PNC Bank 2012 Annual Report Download - page 200

Download and view the complete annual report

Please find page 200 of the 2012 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

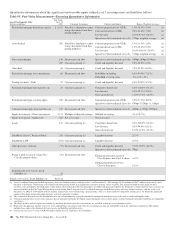

|

|

O

THER

F

INANCIAL

A

SSETS

A

CCOUNTED FOR AT

F

AIR

V

ALUE

ON A

N

ONRECURRING

B

ASIS

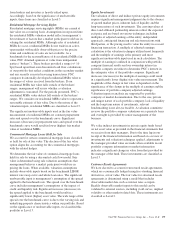

We may be required to measure certain other financial assets

at fair value on a nonrecurring basis. These adjustments to fair

value usually result from the application of lower-of-cost-or-

fair value accounting or write-downs of individual assets due

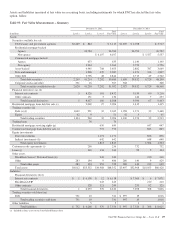

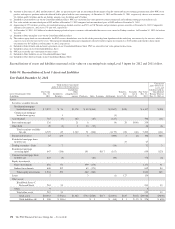

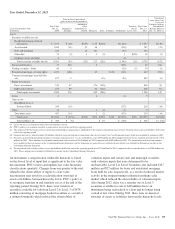

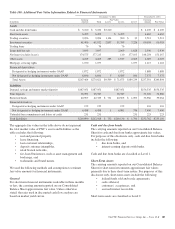

to impairment and are included in Table 96: Fair Value

Measurements – Nonrecurring and Table 97: Fair Value

Measurements – Nonrecurring Quantitative Information.

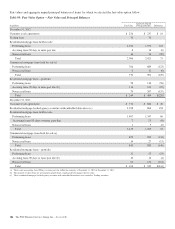

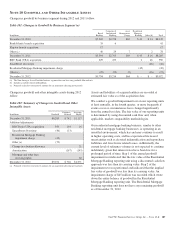

Nonaccrual Loans

The amounts below for nonaccrual loans represent the fair

value of those loans which have been adjusted due to

impairment. The impairment is primarily based on the

appraised value of the collateral or LGD percentage. The LGD

percentage is used to determine the weighted average loss

severity of the nonaccrual loans.

As part of the appraisal process, persons ordering or reviewing

appraisals are independent of the asset manager. Appraisals

must be provided by licensed or certified appraisers and

conform to the Uniform Standards of Professional Appraisal

Practice. For loans secured by commercial properties where

the underlying collateral is in excess of $250,000, appraisals

are obtained at least annually. In certain instances (e.g.,

physical changes in the property), a more recent appraisal is

obtained. Additionally, borrower ordered appraisals are not

permitted, and PNC ordered appraisals are regularly reviewed.

For loans secured by commercial properties where the

underlying collateral is $250,000 and less, there is no

requirement to obtain an appraisal. In instances where an

appraisal is not obtained, the collateral value is determined

consistent with external third-party appraisal standards by an

internal person independent of the asset manager. PNC has a

real estate valuation services group whose sole function is to

manage the real estate appraisal solicitation and evaluation

process for commercial loans. All third-party appraisals are

reviewed by this group, including consideration of comments/

questions on the appraisal by the reviewer, customer

relationship manager, credit officer, and underwriter. Upon

resolving these comments/questions through discussions with

the third-party appraiser, adjustments to the initial appraisal

may occur and be incorporated into the final issued appraisal

report.

If an appraisal is outdated due to changed project or market

conditions, or if the net book value is utilized, management

uses an LGD percentage which represents the exposure PNC

expects to lose in the event a borrower defaults on an

obligation. Accordingly, LGD, which represents the loss

severity, is a function of collateral recovery rates and loan-to-

value. Those rates are established based upon actual PNC loss

experience and external market data. In instances where we

have agreed to sell the property to a third party, the fair value

is based on the contractual sales price adjusted for costs to

sell. In these instances, the most significant unobservable

input is the appraised value or the sales price. The estimated

costs to sell are incremental direct costs to transact a sale such

as broker commissions, legal, closing costs and title transfer

fees. The costs must be essential to the sale and would not

have been incurred if the decision to sell had not been made.

The costs to sell are based on costs associated with our actual

sales of commercial and residential OREO and foreclosed

assets, which are assessed annually.

Loans Held for Sale

The amounts below for loans held for sale include the carrying

value of commercial mortgage loans which are intended to be

sold with servicing retained. The fair value of the commercial

mortgage loans is determined using discounted cash flows.

Significant observable market data includes the applicable

benchmark U.S. Treasury interest rates. These instruments are

classified within Level 3. Significant unobservable inputs

include a spread over the benchmark curve and the embedded

servicing value. Significant increases (decreases) to the spread

over the benchmark curve would result in a significantly lower

(higher) carrying value of the assets. Significant increases

(decreases) in the embedded servicing value would result in

significantly higher (lower) carrying value.

Loans held for sale also includes syndicated commercial loan

inventory. The fair value of the syndicated commercial loan

inventory is primarily determined based on prices provided by

a third-party vendor. The third-party vendor prices are based

upon dealer quotes. These instruments are classified within

Level 2. There were no loans held for sale categorized as

Level 2 at December 31, 2012.

Equity Investments

The amounts below for equity investments represent the

carrying value of Low Income Housing Tax Credit (LIHTC)

investments held for sale calculated using a discounted cash

flow model. The significant unobservable input is

management’s estimate of required market rate of return. The

market rate of return is based on comparison to recent LIHTC

sales in the market. Significant increases (decreases) in this

input would result in a significantly lower (higher) carrying

value of the investments.

Commercial Mortgage Servicing Rights

Commercial MSRs are periodically evaluated for impairment

and the amounts below reflect an impairment of two strata at

December 31, 2012 and three strata at December 31, 2011,

respectively. For purposes of impairment, the commercial

MSRs are stratified based on asset type, which characterizes

the predominant risk of the underlying financial asset. The fair

value of commercial MSRs is estimated by using a discounted

cash flow model incorporating unobservable inputs for

assumptions as to constant prepayment rates, discount rates

and other factors. Significant increases (decreases) in constant

prepayment rates and discount rates would result in

significantly lower (higher) commercial MSR value

determined based on current market conditions and

expectations.

The PNC Financial Services Group, Inc. – Form 10-K 181