Citibank 2015 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2015 Citibank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

|

|

68

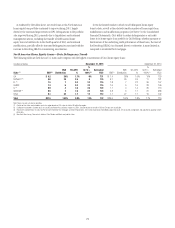

As of December 31, 2015, Citi’s North America residential first mortgage

portfolio contained approximately $2.4 billion of adjustable rate mortgages

that are currently required to make a payment consisting of only accrued

interest for the payment period, or an interest-only payment, compared to

$3.8 billion at December 31, 2014. This decline resulted primarily from

repayments and conversions to amortizing loans. Residential first mortgages

with this payment feature are primarily to high-credit-quality borrowers

who have on average significantly higher origination and refreshed FICO

scores than other loans in the residential first mortgage portfolio, and

have exhibited significantly lower 30+ delinquency rates as compared

with residential first mortgages without this payment feature. As such, Citi

does not believe the residential mortgage loans with this payment feature

represent substantially higher risk in the portfolio.

Citi does not offer option-adjustable rate mortgages/negative-amortizing

mortgage products to its customers. As a result, option-adjustable rate

mortgages/negative-amortizing mortgages represent an insignificant portion

of total balances, since they were acquired only incidentally as part of prior

portfolio and business purchases.

For additional information on Citi’s North America consumer mortgage

portfolio, see Note 15 to the Consolidated Financial Statements.

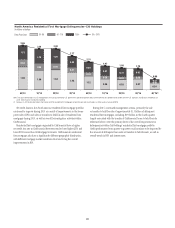

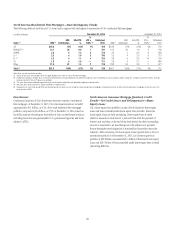

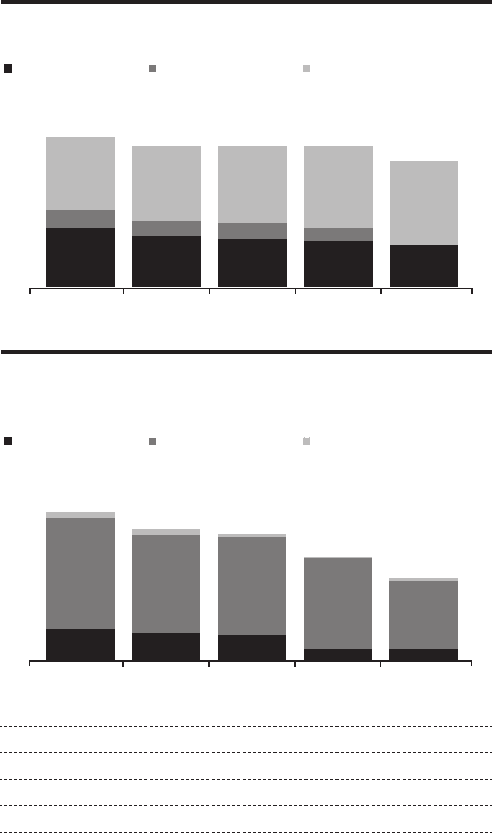

North America Consumer Mortgage Quarterly Credit

Trends—Net Credit Losses and Delinquencies—Residential

First Mortgages

The following charts detail the quarterly credit trends for Citi’s residential

first mortgage portfolio in North America.

4Q’15(1)

3Q’152Q’151Q’154Q’14

27

8

33

23

7

34

22

7

35

21

6

37

19

38

North America Residential First Mortgage—EOP Loans

In billions of dollars

Citi Holdings - CMI Citi Holdings - CFNA Citicorp

$68 $64 $64 $57

$64

4Q'153Q'152Q'151Q'154Q'14

26

91

5

22

81

5

21

80

3

9

75

1

9

56

3

North America Residential First Mortgage—

Net Credit Losses

In millions of dollars

Citi Holdings - CMI Citi Holdings - CFNA Citicorp

$122

$108 $104

$68

$85

Total NCL Rate 0.7% 0.6% 0.6% 0.5% 0.4%

Citi Holdings CMI 0.4% 0.3% 0.4% 0.2% 0.2%

Citi Holdings CFNA 4.6% 4.5% 4.7% 4.6% 4.0%

Citi Holdings Total 1.3% 1.3% 1.4% 1.2% 1.0%

Citicorp 0.05% 0.06% 0.03% 0.01% 0.03%

S&P/Case Shiller Home

Price Index(2) 4.4% 4.9% 4.8% 5.4% 5.6%(3)

Note: CMI refers to loans originated by CitiMortgage. CFNA refers to loans originated by CitiFinancial. Totals

may not sum due to rounding.

(1) Decrease in 4Q’15 EOP loans primarily reflects the transfer of CFNA residential first mortgages to

held-for-sale and classification as Other assets at year-end 2015. This transfer did not impact net

credit losses.

(2) Year-over-year change in the S&P/Case-Shiller U.S. National Home Price Index.

(3) Year-over-year change as of October 2015.