PNC Bank 2012 Annual Report Download - page 98

Download and view the complete annual report

Please find page 98 of the 2012 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

|

|

Indemnification and repurchase claims are typically settled on

an individual loan basis through make-whole payments or

loan repurchases; however, on occasion we may negotiate

pooled settlements with investors. In connection with pooled

settlements, we typically do not repurchase loans and the

consummation of such transactions generally results in us no

longer having indemnification and repurchase exposure with

the investor in the transaction.

For the first and second-lien mortgage balances of unresolved

and settled claims contained in the tables below, a significant

amount of these claims were associated with sold loans

originated through correspondent lender and broker

origination channels. In certain instances when

indemnification or repurchase claims are settled for these

types of sold loans, we have recourse back to the

correspondent lenders, brokers and other third-parties (e.g.,

contract underwriting companies, closing agents, appraisers,

etc.). Depending on the underlying reason for the investor

claim, we determine our ability to pursue recourse with these

parties and file claims with them accordingly. Our historical

recourse recovery rate has been insignificant as our efforts

have been impacted by the inability of such parties to

reimburse us for their recourse obligations (e.g., their capital

availability or whether they remain in business) or factors that

limit our ability to pursue recourse from these parties (e.g.,

contractual loss caps, statutes of limitations).

Origination and sale of residential mortgages is an ongoing

business activity, and, accordingly, management continually

assesses the need to recognize indemnification and repurchase

liabilities pursuant to the associated investor sale agreements.

We establish indemnification and repurchase liabilities for

estimated losses on sold first and second-lien mortgages for

which indemnification is expected to be provided or for loans

that are expected to be repurchased. For the first and second-

lien mortgage sold portfolio, we have established an

indemnification and repurchase liability pursuant to investor

sale agreements based on claims made, demand patterns

observed to date and/or expected in the future, and our

estimate of future claims on a loan by loan basis. To estimate

the mortgage repurchase liability arising from breaches of

representations and warranties, we consider the following

factors: (i) borrower performance in our historically sold

portfolio (both actual and estimated future defaults), (ii) the

level of outstanding unresolved repurchase claims,

(iii) estimated probable future repurchase claims, considering

information about file requests, delinquent and liquidated

loans, resolved and unresolved mortgage insurance rescission

notices and our historical experience with claim rescissions,

(iv) the potential ability to cure the defects identified in the

repurchase claims (“rescission rate”), and (v) the estimated

severity of loss upon repurchase of the loan or collateral,

make-whole settlement, or indemnification.

See Note 24 Commitments and Guarantees in the Notes To

Consolidated Financial Statements in Item 8 of this Report for

additional information.

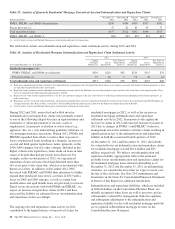

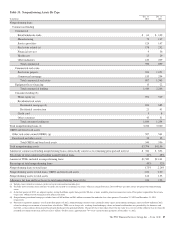

The following tables present the unpaid principal balance of repurchase claims by vintage and total unresolved repurchase claims

for the past five quarters.

Table 28: Analysis of Quarterly Residential Mortgage Repurchase Claims by Vintage

Dollars in millions

December 31

2012

September 30

2012

June 30

2012

March 31

2012

December 31

2011

2004 & Prior $ 11 $ 15 $ 31 $ 10 $ 11

2005 810191213

2006 23 30 56 41 28

2007 45 137 182 100 90

2008 723491718

2008 & Prior 94 215 337 180 160

2009 – 2012 38 52 42 33 29

Total $132 $267 $379 $213 $189

FNMA, FHLMC, and GNMA % 94% 87% 86% 88% 91%

The PNC Financial Services Group, Inc. – Form 10-K 79