PNC Bank 2012 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2012 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

|

|

(f) Nonperforming loans exclude certain government insured or guaranteed loans, loans held for sale, loans accounted for under the fair value option and purchased impaired loans.

(g) OREO excludes $380 million and $280 million at December 31, 2012 and December 31, 2011, respectively, related to residential real estate that was acquired by us upon foreclosure

of serviced loans because they are insured by the Federal Housing Administration (FHA) or guaranteed by the Department of Veterans Affairs (VA).

(h) The allowance for loan and lease losses includes impairment reserves attributable to purchased impaired loans. See Note 7 Allowances for Loan and Lease Losses and Unfunded Loan

Commitments and Letters of Credit in the Notes To Consolidated Financial Statements in Item 8 of this Report for additional information.

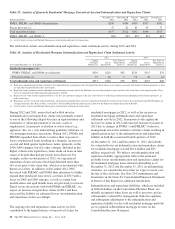

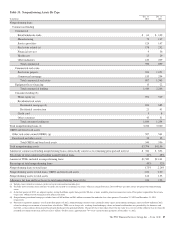

Table 34: OREO and Foreclosed Assets

In millions

Dec. 31

2012

Dec. 31

2011

Other real estate owned (OREO):

Residential properties $167 $191

Residential development properties 135 183

Commercial properties 205 187

Total OREO 507 561

Foreclosed and other assets 33 35

Total OREO and foreclosed assets $540 $596

Total OREO and foreclosed assets declined $56 million during

2012 from $596 million at December 31, 2011, to $540

million at December 31, 2012, which represents 14% of total

nonperforming assets. The decrease is primarily due to

increased sales activity and greater valuation losses offset in

part by an increase from the acquisition of RBC Bank (USA).

Of the $245 million added to OREO through the acquisition of

RBC Bank (USA), $109 million remained at December 31,

2012. As of December 31, 2012 and December 31, 2011, 31%

and 32%, respectively, of our OREO and foreclosed assets

were comprised of 1-4 family residential properties. Excluded

from OREO at December 31, 2012 and December 31, 2011,

respectively, was $380 million and $280 million of residential

real estate that was acquired by us upon foreclosure of

serviced loans because they are insured by the Federal

Housing Administration (FHA) or guaranteed by the

Department of Veterans Affairs (VA).

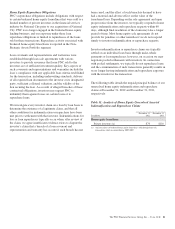

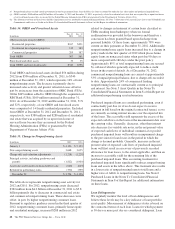

Table 35: Change in Nonperforming Assets

In millions 2012 2011

January 1 $ 4,156 $ 5,123

New nonperforming assets 3,648 3,625

Charge-offs and valuation adjustments (1,218) (1,220)

Principal activity, including paydowns and

payoffs (1,812) (1,960)

Asset sales and transfers to loans held for sale (610) (613)

Returned to performing status (370) (799)

December 31 $ 3,794 $ 4,156

The table above represents nonperforming asset activity for

2012 and 2011. For 2012, nonperforming assets decreased

$362 million from $4.2 billion at December 31, 2011 to $3.8

billion primarily due to decreases in commercial real estate

and commercial nonperforming loans. These decreases were

offset, in part, by higher nonperforming consumer loans.

Pursuant to regulatory guidance issued in the third quarter of

2012, nonperforming consumer loans, primarily home equity

and residential mortgage, increased $288 million in 2012

related to changes in treatment of certain loans classified as

TDRs resulting from bankruptcy where no formal

reaffirmation was provided by the borrower and therefore a

concession has been granted based upon discharge from

personal liability. Of these loans, approximately 78% were

current on their payments at December 31, 2012. Additionally,

nonperforming home equity loans increased due to a change in

policy made in the first quarter of 2012 which places home

equity loans on nonaccrual status when past due 90 days or

more compared with 180 days under the prior policy.

Approximately 85% of total nonperforming loans are secured

by collateral which is generally expected to reduce credit

losses in the event of default. As of December 31, 2012,

commercial nonperforming loans are carried at approximately

53% of unpaid principal balance, due to charge-offs recorded

to date. Approximately 24% of commercial lending

nonperforming loans are contractually current as to principal

and interest. See Note 5 Asset Quality in the Notes To

Consolidated Financial Statements in Item 8 of this Report for

additional nonperforming asset information.

Purchased impaired loans are considered performing, even if

contractually past due (or if we do not expect to receive

payment in full based on the original contractual terms), as we

are currently accreting interest income over the expected life

of the loans. The accretable yield represents the excess of the

expected cash flows on the loans at the measurement date over

the carrying value. Generally, decreases, other than interest

rate decreases for variable rate notes, in the net present value

of expected cash flows of individual commercial or pooled

purchased impaired loans will result in an impairment charge

to the provision for loan losses in the period in which the

change is deemed probable. Generally, increases in the net

present value of expected cash flows of purchased impaired

loans will first result in a recovery of previously recorded

allowance for loan losses, to the extent applicable, and then an

increase to accretable yield for the remaining life of the

purchased impaired loans. This accounting treatment for

purchased impaired loans significantly reduces nonperforming

loans and assets in the tables above. This treatment also results

in a lower ratio of nonperforming loans to total loans and a

higher ratio of ALLL to nonperforming loans. See Note 6

Purchased Loans in the Notes To Consolidated Financial

Statements in Item 8 of this Report for additional information

on these loans.

Loan Delinquencies

We regularly monitor the level of loan delinquencies and

believe these levels may be a key indicator of loan portfolio

asset quality. Measurement of delinquency status is based on

the contractual terms of each loan. Loans for which payment

is 30 days or more past due are considered delinquent. Loan

88 The PNC Financial Services Group, Inc. – Form 10-K