credit spreads, thus providing offsetting CVAs affecting revenue. However, in

the fourth quarter of 2008, Citigroup’s credit spreads generally narrowed and

counterparty credit spreads widened, each of which negatively affected

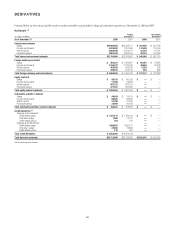

revenues. The table below summarizes the CVA applied to the fair value of

derivative instruments as of December 31, 2008 and 2007.

Credit valuation adjustment

Contra liability (contra asset)

In millions of dollars

December 31,

2008

December 31,

2007

Non-monoline counterparties $(8,266) $(1,613)

Citigroup (own) 3,611 1,329

Net non-monoline CVA (4,655) (284)

Monoline counterparties (1) (4,279) (967)

Total CVA—derivative instruments $(8,934) $(1,251)

(1) Certain derivatives with monoline counterparties were terminated during 2008.

The table below summarizes pre-tax gains (losses) related to changes in

credit valuation adjustments on derivative instruments for the years ended

December 31, 2008 and 2007:

Credit valuation

adjustment gain

(loss)

In millions of dollars 2008 2007

Non-monoline counterparties $ (6,653) $(1,301)

Citigroup (own) 2,282 1,329

Net non-monoline CVA (4,371) 28

Monoline counterparties (5,736) (967)

Total CVA—derivative instruments $(10,107) $ (939)

The credit valuation adjustment amounts shown above relate solely to the

derivative portfolio, and do not include:

• Own-credit adjustments for non-derivative liabilities measured at fair

value under the fair-value option. See Note 26 on page 192 for further

information.

• The effect of counterparty credit risk embedded in non-derivative

instruments. During 2008, general spread widening has negatively

affected the market value of a range of financial instruments. Losses on

non-derivative instruments, such as bonds and loans, related to

counterparty credit risk are not included in the table above.

Credit Derivatives

Like all other derivative types, the Company makes markets in and trades a

range of credit derivatives, both on behalf of clients as well as for its own

account. Through these contracts the Company either purchases or writes

protection on either a single-name or portfolio basis. The Company uses

credit derivatives to help mitigate credit risk in its corporate loan portfolio

and other cash positions, to take proprietary trading positions, and to

facilitate client transactions.

Credit derivatives generally require that the seller of credit protection

make payments to the buyer upon the occurrence of predefined events

(settlement triggers). These settlement triggers, which are defined by the

form of the derivative and the referenced credit, are generally limited to the

market standard of failure to pay on indebtedness and bankruptcy of the

reference credit and, in a more limited range of transactions, debt

restructuring. Credit derivative transactions referring to emerging market

reference credits will also typically include additional settlement triggers to

cover the acceleration of indebtedness and the risk of repudiation or a

payment moratorium. In certain transactions on a portfolio of referenced

credits or asset-backed securities, the seller of protection may not be required

to make payment until a specified amount of losses have occurred with

respect to the portfolio and/or may only be required to pay for losses up to a

specified amount.

92