Citibank 2008 Annual Report Download - page 200

Download and view the complete annual report

Please find page 200 of the 2008 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

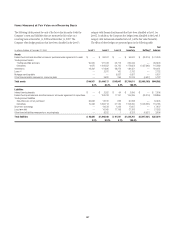

|

|

value of these exposures (other than high grade and mezzanine as described

below) is based on estimates of future cash flows from the mortgage loans

underlying the assets of the ABS CDOs. To determine the performance of the

underlying mortgage loan portfolios, the Company estimates the

prepayments, defaults and loss severities based on a number of

macroeconomic factors, including housing price changes, unemployment

rates, interest rates and borrower and loan attributes, such as age, credit

scores, documentation status, loan-to-value (LTV) ratios and debt-to-income

(DTI) ratios. The model is calibrated using available mortgage loan

information including historical loan performance. In addition, the

methodology estimates the impact of geographic concentration of mortgages

and the impact of reported fraud in the origination of subprime mortgages.

An appropriate discount rate is then applied to the cash flows generated for

each ABCP and CDO-squared tranche, in order to estimate its current fair

value.

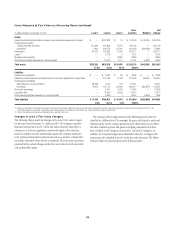

When necessary, the valuation methodology used by Citigroup is refined

and the inputs used for the purposes of estimation are modified, in part, to

reflect ongoing market developments. More specifically, the inputs of home

price appreciation (HPA) assumptions and delinquency data were updated

during the fourth quarter along with discount rates that are based upon a

weighted average combination of implied spreads from single name ABS

bond prices and ABX indices, as well as CLO spreads.

Beginning with the third quarter of 2008, the Company used the Loan

Performance Index to estimate the impact of housing price changes.

Previously, it incorporated the S&P/Case-Shiller Index. This change was

made because the Loan Performance Index provided more comprehensive

geographic data. In addition, the Company’s mortgage default model uses

recent mortgage performance data, a period of sharp home price declines

and high levels of mortgage foreclosures.

The valuation as of December 31, 2008 assumes a cumulative decline in

U.S. housing prices from peak to trough of 33%. This rate assumes declines

of 16% and 13% in 2008 and 2009, respectively, the remainder of the 33%

decline having already occurred before the end of 2007.

In addition, during the last three quarters of 2008, the discount rates were

based on a weighted average combination of the implied spreads from single

name ABS bond prices, ABX indices and CLO spreads, depending on vintage

and asset types. To determine the discount margin, the Company applies the

mortgage default model to the bonds underlying the ABX indices and other

referenced cash bonds and solves for the discount margin that produces the

market prices of those instruments.

Starting in the third quarter of 2008, the valuation of the high grade and

mezzanine ABS CDO positions was changed from model valuation to trader

prices based on the underlying assets of each high grade and mezzanine ABS

CDO. Unlike the ABCP and CDO-squared positions, the high grade and

mezzanine positions are now largely hedged through the ABX and bond

short positions, which are, by necessity, trader priced. Thus, this change

brings closer symmetry in the way these long and short positions are valued

by the Company. Citigroup intends to use trader marks to value this portion

of the portfolio going forward so long as it remains largely hedged.

The primary drivers that currently impact the super senior valuations are

the discount rates used to calculate the present value of projected cash flows

and projected mortgage loan performance.

Given the above, the Company’s CDO super senior subprime direct

exposures were classified in Level 3 of the fair-value hierarchy.

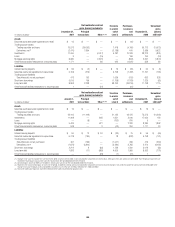

For most of the lending and structuring direct subprime exposures

(excluding super seniors), fair value is determined utilizing observable

transactions where available, other market data for similar assets in markets

that are not active and other internal valuation techniques.

Investments

The investments category includes available-for-sale debt and marketable

equity securities, whose fair value is determined using the same procedures

described for trading securities above or, in some cases, using vendor prices

as the primary source.

Also included in investments are nonpublic investments in private equity

and real estate entities held by the S&B business. Determining the fair value

of nonpublic securities involves a significant degree of management

resources and judgment as no quoted prices exist and such securities are

generally very thinly traded. In addition, there may be transfer restrictions on

private equity securities. The Company uses an established process for

determining the fair value of such securities, using commonly accepted

valuation techniques, including the use of earnings multiples based on

comparable public securities, industry-specific non-earnings-based multiples

and discounted cash flow models. In determining the fair value of nonpublic

securities, the Company also considers events such as a proposed sale of the

investee company, initial public offerings, equity issuances, or other

observable transactions.

Private equity securities are generally classified in Level 3 of the fair-value

hierarchy.

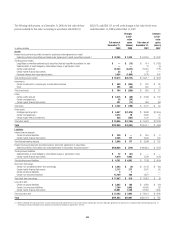

Short-Term Borrowings and Long-Term Debt

Where fair-value accounting has been elected, the fair value of

non-structured liabilities is determined by discounting expected cash flows

using the appropriate discount rate for the applicable maturity. Such

instruments are generally classified in Level 2 of the fair-value hierarchy as

all inputs are readily observable.

The Company determines the fair value of structured liabilities (where

performance is linked to structured interest rates, inflation or currency risks)

and hybrid financial instruments (performance linked to risks other than

interest rates, inflation or currency risks) using the appropriate derivative

valuation methodology (described above) given the nature of the embedded

risk profile. Such instruments are classified in Level 2 or Level 3 depending

on the observability of significant inputs to the model.

Market Valuation Adjustments

Liquidity adjustments are applied to items in Level 2 and Level 3 of the fair-

value hierarchy to ensure that the fair value reflects the price at which the

entire position could be liquidated. The liquidity reserve is based on the

bid-offer spread for an instrument, adjusted to take into account the size of

the position.

Counterparty credit-risk adjustments are applied to derivatives, such as

over-the-counter derivatives, where the base valuation uses market

parameters based on the LIBOR interest rate curves. Not all counterparties

have the same credit risk as that implied by the relevant LIBOR curve, so it is

necessary to consider the market view of the credit risk of a counterparty in

order to estimate the fair value of such an item.

Bilateral or “own” credit-risk adjustments are applied to reflect the

Company’s own credit risk when valuing derivatives and liabilities measured

at fair value, in accordance with the requirements of SFAS 157.

194