Citibank 2015 Annual Report Download - page 118

Download and view the complete annual report

Please find page 118 of the 2015 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

|

|

100

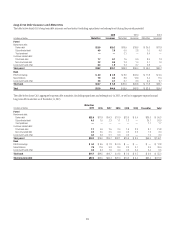

Interest Revenue/Expense and Net Interest Margin

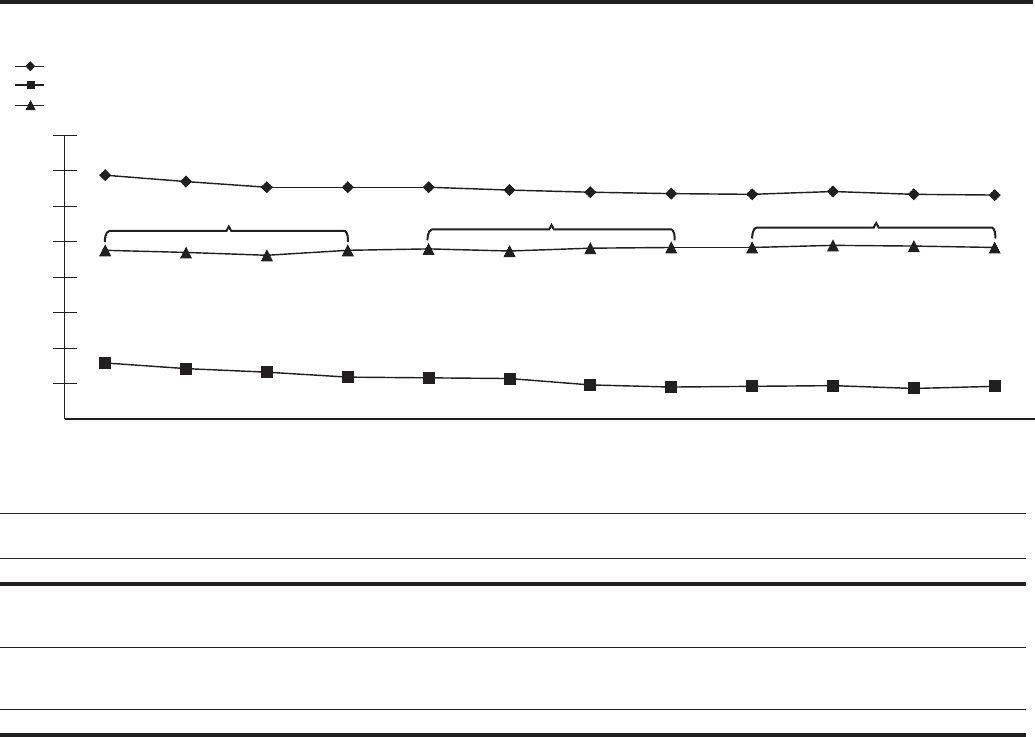

Average Rates

-

Interest Revenue, Interest Expense, and Net Interest Margin

Interest Revenue-Average Rate

Interest Expense-Average Rate

Net Interest Margin

0.96%

0.93%

0.97%

0.96%

0.95%

0.98%

1.07%

1.08%

1.09%

1.16%

1.21%

1.29%

2.88%

3.94% 3.85% 3.77% 3.77% 3.77% 3.73% 3.70% 3.68% 3.67% 3.71% 3.67% 3.66%

2.85% 2.81% 2.88% 2.90% 2.87% 2.91% 2.92% 2.92% 2.95% 2.94% 2.92%

1Q13 2Q13

2013: 2.85% 2014: 2.90% 2015: 2.93%

3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

In millions of dollars, except as otherwise noted 2015 2014 2013

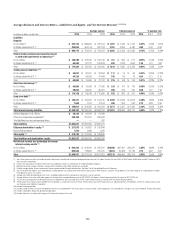

Change

2015 vs. 2014

Change

2014 vs. 2013

Interest revenue (1) $59,040 $62,180 $63,491 (5)% (2)%

Interest expense 11,921 13,690 16,177 (13) (15)

Net interest revenue (1)(2) $47,119 $48,490 $47,314 (3)% 2%

Interest revenue—average rate 3.68% 3.72% 3.83% (4)bps (11)bps

Interest expense—average rate 0.95 1.02 1.19 (7)bps (17)bps

Net interest margin 2.93 2.90 2.85 3 bps 5bps

Interest-rate benchmarks

Two-year U.S. Treasury note—average rate 0.69% 0.46% 0.31% 23 bps 15bps

10-year U.S. Treasury note—average rate 2.14 2.54 2.35 (40)bps 19bps

10-year vs. two-year spread 145bps 208bps 204bps

Note: All interest expense amounts include FDIC deposit insurance assessments.

(1) Net interest revenue includes the taxable equivalent adjustments related to the tax-exempt bond portfolio (based on the U.S. federal statutory tax rate of 35%) of $487 million, $498 million, and $521 million for 2015,

2014 and 2013, respectively.

(2) Excludes expenses associated with certain hybrid financial instruments, which are classified as Long-term debt and accounted for at fair value with changes recorded in Principal transactions.

Citi’s net interest margin (NIM) is calculated by dividing gross interest

revenue less gross interest expense by average interest earning assets. Citi’s

NIM was 2.92% in the fourth quarter of 2015, a slight decrease from 2.94%

in the third quarter of 2015, and improved to 2.93% for the full year 2015,

compared to 2.90% in 2014. The improvement in Citi’s NIM for the full

year 2015 was driven by trading NIM and the impact of lower cost of funds,

primarily declines in the cost of long-term debt, partially offset by lower loan

yields. Going into 2016, Citi’s NIM will reflect the sale of OneMain Financial,

which will be partially offset by the benefit of debt repurchases during 2015,

including in the fourth quarter of 2015. Accordingly, Citi currently expects a

decrease in its NIM in the first half of 2016.

As noted in the tables above, Citi’s interest expense includes the impact

of FDIC deposit insurance assessments. As part of the Dodd-Frank Act, the

FDIC is required to ensure that its deposit insurance fund reserve ratio

reaches 1.35% by September 30, 2020. In the fourth quarter of 2015, the

FDIC issued a notice of proposed rulemaking that would impose on insured

depository institutions with at least $10 billion in assets (large banks),

which includes Citibank, a surcharge of 4.5 basis points per annum until

the fund reaches the required ratio, which the FDIC estimates would take

approximately two years. Based on its current assessment base, Citi estimates

the net impact to Citibank would be approximately $500 million over the

two-year period. As part of its proposed rulemaking, the FDIC also discussed

an alternative to the surcharge proposal which would impose a one-time

assessment, similar to a shortfall assessment, on large banks in order to