PNC Bank 2012 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2012 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

|

|

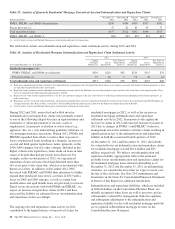

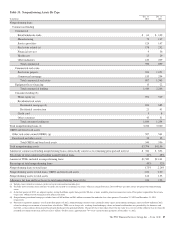

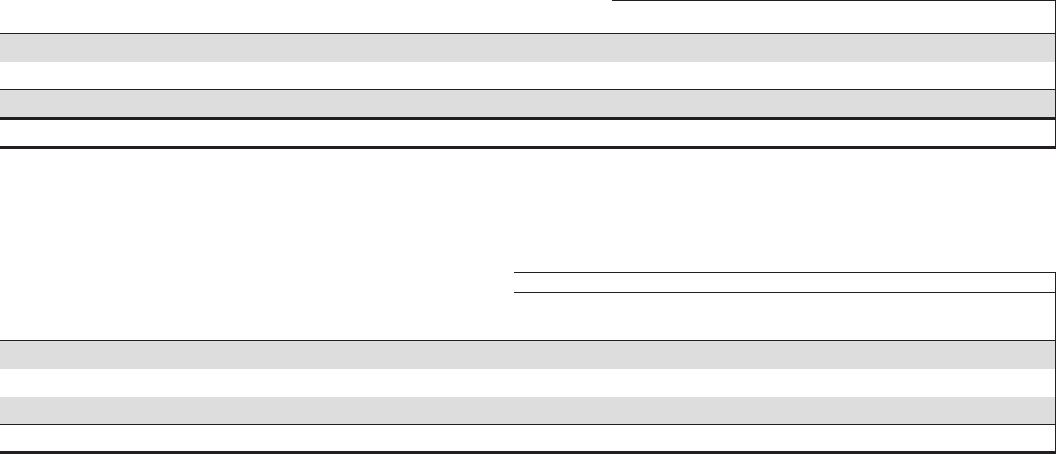

Table 29: Analysis of Quarterly Residential Mortgage Unresolved Asserted Indemnification and Repurchase Claims

Dollars in millions

December 31

2012

September 30

2012

June 30

2012

March 31

2012

December 31

2011

FNMA, FHLMC, and GNMA Securitizations $290 $430 $419 $337 $302

Private Investors (a) 47 82 83 69 73

Total unresolved claims $337 $512 $502 $406 $375

FNMA, FHLMC, and GNMA % 86% 84% 83% 83% 81%

(a) Activity relates to loans sold through Non-agency securitization and loan sale transactions.

The table below details our indemnification and repurchase claim settlement activity during 2012 and 2011.

Table 30: Analysis of Residential Mortgage Indemnification and Repurchase Claim Settlement Activity

2012 2011

Year ended December 31 – In millions

Unpaid

Principal

Balance (a)

Losses

Incurred (b)

Fair Value of

Repurchased

Loans (c)

Unpaid

Principal

Balance (a)

Losses

Incurred (b)

Fair Value of

Repurchased

Loans (c)

Residential mortgages (d):

FNMA, FHLMC, and GNMA securitizations $356 $210 $85 $220 $115 $74

Private investors (e) 75 46 5 76 48 14

Total indemnification and repurchase settlements $431 $256 $90 $296 $163 $88

(a) Represents unpaid principal balance of loans at the indemnification or repurchase date. Excluded from these balances are amounts associated with pooled settlement payments as loans

are typically not repurchased in these transactions.

(b) Represents both i) amounts paid for indemnification/settlement payments and ii) the difference between loan repurchase price and fair value of the loan at the repurchase date. These

losses are charged to the indemnification and repurchase liability.

(c) Represents fair value of loans repurchased only as we have no exposure to changes in the fair value of loans or underlying collateral when indemnification/settlement payments are

made to investors.

(d) Repurchase activity associated with insured loans, government-guaranteed loans, and loans repurchased through the exercise of our removal of account provision (ROAP) option are

excluded from this table. Refer to Note 3 in the Notes To Consolidated Financial Statements in Item 8 of this Report for further discussion of ROAPs.

(e) Activity relates to loans sold through Non-agency securitizations and loan sale transactions.

During 2012 and 2011, unresolved and settled investor

indemnification and repurchase claims were primarily related

to one of the following alleged breaches in representations and

warranties: (i) misrepresentation of income, assets or

employment, (ii) property evaluation or status issues (e.g.,

appraisal, title, etc.), (iii) underwriting guideline violations, or

(iv) mortgage insurance rescissions. During 2012, FNMA and

FHLMC expanded their efforts to reduce their exposure to

losses on purchased loans resulting in a dramatic increase in

second and third quarter repurchase claims, primarily on the

2006-2008 vintages, but also other vintages. Included in this

higher volume were repurchase claims made on loans in later

stages of default than had previously been observed. For

example, in the second quarter of 2012, we experienced

repurchase claims on loans which had defaulted more than

two years prior to the claim date, which was inconsistent with

historical activity. In addition, in December 2012, PNC

discussed with FHLMC and FNMA their intentions to further

expand their purchased loan review activities in 2013 with a

focus on 2004 and 2005 vintages, as well as certain loan

modifications and aged default loans not previously reviewed.

Based on our discussions with both FNMA and FHLMC, we

expect an increase in repurchase claims in 2013 and have

increased the liability for estimated losses on indemnification

and repurchase claims accordingly.

The ongoing elevated repurchase claim activity in 2012

contributed to the higher balance of unresolved claims for

residential mortgages in 2012, as well as the increase in

residential mortgage indemnification and repurchase

settlement activity in 2012. In response to the significant

increase in claims in 2012 and expected increase in claims in

2013 due to changes in FNMA’s and FHLMC’s behavior,

management revised its estimates of future claims resulting in

significant increases to the indemnification and repurchase

liability in both the second and fourth quarters of 2012.

At December 31, 2012 and December 31, 2011, the liability

for estimated losses on indemnification and repurchase claims

for residential mortgages totaled $614 million and $83

million, respectively. We believe our indemnification and

repurchase liability appropriately reflects the estimated

probable losses on indemnification and repurchase claims for

all residential mortgage loans sold and outstanding as of

December 31, 2012 and December 31, 2011. In making these

estimates, we consider the losses that we expect to incur over

the life of the sold loans. See Note 24 Commitments and

Guarantees in the Notes To Consolidated Financial Statements

in Item 8 of this Report for additional information.

Indemnification and repurchase liabilities, which are included

in Other liabilities on the Consolidated Balance Sheet, are

initially recognized when loans are sold to investors and are

subsequently evaluated by management. Initial recognition

and subsequent adjustments to the indemnification and

repurchase liability for the sold residential mortgage portfolio

are recognized in Residential mortgage revenue on the

Consolidated Income Statement.

80 The PNC Financial Services Group, Inc. – Form 10-K