PNC Bank 2012 Annual Report Download - page 181

Download and view the complete annual report

Please find page 181 of the 2012 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

|

|

N

OTE

7A

LLOWANCES FOR

L

OAN AND

L

EASE

L

OSSES AND

U

NFUNDED

L

OAN

C

OMMITMENTS

AND

L

ETTERS OF

C

REDIT

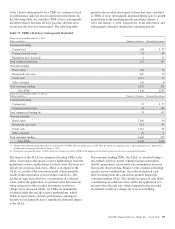

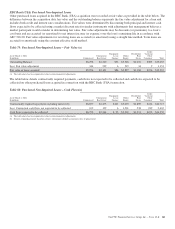

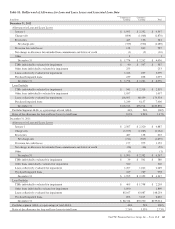

We maintain the ALLL and the Allowance for Unfunded Loan

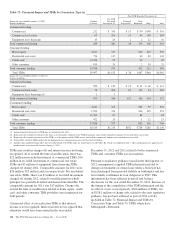

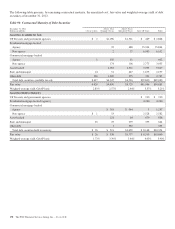

Commitments and Letters of Credit at levels that we believe to

be appropriate to absorb estimated probable credit losses

incurred in the portfolios as of the balance sheet date. We use

the two main portfolio segments – Commercial Lending and

Consumer Lending – and we develop and document the ALLL

under separate methodologies for each of these segments as

further discussed and presented below.

A

LLOWANCE FOR

L

OAN AND

L

EASE

L

OSSES

C

OMPONENTS

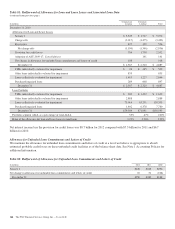

For all loans, except purchased impaired loans, the ALLL is

the sum of three components: (i) asset specific/individual

impaired reserves, (ii) quantitative (formulaic or pooled)

reserves, and (iii) qualitative (judgmental) reserves. See Note

6 Purchased Loans for additional ALLL information. The

reserve calculation and determination process is dependent on

the use of key assumptions. Key reserve assumptions and

estimation processes react to and are influenced by observed

changes in loan portfolio performance experience, the

financial strength of the borrower, and economic conditions.

Key reserve assumptions are periodically updated. During the

third quarter of 2012, PNC increased the amount of internally

observed data used in estimating the key commercial lending

assumptions of PD and LGD.

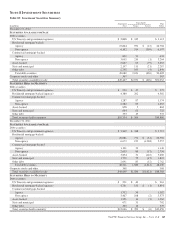

A

SSET

S

PECIFIC

/I

NDIVIDUAL

C

OMPONENT

Commercial nonperforming loans and all TDRs are

considered impaired and are evaluated for a specific reserve.

See Note 1 Accounting Policies for additional information.

C

OMMERCIAL

L

ENDING

Q

UANTITATIVE

C

OMPONENT

The estimates of the quantitative component of ALLL for

incurred losses within the commercial lending portfolio

segment are determined through statistical loss modeling

utilizing PD, LGD, and outstanding balance of the loan. Based

upon loan risk ratings we assign PDs and LGDs. Each of these

statistical parameters is determined based on internal

historical data and market data. PD is influenced by such

factors as liquidity, industry, obligor financial structure,

access to capital, and cash flow. LGD is influenced by

collateral type, original and/or updated LTV, and guarantees

by related parties.

C

ONSUMER

L

ENDING

Q

UANTITATIVE

C

OMPONENT

Quantitative estimates within the consumer lending portfolio

segment are calculated using a roll-rate model based on

statistical relationships, calculated from historical data that

estimate the movement of loan outstandings through the

various stages of delinquency and ultimately charge-off.

Qualitative Component

While our reserve methodologies strive to reflect all relevant

risk factors, there continues to be uncertainty associated with,

but not limited to, potential imprecision in the estimation

process due to the inherent time lag of obtaining information

and normal variations between estimates and actual outcomes.

We provide additional reserves that are designed to provide

coverage for losses attributable to such risks. The ALLL also

includes factors which may not be directly measured in the

determination of specific or pooled reserves. Such qualitative

factors include:

• Industry concentrations and conditions,

• Recent credit quality trends,

• Recent loss experience in particular portfolios,

• Recent macro-economic factors,

• Changes in risk selection and underwriting standards,

and

• Timing of available information, including the

performance of first lien positions.

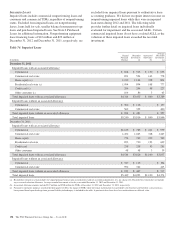

A

LLOWANCE FOR

RBC B

ANK

(USA) P

URCHASED

N

ON

-I

MPAIRED

L

OANS

ALLL for RBC Bank (USA) purchased non-impaired loans is

determined based upon the methodologies described above

compared to the remaining acquisition date fair value discount

that has yet to be accreted into interest income. After making

the comparison, an ALLL is recorded for the amount greater

than the discount, or no ALLL is recorded if the discount is

greater.

A

LLOWANCE FOR

P

URCHASED

I

MPAIRED

L

OANS

ALLL for purchased impaired loans is determined in

accordance with ASC 310-30 by comparing the net present

value of the cash flows expected to be collected to the

Recorded Investment for a given loan (or pool of loans). In

cases where the net present value of expected cash flows is

lower than Recorded Investment, ALLL is established. Cash

flows expected to be collected represent management’s best

estimate of the cash flows expected over the life of a loan (or

pool of loans). For large balance commercial loans, cash flows

are separately estimated and compared to the Recorded

Investment at the loan level. For smaller balance pooled loans,

cash flows are estimated using cash flow models and

compared at the risk pool level, which was defined at

acquisition based on risk characteristics of the loan. Our cash

flow models use loan data including, but not limited to,

delinquency status of the loan, updated borrower FICO credit

scores, geographic information, historical loss experience, and

updated LTVs, as well as estimates for unemployment rates,

home prices and other economic factors to determine

estimated cash flows.

162 The PNC Financial Services Group, Inc. – Form 10-K