Citibank 2015 Annual Report Download - page 130

Download and view the complete annual report

Please find page 130 of the 2015 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

|

|

112

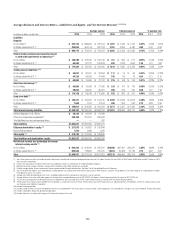

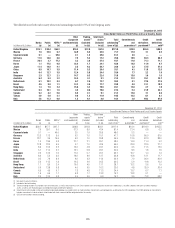

Emerging Markets Trading Account Assets and Investment

Securities

In the ordinary course of business, Citi holds securities in its trading accounts

and investment accounts, including those above. Trading account assets are

marked to market daily, with asset levels varying as Citi maintains inventory

consistent with customer needs. Investment securities are recorded at either

fair value or historical cost, based on the underlying accounting treatment,

and are predominantly held as part of the local entity asset and liability

management program or to comply with local regulatory requirements.

In the markets in the table above, approximately 99% of Citi’s investment

securities were related to sovereign issuers as of December 31, 2015.

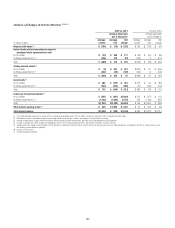

Emerging Markets Consumer Lending

GCB’s strategy within the emerging markets is consistent with GCB’s overall

strategy, which is to leverage its global footprint to serve its target clients.

The retail bank seeks to be the preeminent bank for the emerging affluent

and affluent consumers in large urban centers. In credit cards and in certain

retail markets, Citi serves customers in a somewhat broader set of segments

and geographies. Commercial banking generally serves small- and middle-

market enterprises operating in GCB’s geographic markets, focused on clients

that value Citi’s global capabilities. Overall, Citi believes that its customers

are more resilient than the overall market under a wide range of economic

conditions. Citi’s consumer business has a well-established risk appetite

framework across geographies and products that reflects the business strategy

and activities and establishes boundaries around the key risks that arise from

the strategy and activities.

As of December 31, 2015, GCB had approximately $110 billion of

consumer loans outstanding to borrowers in the emerging markets, or

approximately 38% of GCB’s total loans, largely unchanged from September

30, 2015 and compared to $118 billion (41%) as of December 31, 2014.

Of the approximate $110 billion as of December 31, 2015, the five largest

emerging markets—Mexico, Korea, Singapore, Hong Kong and Taiwan—

comprised approximately 27% of GCB’s total loans. Within the emerging

markets, 30% of Citi’s GCB loans were mortgages, 26% were commercial

markets loans, 24% were personal loans and 20% were credit card loans, each

as of December 31, 2015.

Overall consumer credit quality remained generally stable in the fourth

quarter of 2015, as net credit losses in the emerging markets were 1.9%

of average loans, compared to 1.8% and 2.2% in the third quarter of 2015

and fourth quarter of 2014, respectively, consistent with Citi’s target market

strategy and risk appetite framework. The increase in net credit losses

in certain emerging market countries in Asia, such as Hong Kong and

Indonesia, primarily related to Citi’s commercial banking business in such

countries and was primarily due to the impact of lower commodity prices as

well as the slowdown in growth in the region. The increase in net credit losses

in Brazil also related to the commercial banking business and largely related

to a wind-down portfolio in Brazil, where the losses were mostly offset by the

release of previously-established loan loss reserves.

Emerging Markets Corporate Lending

Consistent with ICG’s overall strategy, Citi’s corporate clients in the emerging

markets are typically large, multinational corporations that value Citi’s

global network. Citi aims to establish relationships with these clients that

encompass multiple products, consistent with client needs, including

cash management and trade services, foreign exchange, lending, capital

markets and M&A advisory. Citi believes that its target corporate segment

is more resilient under a wide range of economic conditions, and that

its relationship-based approach to client service enables it to effectively

manage the risks inherent in such relationships. Citi has a well-established

risk appetite framework around its corporate lending activities, including

risk-based limits and approval authorities and portfolio concentration

boundaries.

As of December 31, 2015, corporate loans (excluding the private bank)

were approximately $93 billion in the emerging markets, representing

approximately 43% of total corporate loans outstanding, compared to

$97 billion (43%) and $99 billion (47%) as of September 30, 2015 and

December 31, 2014, respectively. No single emerging markets country

accounted for more than 6% of Citi’s corporate loans as of the end of the

fourth quarter of 2015.

As of December 31, 2015, approximately 75% of Citi’s emerging markets

corporate credit portfolio (excluding the private bank), including loans

and unfunded lending commitments, was rated investment grade, which

Citi considers to be ratings of BBB or better according to its internal risk

measurement system and methodology (for additional information on Citi’s

internal risk measurement system for corporate credit, see “Corporate Credit”

above). The majority of the remainder was rated BB or B according to Citi’s

internal risk measurement system and methodology.

The private bank, which is part of ICG and primarily serves high-net-

worth individuals, had approximately $17 billion of loans in the emerging

markets as of December 31, 2015, representing approximately 25% of the

business’s total loans outstanding, unchanged from September 30, 2015 and

compared to $17 billion (27%) as of December 31, 2014. Private bank loans

are typically secured by liquid collateral or real estate and, consistent with the

rest of the ICG loan portfolio, the business has a well-established risk appetite

framework around its lending activities, including risk-based limits and

approval authorities and portfolio concentration boundaries.

Overall ICG net credit losses in the emerging markets were 0.1% of average

loans in the fourth quarter of 2015, compared to 0.0% and 0.4% in the third

quarter of 2015 and fourth quarter of 2014, respectively. The ratio of non-

accrual ICG loans to total loans in the emerging markets remained stable at

0.4% as of December 31, 2015.