Citibank 2008 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2008 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

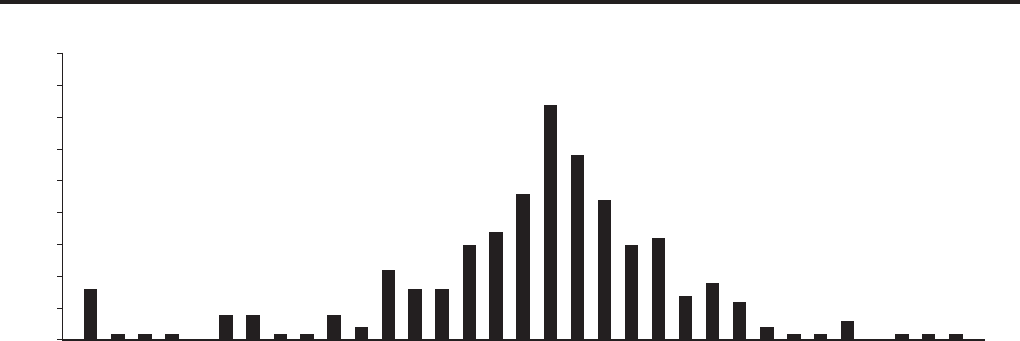

Total revenues of the trading business consist of:

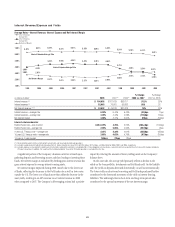

• customer revenue, which includes spreads from customer flow and

positions taken to facilitate customer orders;

• proprietary trading activities in both cash and derivative transactions; and

• net interest revenue.

All trading positions are marked to market, with the result reflected in

earnings. In 2008, negative trading-related revenue (net losses) was recorded

for 109 of 260 trading days. Of the 109 days on which negative revenue (net

losses) was recorded, 21 were greater than $400 million. The following

histogram of total daily revenue or loss captures trading volatility and shows

the number of days in which the Company’s trading-related revenues fell

within particular ranges.

($600) to ($550)

Histogram of Daily Trading-Related Revenue*

-

Twelve Months Ended December 31, 2008

-

5

10

15

20

40

35

30

25

45

Revenue (dollars in millions)

Number of Trading Days

*Includes subprime-related losses on credit positions which were marked intermittently during each month. Most of the loss events in the $800-$4,500 million category are due to

cumulative write-downs on these positions.

($4500) to ($800)

($50) to 0

($100) to ($50)

($150) to ($100)

($200) to ($150)

($250) to ($200)

($300) to ($250)

($350) to ($300)

($400) to ($350)

($450) to ($400)

($500) to ($450)

($550) to ($500)

($650) to ($600)

($700) to ($650)

($750) to ($700)

($800) to ($750)

0 to 50

50 to 100

100 to 150

150 to 200

200 to 250

250 to 300

300 to 350

350 to 400

400 to 450

450 to 500

500 to 550

550 to 600

600 to 650

650 to 700

700 to 750

750 to 800

Citigroup periodically performs extensive back-testing of many hypothetical

test portfolios as one check of the accuracy of its VAR. Back-testing is the

process in which the daily VAR of a portfolio is compared to the actual daily

change in the market value of its transactions. Back-testing is conducted to

confirm that the daily market value losses in excess of a 99% confidence level

occur, on average, only 1% of the time. The VAR calculation for the

hypothetical test portfolios, with different degrees of risk concentration,

meets this statistical criteria.

The level of price risk exposure at any given point in time depends on the

market environment and expectations of future price and market

movements, and will vary from period to period.

For Citigroup’s major trading centers, the aggregate pretax VAR in the

trading portfolios was $319 million at December 31, 2008 and $191 million

at December 31, 2007. Daily exposures averaged $292 million in 2008 and

ranged from $220 million to $393 million.

The Subprime Group (SPG) exposures became fully integrated into VAR

during the first quarter of 2008. As a result, December 31, 2008 VAR and

2008 average VAR increased by approximately $29 million and $111 million,

respectively.

74