Citibank 2008 Annual Report Download - page 195

Download and view the complete annual report

Please find page 195 of the 2008 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

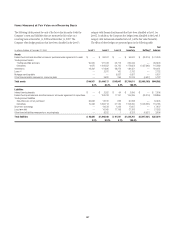

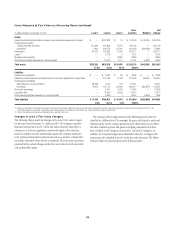

|

|

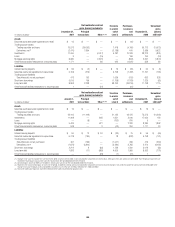

24. DERIVATIVES ACTIVITIES

In the ordinary course of business, Citigroup enters into various types of

derivative transactions. These derivative transactions include:

•Futures and forward contracts which are commitments to buy or sell at

a future date a financial instrument, commodity or currency at a

contracted price and may be settled in cash or through delivery.

•Swap contracts which are commitments to settle in cash at a future date

or dates that may range from a few days to a number of years, based on

differentials between specified financial indices, as applied to a notional

principal amount.

•Option contracts which give the purchaser, for a fee, the right, but not

the obligation, to buy or sell within a limited time a financial instrument,

commodity or currency at a contracted price that may also be settled in

cash, based on differentials between specified indices or prices.

Citigroup enters into these derivative contracts for the following reasons:

•Trading Purposes—Customer Needs – Citigroup offers its customers

derivatives in connection with their risk-management actions to transfer,

modify or reduce their interest rate, foreign exchange and other market/

credit risks or for their own trading purposes. As part of this process,

Citigroup considers the customers’ suitability for the risk involved, and

the business purpose for the transaction. Citigroup also manages its

derivative-risk positions through offsetting trade activities, controls

focused on price verification, and daily reporting of positions to senior

managers.

•Trading Purposes—Own Account – Citigroup trades derivatives for its

own account. Trading limits and price verification controls are key

aspects of this activity.

•Asset/Liability Management Hedging—Citigroup uses derivatives in

connection with its risk-management activities to hedge certain risks or

reposition the risk profile of the Company. For example, Citigroup may

issue fixed-rate long-term debt and then enter into a receive-fixed,

pay-variable-rate interest rate swap with the same tenor and notional

amount to convert the interest payments to a net variable-rate basis. This

strategy is the most common form of an interest rate hedge, as it

minimizes interest cost in certain yield curve environments. Derivatives

are also used to manage risks inherent in specific groups of on-balance

sheet assets and liabilities, including investments, corporate and

consumer loans, deposit liabilities, as well as other interest-sensitive assets

and liabilities. In addition, foreign- exchange contracts are used to hedge

non-U.S. dollar denominated debt, available-for-sale securities, net

capital exposures and foreign-exchange transactions.

Derivatives may expose Citigroup to market, credit or liquidity risks in

excess of the amounts recorded on the Consolidated Balance Sheet. Market

risk on a derivative product is the exposure created by potential fluctuations

in interest rates, foreign-exchange rates and other values and is a function of

the type of product, the volume of transactions, the tenor and terms of the

agreement, and the underlying volatility. Credit risk is the exposure to loss in

the event of nonperformance by the other party to the transaction where the

value of any collateral held is not adequate to cover such losses. The

recognition in earnings of unrealized gains on these transactions is subject

to management’s assessment as to collectibility. Liquidity risk is the potential

exposure that arises when the size of the derivative position may not be able

to be rapidly adjusted in periods of high volatility and financial stress at a

reasonable cost.

Accounting for Derivative Hedging

Citigroup accounts for its hedging activities in accordance with SFAS 133. As

a general rule, SFAS 133 hedge accounting is permitted for those situations

where the Company is exposed to a particular risk, such as interest-rate or

foreign-exchange risk, that causes changes in the fair value of an asset or

liability, or variability in the expected future cash flows of an existing asset,

liability or a forecasted transaction that may affect earnings.

Derivative contracts hedging the risks associated with the changes in fair

value are referred to as fair value hedges, while contracts hedging the risks

affecting the expected future cash flows are called cash flow hedges. Hedges

that utilize derivatives or debt instruments to manage the foreign exchange

risk associated with equity investments in non-U.S. dollar functional

currency foreign subsidiaries (net investment in a foreign operation) are

called net investment hedges.

All derivatives are reported on the balance sheet at fair value. In addition,

where applicable, all such contracts covered by master netting agreements

are reported net. Gross positive fair values are netted with gross negative fair

values by counterparty pursuant to a valid master netting agreement. In

addition, payables and receivables in respect of cash collateral received from

or paid to a given counterparty are included in this netting. However,

non-cash collateral is not included.

As of December 31, 2008 and December 31, 2007, the amount of payables

in respect of cash collateral received that was netted with unrealized gains

from derivatives was $52 billion and $26 billion, respectively, while the

amount of receivables in respect of cash collateral paid that was netted with

unrealized losses from derivatives was $58 billion and $37 billion,

respectively.

If certain hedging criteria specified in SFAS 133 are met, including testing

for hedge effectiveness, special hedge accounting may be applied. The hedge-

effectiveness assessment methodologies for similar hedges are performed in a

similar manner and are used consistently throughout the hedging

relationships. For fair value hedges, the changes in value of the hedging

derivative, as well as the changes in value of the related hedged item, due to

the risk being hedged, are reflected in current earnings. For cash flow hedges

and net investment hedges, the changes in value of the hedging derivative

are reflected in Accumulated other comprehensive income (loss) in

Stockholders’ equity, to the extent the hedge was effective. Hedge

ineffectiveness, in either case, is reflected in current earnings.

For asset/liability management hedging, the fixed-rate long-term debt

may be recorded at amortized cost under current U.S. GAAP. However, by

electing to use SFAS 133 hedge accounting, the carrying value of the debt is

adjusted for changes in the benchmark interest rate, with any such changes

in value recorded in current earnings. The related interest-rate swap is also

recorded on the balance sheet at fair value, with any changes in fair value

reflected in earnings. Thus, any ineffectiveness resulting from the hedging

relationship is recorded in current earnings. Alternatively, an economic

hedge, which does not meet the SFAS 133 hedging criteria, would involve

only recording the derivative at fair value on the balance sheet, with its

associated changes in fair value recorded in earnings. The debt would

continue to be carried at amortized cost and, therefore, current earnings

would be impacted only by the interest rate shifts that cause the change in

189