Citibank 2015 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2015 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

|

|

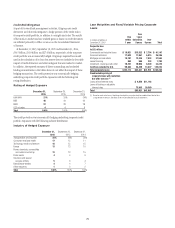

73

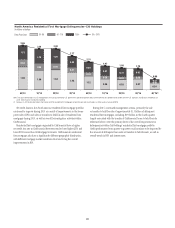

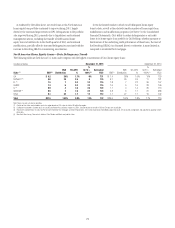

As evidenced by the tables above, net credit losses in the North America

home equity loan portfolio continued to improve during 2015, largely

driven by the continued improvement in HPI. Delinquencies in the portfolio

also improved during 2015, primarily due to liquidations and continued

management actions, including the transfer of CitiFinancial home

equity loans to held-for-sale in the fourth quarter of 2015 and continued

modifications, partially offset by increased delinquencies associated with the

increase in Revolving HELOCs commencing amortization.

Given the limited market in which to sell delinquent home equity

loans to date, as well as the relatively smaller number of home equity loan

modifications and modification programs (see Note 15 to the Consolidated

Financial Statements), Citi’s ability to reduce delinquencies or net credit

losses in its home equity loan portfolio in Citi Holdings, whether pursuant to

deterioration of the underlying credit performance of these loans, the reset of

the Revolving HELOCs (as discussed above) or otherwise, is more limited as

compared to residential first mortgages.

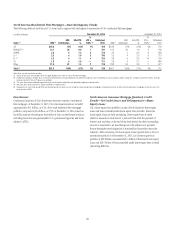

North America Home Equity Loans—State Delinquency Trends

The following tables set forth the six U.S. states and/or regions with the highest concentration of Citi’s home equity loans:

In billions of dollars December 31, 2015 December 31, 2014

State (1) ENR (2)

ENR

Distribution

90+DPD

%

%

CLTV >

100% (3)

Refreshed

FICO ENR (2)

ENR

Distribution

90+DPD

%

%

CLTV >

100% (3)

Refreshed

FICO

CA $ 6.2 29% 1.7% 6% 731 $ 7.4 28% 1.5% 10% 729

NY/NJ/CT (4) 6.0 28 2.5 8 725 6.7 25 2.4 11 721

FL (4) 1.5 7 2.0 24 715 1.8 7 2.2 36 707

VA/MD 1.3 6 2.0 23 715 1.6 6 1.6 28 706

IL (4) 0.9 4 1.6 29 722 1.1 4 1.4 35 716

IN/OH/MI (4) 0.5 3 1.9 24 703 0.8 3 1.7 31 688

Other 5.1 24 1.7 12 712 7.1 27 1.7 19 702

Total $21.5 100% 2.0% 12% 722 $26.6 100% 1.8% 17% 715

Note: Totals may not sum due to rounding.

(1) Certain of the states are included as part of a region based on Citi’s view of similar HPI within the region.

(2) Ending net receivables. Excludes loans in Canada and Puerto Rico and loans subject to LTSCs. Excludes balances for which FICO or LTV data are unavailable.

(3) Represents combined loan-to-value (CLTV) for both residential first mortgages and home equity loans. CLTV ratios (loan balance divided by appraised value) are calculated at origination and updated by applying market

price data.

(4) New York, New Jersey, Connecticut, Indiana, Ohio, Florida and Illinois are judicial states.