Citibank 2008 Annual Report Download - page 201

Download and view the complete annual report

Please find page 201 of the 2008 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

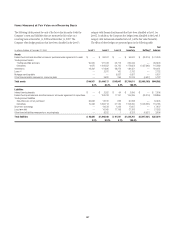

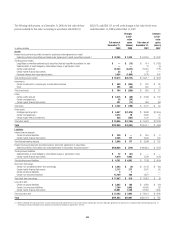

|

|

Counterparty and own credit adjustments consider the estimated future

cash flows between Citi and its counterparties under the terms of the

instrument and the effect of credit risk on the valuation of those cash flows,

rather than a point-in-time assessment of the current recognized net asset or

liability. Furthermore, the credit-risk adjustments take into account the effect

of credit-risk mitigants, such as pledged collateral and any legal right of

offset (to the extent such offset exists) with a counterparty through

arrangements such as netting agreements.

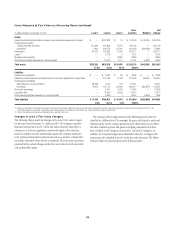

Auction Rate Securities

Auction rate securities (ARS) are long-term municipal bonds, corporate

bonds, securitizations and preferred stocks with interest rates or dividend

yields that are reset through periodic auctions. The coupon paid in the

current period is based on the rate determined by the prior auction. In the

event of an auction failure, ARS holders receive a “fail rate” coupon, which

is specified by the original issue documentation of each ARS.

Where insufficient orders to purchase all of the ARS issue to be sold in an

auction were received, the primary dealer or auction agent would

traditionally have purchased any residual unsold inventory (without a

contractual obligation to do so). This residual inventory would then be

repaid through subsequent auctions, typically in a short timeframe. Due to

this auction mechanism and generally liquid market, ARS have historically

traded and were valued as short-term instruments.

Citigroup acted in the capacity of primary dealer for approximately $72

billion of ARS and continued to purchase residual unsold inventory in

support of the auction mechanism until mid-February 2008. After this date,

liquidity in the ARS market deteriorated significantly, auctions failed due to

a lack of bids from third-party investors, and Citigroup ceased to purchase

unsold inventory. Following a number of ARS refinancings, at December 31,

2008, Citigroup continued to act in the capacity of primary dealer for

approximately $37 billion of outstanding ARS.

The Company classifies its ARS as held-to-maturity, available-for-sale

and trading securities.

Prior to our first auction’s failing in the first quarter of 2008, Citigroup

valued ARS based on observation of auction market prices, because the

auctions had a short maturity period (7, 28 and 35 days). This generally

resulted in valuations at par. Once the auctions failed, ARS could no longer

be valued using observation of auction market prices. Accordingly, the fair

value of ARS is currently estimated using internally developed discounted

cash flow valuation techniques specific to the nature of the assets underlying

each ARS.

For ARS with U.S. municipal securities as underlying assets, future cash

flows are estimated based on the terms of the securities underlying each

individual ARS and discounted at an estimated discount rate in order to

estimate the current fair value. The key assumptions that impact the ARS

valuations are estimated prepayments and refinancings, estimated fail rate

coupons (i.e., the rate paid in the event of auction failure, which varies

according to the current credit rating of the issuer) and the discount rate

used to calculate the present value of projected cash flows. The discount rate

used for each ARS is based on rates observed for straight issuances of other

municipal securities. In order to arrive at the appropriate discount rate, these

observed rates were adjusted upward to factor in the specifics of the ARS

structure being valued, such as callability, and the illiquidity in the ARS

market.

For ARS with student loans as underlying assets, future cash flows are

estimated based on the terms of the loans underlying each individual ARS,

discounted at an appropriate rate in order to estimate the current fair value.

The key assumptions that impact the ARS valuations are the expected

weighted average life of the structure, estimated fail rate coupons, the

amount of leverage in each structure and the discount rate used to calculate

the present value of projected cash flows. The discount rate used for each

ARS is based on rates observed for basic securitizations with similar

maturities to the loans underlying each ARS being valued. In order to arrive

at the appropriate discount rate, these observed rates were adjusted upward to

factor in the specifics of the ARS structure being valued, such as callability,

and the illiquidity in the ARS market.

During the first quarter of 2008, ARS for which the auctions failed and

where no secondary market has developed were moved to Level 3, as the

assets were subject to valuation using significant unobservable inputs. For

ARS which are subject to SFAS 157 classification, the majority continue to be

classified in Level 3.

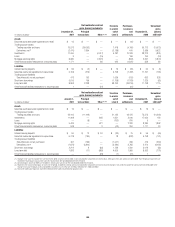

Alt-A Mortgage Securities

The Company classifies its Alt-A mortgage securities as Held-to-Maturity,

Available-for-Sale, and Trading investments. The securities classified as

trading and available-for-sale are recorded at fair value with changes in fair

value reported in current earnings and OCI, respectively. For these purposes,

Alt-A mortgage securities are non-agency residential mortgage-backed

securities (RMBS) where (1) the underlying collateral has weighted average

FICO scores between 680 and 720 or (2) for instances where FICO scores are

greater than 720, RMBS have 30% or less of the underlying collateral

composed of full documentation loans.

Similar to the valuation methodologies used for other trading securities

and trading loans, the Company generally determines the fair value of Alt-A

mortgage securities utilizing internal valuation techniques. Fair-value

estimates from internal valuation techniques are verified, where possible, to

prices obtained from independent vendors. Vendors compile prices from

various sources. Where available, the Company may also make use of quoted

prices for recent trading activity in securities with the same or similar

characteristics to that being valued.

The internal valuation techniques used for Alt-A mortgage securities, as

with other mortgage exposures, consider estimated housing price changes,

unemployment rates, interest rates and borrower attributes. They also

consider prepayment rates as well as other market indicators.

Alt-A mortgage securities that are valued using these methods are

generally classified as Level 2. However, Alt-A mortgage securities backed by

Alt-A mortgages of lower quality or more recent vintages are mostly classified

in Level 3 due to the reduced liquidity that exists for such positions, which

reduces the reliability of prices available from independent sources.

195