Citibank 2008 Annual Report Download - page 109

Download and view the complete annual report

Please find page 109 of the 2008 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

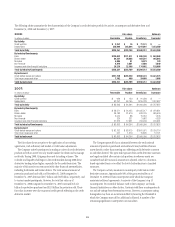

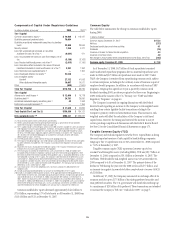

Liquidity Ratios

A series of standard corporate-wide liquidity ratios has been established to

monitor the structural elements of Citigroup’s liquidity. As discussed on page

102, for the Parent and CGMHI, ratios are established for liquid assets

against short-term obligations. For bank entities, key liquidity ratios include

cash capital (defined as core deposits, long-term debt, and capital compared

with illiquid assets), liquid assets against liquidity gaps, core deposits to

loans, and deposits to loans. Several measures exist to review potential

concentrations of funding by individual name, product, industry, or

geography. Triggers for management discussion, which may result in other

actions, have been established against these ratios. In addition, each

individual major operating subsidiary or country establishes targets against

these ratios and may monitor other ratios as approved in its funding and

liquidity plan.

For CGMHI and Bank Entities, one of the key structural liquidity

measures is the cash capital ratio. Cash capital is a broader measure of the

ability to fund the structurally illiquid portion of the Company’s balance

sheet than traditional measures such as deposits to loans or core deposits to

loans. The ratio measures the ability to fund illiquid assets with structurally

long-term funding over one year. At December 31, 2008, both CGMHI and

the aggregate Bank Entities had an excess of structural long-term funding as

compared with their illiquid assets.

Market Triggers

Market triggers are internal or external market or economic factors that may

imply a change to market liquidity or Citigroup’s access to the markets.

Citigroup market triggers are monitored on a weekly basis by the Treasurer

and the head of Risk Architecture and are presented to the FinALCO.

Appropriate market triggers are also established and monitored for each

major operating subsidiary and/or country as part of the funding and

liquidity plans. Local triggers are reviewed with the local country or business

ALCO and independent risk management.

Stress Testing

Simulated liquidity stress testing is periodically performed for each major

operating subsidiary and/or country. A variety of firm-specific and market-

related scenarios are used at the consolidated level and in individual

countries. These scenarios include assumptions about significant changes in

key funding sources, credit ratings, contingent uses of funding, and political

and economic conditions in certain countries. The results of stress tests of

individual countries and operating subsidiaries are reviewed to ensure that

each individual major operating subsidiary or country is either a self-funded

or net provider of liquidity. In addition, a Contingency Funding Plan is

prepared on a periodic basis for Citigroup. The plan includes detailed

policies, procedures, roles and responsibilities, and the results of corporate

stress tests. The product of these stress tests is a series of alternatives that can

be used by the Treasurer in a liquidity event.

During 2008, Citigroup increased the frequency, duration, and severity of

certain stress testing, particularly related to the interconnection of

idiosyncratic and systemic risk. In addition, in conformity with

recommendations made by the Credit Risk Management Policy Group III,

Citigroup instituted a 30-day maximum cash flow for some of its key

operating entities.

CGMHI monitors liquidity by tracking asset levels, collateral and funding

availability to maintain flexibility to meet its financial commitments. As a

policy, CGMHI attempts to maintain sufficient capital and funding sources in

order to have the capacity to finance itself on a fully collateralized basis in

the event that its access to uncollateralized financing is temporarily

impaired. This is documented in CGMHI’s Contingency Funding Plan. This

plan is reviewed periodically to keep the funding options current and in line

with market conditions. The management of this plan includes an analysis

used to determine CGMHI’s ability to withstand varying levels of stress,

including rating downgrades, which could impact its liquidation horizons

and required margins. CGMHI maintains liquidity reserves of cash and

available loan value of unencumbered securities in excess of its outstanding

short-term uncollateralized liabilities. This is monitored on a daily basis.

CGMHI also ensures that long-term illiquid assets are funded with long-term

liabilities.

103