PNC Bank 2012 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2012 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

|

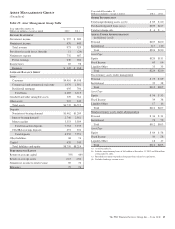

|

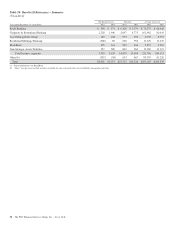

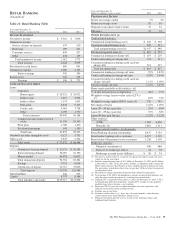

R

ETAIL

B

ANKING

(Unaudited)

Table 21: Retail Banking Table

Year ended December 31

Dollars in millions, except as noted 2012 2011

I

NCOME

S

TATEMENT

Net interest income $ 4,316 $ 3,806

Noninterest income

Service charges on deposits 547 510

Brokerage 189 201

Consumer services 838 927

Other 438 135

Total noninterest income 2,012 1,773

Total revenue 6,328 5,579

Provision for credit losses 800 891

Noninterest expense 4,586 4,103

Pretax earnings 942 585

Income taxes 346 214

Earnings $ 596 $ 371

A

VERAGE

B

ALANCE

S

HEET

Loans

Consumer

Home equity $ 28,321 $ 25,972

Indirect auto 5,467 3,094

Indirect other 1,174 1,491

Education 8,878 9,103

Credit cards 4,063 3,738

Other 2,039 1,750

Total consumer 49,942 45,148

Commercial and commercial real

estate 11,198 10,567

Floor plan 1,788 1,450

Residential mortgage 946 1,180

Total loans 63,874 58,345

Goodwill and other intangible assets 6,123 5,751

Other assets 2,576 2,352

Total assets $ 72,573 $ 66,448

Deposits

Noninterest-bearing demand $ 20,179 $ 18,183

Interest-bearing demand 28,007 22,196

Money market 46,578 41,002

Total transaction deposits 94,764 81,381

Savings 9,751 8,098

Certificates of deposit 25,715 33,006

Total deposits 130,230 122,485

Other liabilities 340 855

Capital 8,747 8,168

Total liabilities and equity $139,317 $131,508

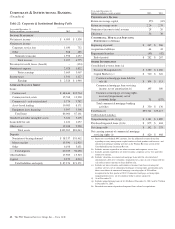

Year ended December 31

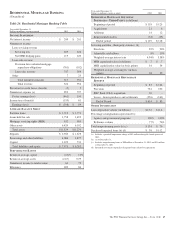

Dollars in millions, except as noted 2012 2011

P

ERFORMANCE

R

ATIOS

Return on average capital 7% 5%

Return on average assets .82 .56

Noninterest income to total revenue 32 32

Efficiency 72 74

O

THER

I

NFORMATION

(a)

Credit-related statistics:

Commercial nonperforming assets $ 245 $ 336

Consumer nonperforming assets 902 513

Total nonperforming assets (b) $1,147 $ 849

Purchased impaired loans (c) $ 819 $ 757

Commercial lending net charge-offs $ 119 $ 219

Credit card lending net charge-offs 174 211

Consumer lending (excluding credit card) net

charge-offs 521 427

Total net charge-offs $ 814 $ 857

Commercial lending net charge-off ratio .92% 1.82%

Credit card lending net charge-off ratio 4.28% 5.64%

Consumer lending (excluding credit card) net

charge-off ratio 1.11% 1.00%

Total net charge-off ratio 1.27% 1.47%

Home equity portfolio credit statistics: (d)

% of first lien positions at origination 42% 39%

Weighted-average loan-to-value ratios (LTVs)

(e) 81% 72%

Weighted-average updated FICO scores (f) 742 743

Net charge-off ratio 1.22% 1.09%

Loans 30 – 59 days past due .52% .58%

Loans 60 – 89 days past due .33% .38%

Loans 90 days past due (g) 1.22% 1.22%

Other statistics:

ATMs 7,282 6,806

Branches (h) 2,881 2,511

Customer-related statistics: (in thousands)

Retail Banking checking relationships 6,475 5,761

Retail online banking active customers 4,227 3,519

Retail online bill payment active customers 1,236 1,105

Brokerage statistics:

Financial consultants (i) 636 686

Full service brokerage offices 41 38

Brokerage account assets (billions) $ 38 $ 34

(a) Presented as of December 31, except for net charge-offs and net charge-off ratios,

which are for the year ended.

(b) Includes nonperforming loans of $1.1 billion at December 31, 2012 and $.8 billion

at December 31, 2011. In the first quarter of 2012, we adopted a policy stating that

Home equity loans past due 90 days or more would be placed on nonaccrual status.

The prior policy required that these loans be past due 180 days before being placed

on nonaccrual status.

(c) Recorded investment of purchased impaired loans related to acquisitions.

(d) Lien position, LTV, FICO and delinquency statistics are based upon balances and

other data that exclude the impact of accounting for acquired loans.

(e) Updated LTV is reported for December 31, 2012. For December 31, 2011, LTV is

based upon data from loan origination. Original LTV excludes certain acquired

portfolio loans where this data is not available.

(f) Represents FICO scores that are updated monthly for home equity lines and

quarterly for the home equity installment loans.

(g) Includes non-accrual loans.

(h) Excludes satellite offices (e.g., drive-ups, electronic branches, and retirement

centers) that provide limited products and/or services.

(i) Financial consultants provide services in full service brokerage offices and

traditional bank branches.

The PNC Financial Services Group, Inc. – Form 10-K 59