Citibank 2008 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2008 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

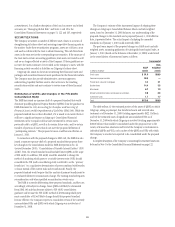

ACCOUNTING CHANGES

Adoption of SFAS 157—Fair Value Measurements

The Company elected to adopt SFAS No. 157, Fair Value Measurements

(SFAS 157), as of January 1, 2007. SFAS 157 does not determine or affect the

circumstances under which fair value measurements are used, but defines

fair value, expands disclosure requirements around fair value and specifies a

hierarchy of valuation techniques based on whether the inputs to those

valuation techniques are observable or unobservable. Observable inputs

reflect market data obtained from independent sources, while unobservable

inputs reflect the Company’s market assumptions. These two types of inputs

create the following fair value hierarchy:

• Level 1–Quoted prices for identical instruments in active markets.

• Level 2–Quoted prices for similar instruments in active markets; quoted

prices for identical or similar instruments in markets that are not active;

and model-derived valuations in which all significant inputs and

significant value drivers are observable in active markets.

• Level 3–Valuations derived from valuation techniques in which one or

more significant inputs or significant value drivers are unobservable.

This hierarchy requires the Company to use observable market data,

when available, and to minimize the use of unobservable inputs when

determining fair value.

For some products or in certain market conditions, observable inputs may

not be available. For example, during the market dislocations that occurred

in the second half of 2007, and continued throughout 2008, certain markets

became illiquid, and some key inputs used in valuing certain exposures were

unobservable. When and if these markets are liquid, the valuation of these

exposures will use the related observable inputs available at that time from

these markets.

Under SFAS 157, Citigroup is required to take into account its own credit

risk when measuring the fair value of derivative positions as well as other

liabilities for which it has elected fair value accounting under SFAS 155

Accounting for Certain Hybrid Financial Instruments (SFAS 155) and

SFAS 159, The Fair Value Option for Financial Assets and Financial

Liabilities (SFAS 159), after taking into consideration the effects of credit-

risk mitigants. The adoption of SFAS 157 has also resulted in some other

changes to the valuation techniques used by Citigroup when determining the

fair value of derivatives, most notably changes to the way that the probability

of default of a counterparty is factored in, and the elimination of a derivative

valuation adjustment which is no longer necessary under SFAS 157. The

cumulative effect at January 1, 2007 of making these changes was a gain of

$250 million after tax ($402 million pretax), or $0.05 per diluted share,

which was recorded in the 2007 first quarter earnings within the S&B

business.

SFAS 157 also precludes the use of block discounts for instruments traded

in an active market, which were previously applied to large holdings of

publicly traded equity securities, and requires the recognition of trade-date

gains related to certain derivative trades that use unobservable inputs in

determining their fair value. Previous accounting guidance allowed the use

of block discounts in certain circumstances and prohibited the recognition of

day-one gains on certain derivative trades when determining the fair value of

instruments not traded in an active market. The cumulative effect of these

changes resulted in an increase to January 1, 2007 Retained earnings of

$75 million.

Adoption of SFAS 159—Fair Value Option

In conjunction with the adoption of SFAS 157, the Company also adopted

SFAS 159, as of January 1, 2007. SFAS 159 provides for an election by the

Company, on an instrument-by-instrument basis for most financial assets

and liabilities to be reported at fair value with changes in fair value reported

in earnings. After the initial adoption, the election is made at the time of the

acquisition of a financial asset, financial liability or a firm commitment,

and it may not be revoked. SFAS 159 provides an opportunity to mitigate

volatility in reported earnings that resulted prior to its adoption from being

required to apply fair value accounting to certain economic hedges (e.g.,

derivatives) while having to measure the assets and liabilities being

economically hedged using an accounting method other than fair value.

Under the SFAS 159 transition provisions, the Company elected to apply

fair value accounting to certain financial instruments held at January 1,

2007 with future changes in value reported in earnings. The adoption of

SFAS 159 resulted in an after-tax decrease to January 1, 2007 retained

earnings of $99 million ($157 million pretax). See Note 27 to the

Consolidated Financial Statements on page 202 for additional information.

17