Citibank 2008 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2008 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

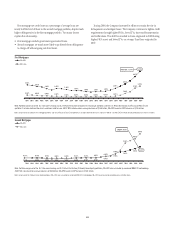

|

|

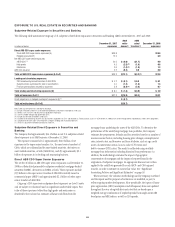

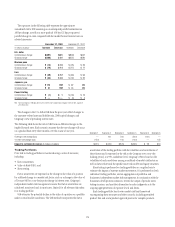

Direct Exposure to Monolines

In its Securities and Banking business, the Company has exposure to

various monoline bond insurers (Monolines), listed in the table below, from

hedges on certain investments and from trading positions. The hedges are

composed of credit default swaps and other hedge instruments. During

2007, the Company established a $967 million credit valuation adjustment

(CVA) reserve on the fair-value exposures related to these Monolines. In

2008, the Company added $5.7 billion to this reserve and recorded

utilizations of $2.4 billion, bringing the December 31, 2008 balance to $4.3

billion.

The following table summarizes the market value of the Company’s

direct exposures to and the corresponding notional amounts of transactions

with the various Monolines as well as the aggregate credit valuation

adjustment associated with these exposures as of December 31, 2008 and

2007 in S&B:

December 31, 2008 December 31, 2007

In millions of dollars

Fair-

value

exposure

Notional

amount

of

transactions

Fair-

value

exposure

Notional

amount

of

transactions

Direct subprime ABS CDO super senior:

Ambac $ 4,461 $5,357 $1,815 $ 5,485

FGIC ——909 1,460

ACA ——438 600

Radian ——100 100

Subtotal direct subprime ABS CDO super senior $ 4,461 $5,357 $3,262 $ 7,645

Trading assets—subprime:

Ambac ——$1,150 $ 1,400

Trading assets—subprime ——$1,150 $ 1,400

Trading assets—non-subprime:

MBIA $ 1,924 $4,040 $ 395 $ 5,620

FSA 204 1,126 121 1,126

ACA ——50 1,925

Assured 141 465 7 340

Radian 58 150 5 350

Ambac 21 1,106 — 1,971

Trading assets—non-subprime $ 2,348 $6,887 $ 578 $11,332

Subtotal trading assets $ 2,348 $6,887 $1,728 $12,732

Total gross fair-value direct exposure $ 6,809 $4,990

Credit valuation adjustment $(4,279) $ (967)

Total net fair-value direct exposure $ 2,530 $4,023

The fair-value exposure, net of payable and receivable positions,

represents the market value of the contract as of December 31, 2008 and

2007, excluding the credit valuation adjustment. The notional amount of

the transactions, including both long and short positions, is used as a

reference value to calculate payments. The credit valuation adjustment is a

downward adjustment to the fair-value exposure to a counterparty to reflect

the counterparty’s creditworthiness in respect of the obligations in question.

Credit market valuation adjustments are based on credit spreads and on

estimates of the terms and timing of the payment obligations of the

Monolines. Timing in turn depends on estimates of the performance of the

transactions to which the Company’s exposure relates, estimates of whether

and when liquidation of such transactions may occur and other factors,

each considered in the context of the terms of the Monolines’ obligations.

As of December 31, 2008 and 2007, the Company had $6.9 billion and

$10.5 billion, respectively, in notional amount of hedges against its direct

subprime ABS CDO super senior positions. Of those amounts, $5.3 billion

and $7.5 billion, respectively, were purchased from Monolines and are

included in the notional amount of transactions in the table above. The fair

value of the hedges provided by the Monolines against the Company’s direct

subprime ABS CDO super senior positions was $4.5 billion as of

December 31, 2008, and $3.3 billion as of December 31, 2007. There was

$0.9 billion net fair-value exposure related to direct subprime ABS CDO

super senior positions with a notional amount of $1.5 billion as of

December 31, 2007, which was settled during the fourth quarter of 2008.

With respect to Citi’s trading assets, there were $2.3 billion and $1.7

billion of fair-value exposure to Monolines as of December 31, 2008 and

2007, respectively. Trading assets include trading positions, both long and

short, in U.S. subprime RMBS and related products, including ABS CDOs.

There was $1.2 billion net fair-value exposure related to subprime trading

positions with a notional amount of $1.4 billion as of December 31, 2007,

which was settled during the third quarter of 2008.

70