Citibank 2015 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2015 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

|

|

72

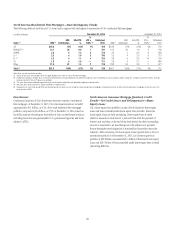

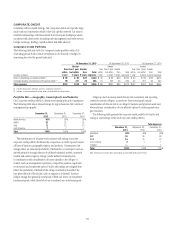

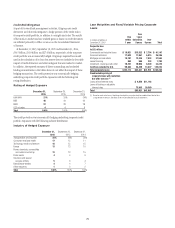

Approximately 6.7% of the Revolving HELOCs that have begun

amortization as of December 31, 2015 were 30+ days past due, compared

to 3.2% of the total outstanding home equity loan portfolio (amortizing

and non-amortizing). This compared to 6.4% and 2.7%, respectively, as

of December 31, 2014. As newly amortizing loans continue to season, the

delinquency rate of the amortizing Revolving HELOC portfolio and total

home equity loan portfolio is expected to continue to increase. In addition,

resets to date have generally occurred during a period of historically low

interest rates, which Citi believes has likely reduced the overall “payment

shock” to the borrower.

Citi continues to monitor this reset risk closely and will continue to

consider any potential impact in determining its allowance for loan loss

reserves. In addition, management continues to review and take additional

actions to offset potential reset risk, such as a borrower outreach program to

provide reset risk education and proactively working with high-risk borrowers

through a specialized single point of contact unit. For further information on

reset risk, see “Risk Factors—Credit and Market Risks” above.

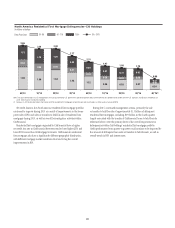

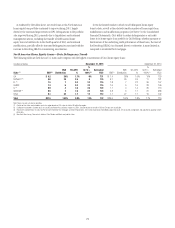

Net Credit Losses and Delinquencies

The following charts detail the quarterly credit trends for Citi’s home equity

loan portfolio in North America:

4Q’153Q’152Q’151Q’154Q’14

25 24 23 22

19

North America Home Equity

—EOP Loans

In billions of dollars

Citi Holdings Citicorp

$28 $27 $26

$23

$25

3334

4

4Q’153Q’152Q’151Q’154Q’14

87

1

81

2

71

2

61

1

56

2

North America Home Equity—Net Credit Losses

In millions of dollars

Citi Holdings Citicorp

$88 $83 $72 $58

$62

Total NCL Rate 1.2% 1.2% 1.1% 1.0% 0.9%

Citi Holdings 1.4% 1.3% 1.2% 1.1% 1.1%

Citicorp 0.2% 0.2% 0.2% 0.1% 0.2%

Note: Totals may not sum due to rounding.

North America Home Equity Loan Delinquencies—Citi Holdings

In billions of dollars

Days Past Due: 30+ DPD180+90-17930-89

4Q’153Q’152Q’151Q’154Q’143Q’142Q’141Q’144Q’13

0.42 0.35 0.34 0.33 0.32 0.27 0.27 0.31 0.27

0.25

0.23 0.21 0.20 0.19 0.18 0.16 0.16 0.15

0.33

0.32 0.31 0.30 0.31 0.31 0.30 0.27

0.29

1.00

0.89 0.85 0.84 0.82

0.75 0.73 0.75 0.69

Note: Totals may not sum due to rounding.