Citibank 2015 Annual Report Download - page 102

Download and view the complete annual report

Please find page 102 of the 2015 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

|

|

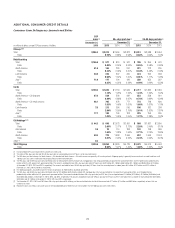

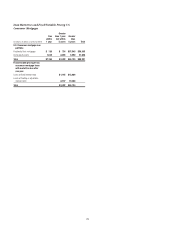

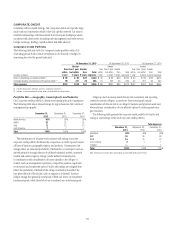

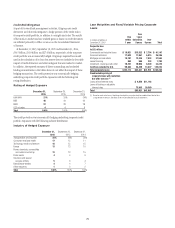

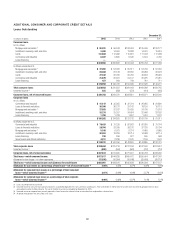

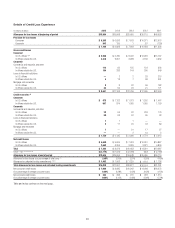

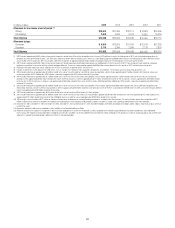

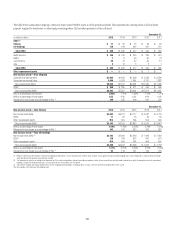

84

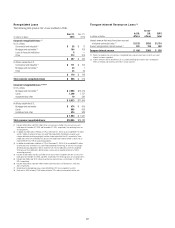

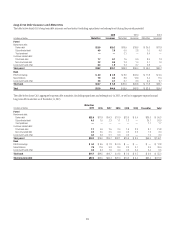

Non-Accrual Loans and Assets and Renegotiated Loans

There is a certain amount of overlap among non-accrual loans and

assets and renegotiated loans. The following summary provides a general

description of each category:

Non-Accrual Loans and Assets:

• Corporate and consumer (commercial market) non-accrual status

is based on the determination that payment of interest or principal

is doubtful.

• A corporate loan may be classified as non-accrual and still be performing

under the terms of the loan structure. Payments received on corporate

non-accrual loans are generally applied to loan principal and not

reflected as interest income. Approximately 45% and 40% of Citi’s

corporate non-accrual loans were performing at December 31, 2015 and

September 30, 2015, respectively.

• Consumer non-accrual status is generally based on aging, i.e., the

borrower has fallen behind on payments.

• Mortgage loans in regulated bank entities discharged through Chapter 7

bankruptcy, other than FHA insured loans, are classified as non-accrual.

Non-bank mortgage loans discharged through Chapter 7 bankruptcy are

classified as non-accrual at 90 days or more past due. In addition, home

equity loans in regulated bank entities are classified as non-accrual if the

related residential first mortgage loan is 90 days or more past due.

• North America Citi-branded cards and Citi retail services are not included

because, under industry standards, credit card loans accrue interest

until such loans are charged off, which typically occurs at 180 days

contractual delinquency.

Renegotiated Loans:

• Includes both corporate and consumer loans whose terms have been

modified in a troubled debt restructuring (TDR).

• Includes both accrual and non-accrual TDRs.