Citibank 2008 Annual Report Download - page 27

Download and view the complete annual report

Please find page 27 of the 2008 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

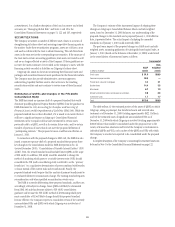

GOODWILL

Citigroup has recorded on its Consolidated Balance Sheet Goodwill of $27.1

billion (approximately 1.4% of assets) and $41.1 billion (approximately

1.9% of assets) at December 31, 2008 and December 31, 2007, respectively.

The December 31, 2008 balance is net of a $9.6 billion goodwill impairment

charge recorded as a result of testing performed as of December 31, 2008.

The impairment is composed of $5.1 billion pretax charge ($4.5 billion after

tax) related to North America Consumer Banking, $4.3 billion pretax

charge ($4.1 billion after tax) related to Latin America Consumer

Banking, and $0.2 billion pre-tax charge ($0.1 billion after tax) related to

EMEA Consumer Banking.

The primary cause for the goodwill impairment in the above reporting

units was the rapid deterioration in the financial markets as well as in the

global economic outlook particularly during the period beginning

mid-November through year end 2008. This deterioration further weakened

the near-term prospects for the financial services industry. These and other

factors, including the increased possibility of further government

intervention, also resulted in the decline in the Company’s market

capitalization from approximately $90 billion at July 1, 2008 and

approximately $74 billion at October 31, 2008 to approximately $36 billion

at December 31, 2008.

The following summary describes Citigroup’s process for accounting for

goodwill and testing for impairment.

Goodwill is allocated to the reporting units at the date the goodwill is

initially recorded. Once goodwill has been allocated to the reporting units, it

generally no longer retains its identification with a particular acquisition,

but instead becomes identified with the reporting unit as a whole. As a result,

all of the fair value of each reporting unit is available to support the value of

goodwill allocated to the unit. As of December 31, 2008, the Company

operated in four core business segments as discussed on page 138. Goodwill

impairment testing is performed at the reporting unit level, one level below

the business segment.

The changes in the management structure during 2008 resulted in the

creation of new business segments. As a result, commencing with the third

quarter of 2008, the Company identified new reporting units as required

under SFAS No. 142, Goodwill and Other Intangible Assets (SFAS 142).

Goodwill affected by the change was reallocated from the previous seven

reporting units to ten new reporting units, using a relative fair value

approach. The ten new reporting units, which remain unchanged at

December 31, 2008, are Securities and Banking, Global Transaction Services,

International Wealth Management, N.A. Wealth Management, North

America Consumer Banking, N.A. Cards, EMEA Consumer Banking,

Latin America Consumer Banking,Asia Consumer Banking and

International Cards.

Under SFAS 142, the goodwill impairment analysis is done in two steps.

The first step requires a comparison of the fair value of the individual

reporting unit to its carrying value including goodwill. If the fair value of the

reporting unit is in excess of the carrying value, the related goodwill is

considered not to be impaired and no further analysis is necessary. If the

carrying value of the reporting unit exceeds the fair value, there is an

indication of potential impairment and a second step of testing is performed

to measure the amount of impairment, if any, for that reporting unit.

When required, the second step of testing involves calculating the implied

fair value of goodwill for each of the affected reporting units. The implied

fair value of goodwill is determined in the same manner as the amount of

goodwill recognized in a business combination, which is the excess of the

fair value of the reporting unit determined in step one over the fair value of

the net assets and identifiable intangibles as if the reporting unit were being

acquired. If the amount of the goodwill allocated to the reporting unit

exceeds the implied fair value of the goodwill in the pro forma purchase

price allocation, an impairment charge is recorded for the excess. An

impairment charge recognized cannot exceed the amount of goodwill

allocated to a reporting unit and cannot be reversed subsequently even if the

fair value of the reporting unit recovers.

Goodwill impairment testing involves management judgment, requiring

an assessment of whether the carrying value of the reporting unit can be

supported by the fair value of the individual reporting unit using widely

accepted valuation techniques, such as the market approach (earnings

multiples and/or transaction multiples) and/or discounted cash flow

methods (DCF). In applying these methodologies the Company utilizes a

number of factors, including actual operating results, future business plans,

economic projections and market data. A combination of methodologies is

used and weighted appropriately for reporting units with significant adverse

changes in business climate. Management may engage an independent

valuation specialist to assist in the Company’s valuation process.

Prior to 2008, the Company primarily employed the market approach for

estimating fair value of the reporting units. As a result of significant adverse

changes during 2008 in certain of the Company’s reporting units and the

increase in financial sector volatility primarily in the U.S., the Company

engaged the services of an independent valuation specialist to assist in the

Company’s valuation of the following reporting units—Securities and

Banking, North America Consumer Banking,Latin America Consumer

Banking and N.A. Cards. The DCF method was incorporated to ensure

reliability of results. The Company believes that the DCF method, using

management projections for the selected reporting units and an appropriate

risk-adjusted discount rate is most reflective of a market participant’s view of

fair values given current market conditions. For the reporting units where

both methods were utilized in 2008, the resulting fair values were relatively

consistent and appropriate weighting was given to outputs from both

methods.

The DCF method used at the time of each impairment test used discount

rates that the Company believes adequately reflected the risk and uncertainty

in the financial markets generally and specifically in the internally

generated cash flow projections. The DCF method employs a capital asset

pricing model in estimating the discount rate. The Company continues to

value the remaining reporting units where it believes the risk of impairment

to be low using primarily the market approach.

21