Citibank 2008 Annual Report Download - page 188

Download and view the complete annual report

Please find page 188 of the 2008 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

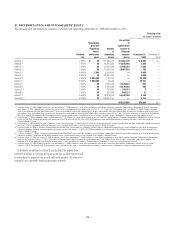

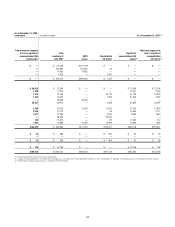

Mortgage Servicing Rights

The fair value of capitalized mortgage loan servicing rights (MSR) was $5.7

billion and $8.4 billion at December 31, 2008 and 2007, respectively. The

MSRs correspond to principal loan balances of $662 billion and $586 billion

as of December 31, 2008 and 2007, respectively. The following table

summarizes the changes in capitalized MSRs:

In millions of dollars 2008 2007

Balance, beginning of year $ 8,380 $ 5,439

Originations 1,311 1,843

Purchases 13,678

Changes in fair value of MSRs due to changes in inputs and

assumptions (2,682) (247)

Transfer to Trading account assets (163) (1,026)

Other changes (1) (1,190) (1,307)

Balance, end of year $ 5,657 $ 8,380

(1) Represents changes due to customer payments and passage of time.

The market for MSRs is not sufficiently liquid to provide participants with

quoted market prices. Therefore, the Company uses an option-adjusted

spread valuation approach to determine the fair value of MSRs. This

approach consists of projecting servicing cash flows under multiple interest

rate scenarios and discounting these cash flows using risk-adjusted discount

rates. The key assumptions used in the valuation of MSRs include mortgage

prepayment speeds and discount rates. The model assumptions and the

MSR’s fair value estimates are compared to observable trades of similar MSR

portfolios and interest-only security portfolios, as available, as well as to MSR

broker valuations and industry surveys. The cash flow model and underlying

prepayment and interest rate models used to value these MSRs are subject to

validation in accordance with the Company’s model validation policies.

The fair value of the MSRs is primarily affected by changes in

prepayments that result from shifts in mortgage interest rates. In managing

this risk, the Company economically hedges a significant portion of the

value of its MSRs through the use of interest rate derivative contracts,

forward purchase commitments of mortgage-backed securities and

purchased securities classified as trading.

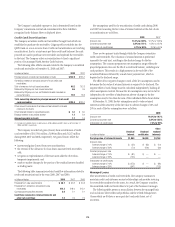

The Company receives fees during the course of servicing previously

securitized mortgages. The amount of these fees for the years ending

December 31, were as follows:

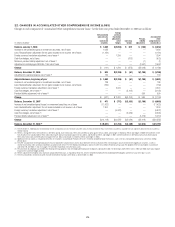

In millions of dollars 2008 2007 2006

Servicing fees $2,121 $1,683 $1,036

Late fees 123 90 56

Ancillary fees 81 61 45

Total MSR fees $2,325 $1,834 $1,137

These fees are classified in the Consolidated Statement of Income as

Commissions and fees.

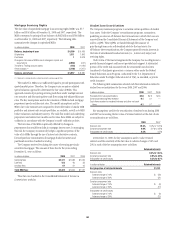

Student Loan Securitizations

The Company maintains programs to securitize certain portfolios of student

loan assets. Under the Company’s securitization programs, transactions

qualifying as sales are off-balance sheet transactions in which the loans are

removed from the Consolidated Financial Statements of the Company and

sold to a QSPE. These QSPEs are funded through the issuance of

pass-through term notes collateralized solely by the trust assets. For

off-balance sheet securitizations, the Company generally retains interests in

the form of subordinated residual interests (i.e., interest-only strips) and

servicing rights.

Under terms of the trust arrangements the Company has no obligations to

provide financial support and has not provided such support. A substantial

portion of the credit risk associated with the securitized loans has been

transferred to third party guarantors or insurers either under the Federal

Family Education Loan Program, authorized by the U.S. Department of

Education under the Higher Education Act of 1965, as amended, or private

credit insurance.

The following table summarizes selected cash flow information related to

student loan securitizations for the years 2008, 2007 and 2006:

In billions of dollars 2008 2007 2006

Proceeds from new securitizations $2.0 $2.9 $7.6

Contractual servicing fees received 0.1 0.1 —

Cash flows received on retained interests and other net cash

flows 0.1 0.1 —

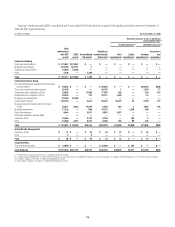

Key assumptions used for the securitization of student loans during 2008

and 2007 in measuring the fair value of retained interests at the date of sale

or securitization are as follows:

2008 2007

Discount rate 10.6% 5.9% to 10.5%

Constant prepayment rate 9.0% 3.1% to 3.8%

Anticipated net credit losses 0.5% 0.3%

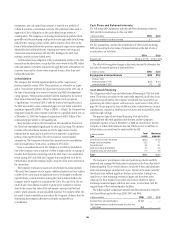

At December 31, 2008, the key assumptions used to value retained

interests and the sensitivity of the fair value to adverse changes of 10% and

20% in each of the key assumptions were as follows:

Retained interests

Discount rate 3.9% to 13.4%

Constant prepayment rate 0.8% to 8.9%

Anticipated net credit losses 0.3% to 0.7%

In millions of dollars Retained interests

Carrying value of retained interests $1,151

Discount rates

Adverse change of 10% $ (26)

Adverse change of 20% (51)

Constant prepayment rate

Adverse change of 10% $ (9)

Adverse change of 20% (17)

Anticipated net credit losses

Adverse change of 10% $ (6)

Adverse change of 20% (13)

182