Citibank 2008 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2008 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

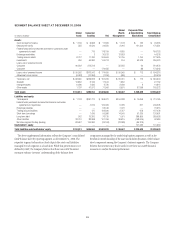

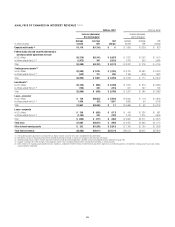

BALANCE SHEET REVIEW

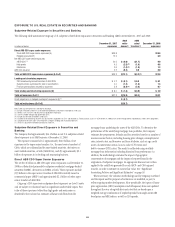

December 31, Increase

(decrease)

%

ChangeIn billions of dollars 2008 2007

Assets

Loans, net of unearned income and allowance for loan losses $ 665 $ 762 $ (97) (13)%

Trading account assets 378 539 (161) (30)

Federal funds sold and securities borrowed or purchased under agreements to resell 184 274 (90) (33)

Investments 256 215 41 19

Other assets 455 397 58 15

Total assets $1,938 $2,187 $(249) (11)%

Liabilities

Deposits $ 774 $ 826 $ (52) (6)%

Federal funds purchased and securities loaned or sold under agreements to repurchase 205 304 (99) (33)

Short-term borrowings and long-term debt 486 574 (88) (15)

Trading account liabilities 167 182 (15) (8)

Other liabilities 164 188 (24) (13)

Total liabilities $1,796 $2,074 $(278) (13)%

Stockholders’ equity $ 142 $ 113 $ 29 26%

Total liabilities and stockholders’ equity $1,938 $2,187 $(249) (11)%

Loans

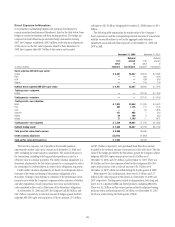

Loans are an extension of credit to individuals, corporations, or government

institutions. Loans vary across regions and industries and primarily include

credit cards, mortgages, other real estate lending, personal loans, auto loans,

student loans, and corporate loans. The majority of loans are carried at cost

with a minimal amount recorded at fair value in accordance with SFAS 155

and SFAS 159.

Consumer and corporate loans comprised 75% and 25%, respectively, of

total loans (net of unearned income and before the allowance for loan

losses).

During 2008 consumer loans decreased by $83 billion, or 14%, primarily

due to:

• $39 billion, or 14%, decrease in installment and revolving credit; and

• $29 billion, or 10%, decrease in mortgage and real estate loans.

These decreases were partially driven by the sales of CitiCapital and the

German retail banking units. Foreign exchange translation also factored

into the decrease in loans, as a number of currencies weakened against the

dollar.

During 2008 corporate loans decreased $15 billion, or 8%, primarily

driven by a decrease of $10 billion, or 7%, in commercial and industrial

loans.

During 2008, average consumer loans (net of unearned income) of

$551 billion yielded an average rate of 8.6%, compared to $523 billion and

9.0% in the prior year. Average corporate loans of $184 billion yielded an

average rate of 8.2% in 2008, compared to $188 billion and 8.5% in the

prior year.

For further information, see “Loans Outstanding” on page 53 and

Note 17 to the Consolidated Financial Statements on page 163.

Trading Account Assets (Liabilities)

Trading account assets include debt and marketable equity securities,

derivatives in a receivable position, residual interests in securitizations, and

physical commodities inventory. In addition, certain assets that Citigroup

has elected to carry at fair value under SFAS 155 and SFAS 159, such as

certain loans and purchase guarantees, are also included in trading account

assets. Trading account liabilities include securities sold, not yet purchased

(short positions) and derivatives in a net payable position as well as certain

liabilities that Citigroup has elected to carry at fair value under SFAS 155 and

SFAS 159.

All trading account assets and liabilities are reported at their fair value,

except for physical commodities inventory which is carried at the lower of cost

or market, with unrealized gains and losses recognized in current income.

During 2008 trading account assets decreased by $161 billion, or 30%,

due to:

• $127 billion, or 70%, decrease in corporate and other debt securities,

driven by a decrease in the SIV assets, a decrease in commercial paper

trading assets and the transfer of trading assets to investments

held-to-maturity and available-for-sale (see “Reclassification of

Financial Assets” on page 87);

• $58 billion, or 55%, decrease in equity securities;

• $35 billion, or 62%, decrease in mortgage loans and collateralized

mortgage securities (CMOs); and

• $9 billion, or 49%, decrease in state and municipal securities;

offset by:

• $38 billion, or 50%, increase in revaluation gains primarily consisting of

increases from interest rates, foreign exchange and credit derivative

contracts, offset by an increase in netting permitted under master netting

agreements;

78