Citibank 2015 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2015 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

|

|

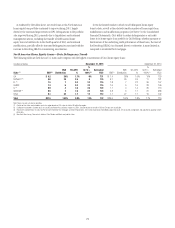

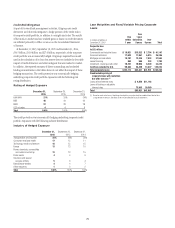

70

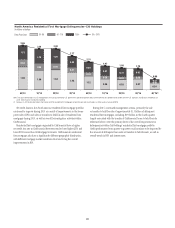

North America Residential First Mortgages—State Delinquency Trends

The following tables set forth the six U.S. states and/or regions with the highest concentration of Citi’s residential first mortgages.

In billions of dollars December 31, 2015 December 31, 2014

State (1) ENR (2)

ENR

Distribution

90+DPD

%

%

LTV >

100% (3)

Refreshed

FICO ENR (2)

ENR

Distribution

90+DPD

%

%

LTV >

100% (3)

Refreshed

FICO

CA $19.2 37% 0.2% 1% 754 $18.9 31% 0.6% 2% 745

NY/NJ/CT (4) 12.7 25 0.8 1 751 12.2 20 1.9 2 740

VA/MD 2.2 4 1.2 2 719 3.0 5 3.0 8 695

IL (4) 2.2 4 1.0 3 735 2.5 4 2.5 9 713

FL (4) 2.2 4 1.1 4 723 2.8 5 3.0 14 700

TX 1.9 4 1.0 — 711 2.5 4 2.7 — 680

Other 11.0 21 1.3 2 710 18.2 30 3.3 7 677

Total (5) $51.5 100% 0.7% 1% 738 $60.1 100% 2.1% 4% 715

Note: Totals may not sum due to rounding.

(1) Certain of the states are included as part of a region based on Citi’s view of similar HPI within the region.

(2) Ending net receivables. Excludes loans in Canada and Puerto Rico, loans guaranteed by U.S. government agencies, loans recorded at fair value and loans subject to long term standby commitments (LTSCs). Excludes

balances for which FICO or LTV data are unavailable.

(3) LTV ratios (loan balance divided by appraised value) are calculated at origination and updated by applying market price data.

(4) New York, New Jersey, Connecticut, Florida and Illinois are judicial states.

(5) Improvement in state trends during 2015 was primarily due to the sale or transfer to held-for-sale of residential first mortgages, including the transfer of CitiFinancial residential first mortgages to held-for-sale in the

fourth quarter of 2015.

Foreclosures

A substantial majority of Citi’s foreclosure inventory consists of residential

first mortgages. At December 31, 2015, Citi’s foreclosure inventory included

approximately $0.1 billion, or 0.2%, of the total residential first mortgage

portfolio, compared to $0.6 billion, or 0.9%, at December 31, 2014, based on

the dollar amount of ending net receivables of loans in foreclosure inventory,

excluding loans that are guaranteed by U.S. government agencies and loans

subject to LTSCs.

North America Consumer Mortgage Quarterly Credit

Trends—Net Credit Losses and Delinquencies—Home

Equity Loans

Citi’s home equity loan portfolio consists of both fixed-rate home equity

loans and loans extended under home equity lines of credit. Fixed-rate

home equity loans are fully amortizing. Home equity lines of credit

allow for amounts to be drawn for a period of time with the payment of

interest only and then, at the end of the draw period, the then-outstanding

amount is converted to an amortizing loan (the interest-only payment

feature during the revolving period is standard for this product across the

industry). After conversion, the home equity loans typically have a 20-year

amortization period. As of December 31, 2015, Citi’s home equity loan

portfolio of $22.8 billion consisted of $6.3 billion of fixed-rate home equity

loans and $16.5 billion of loans extended under home equity lines of credit

(Revolving HELOCs).