PNC Bank 2012 Annual Report Download - page 238

Download and view the complete annual report

Please find page 238 of the 2012 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

|

|

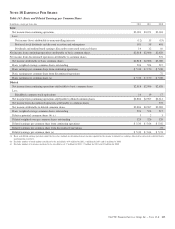

PNC files tax returns in most states and some non-U.S.

jurisdictions each year and is under continuous examination

by various state taxing authorities. With few exceptions, we

are no longer subject to state and local and non-U.S. income

tax examinations by taxing authorities for periods before

2003. For all open audits, any potential adjustments have been

considered in establishing our reserve for unrecognized tax

benefits as of December 31, 2012.

Our policy is to classify interest and penalties associated with

income taxes as income tax expense. For 2012, we had

expense of $4 million of gross interest and penalties

increasing income tax expense. The total accrued interest and

penalties at December 31, 2012 and December 31, 2011 was

$93 million and $81 million, respectively.

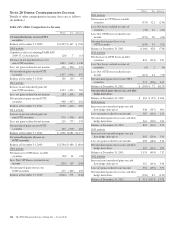

N

OTE

22 R

EGULATORY

M

ATTERS

We are subject to the regulations of certain federal, state, and

foreign agencies and undergo periodic examinations by such

regulatory authorities.

The ability to undertake new business initiatives (including

acquisitions), the access to and cost of funding for new

business initiatives, the ability to pay dividends, the ability to

repurchase shares or other capital instruments, the level of

deposit insurance costs, and the level and nature of regulatory

oversight depend, in large part, on a financial institution’s

capital strength. The minimum US regulatory capital ratios

under Basel I are 4% for Tier 1 risk-based, 8% for total risk-

based and 4% for leverage. To qualify as “well capitalized,”

regulators require banks to maintain capital ratios of at least

6% for Tier 1 risk-based, 10% for total risk-based and 5% for

leverage. To be “well capitalized,” a bank holding company

must maintain capital ratios of at least 6% Tier 1 risk-based

and 10% for total risk-based. At December 31, 2012 and

December 31, 2011, PNC and PNC Bank, N.A. met the “well

capitalized” capital ratio requirements based on US regulatory

capital ratio requirements under Basel I.

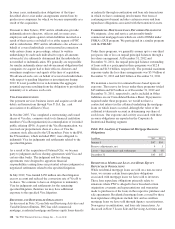

The following table sets forth regulatory capital ratios for

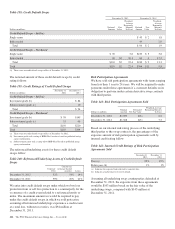

PNC and its bank subsidiary, PNC Bank, N.A.

Table 152: Regulatory Capital

Amount Ratios

December 31

Dollars in millions 2012 2011 2012 2011

Risk-based capital

Tier 1

PNC $30,226 $29,073 11.6% 12.6%

PNC Bank, N.A. 28,352 25,536 11.3 11.4

Total

PNC 38,234 36,548 14.7 15.8

PNC Bank, N.A. 35,756 32,322 14.2 14.4

Leverage

PNC 30,226 29,073 10.4 11.1

PNC Bank, N.A. 28,352 25,536 10.1 10.0

The principal source of parent company cash flow is the

dividends it receives from its subsidiary bank, which may be

impacted by the following:

• Capital needs,

• Laws and regulations,

• Corporate policies,

• Contractual restrictions, and

• Other factors.

Also, there are statutory and regulatory limitations on the

ability of national banks to pay dividends or make other

capital distributions. The amount available for dividend

payments to the parent company by PNC Bank, N.A. without

prior regulatory approval was approximately $1.5 billion at

December 31, 2012.

Under federal law, a bank subsidiary generally may not extend

credit to, or engage in other types of covered transactions

(including the purchase of assets) with, the parent company or

its non-bank subsidiaries on terms and under circumstances

that are not substantially the same as comparable transactions

with nonaffiliates. A bank subsidiary may not extend credit to,

or engage in a covered transaction with, the parent company

or a non-bank subsidiary if the aggregate amount of the bank’s

extensions of credit and other covered transactions with the

parent company or non-bank subsidiary exceeds 10% of the

capital stock and surplus of such bank subsidiary or the

aggregate amount of the bank’s extensions of credit and other

covered transactions with the parent company and all non-

bank subsidiaries exceeds 20% of the capital and surplus of

such bank subsidiary. Such extensions of credit, with limited

exceptions, must be at least fully collateralized in accordance

with specified collateralization thresholds, with the thresholds

varying based on the type of assets serving as collateral. In

certain circumstances, federal regulatory authorities may

impose more restrictive limitations.

Federal Reserve Board regulations require depository

institutions to maintain cash reserves with a Federal Reserve

Bank (FRB). At December 31, 2012, the balance outstanding

at the FRB was $3.5 billion.

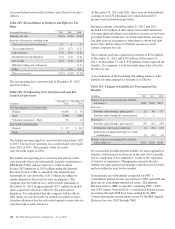

N

OTE

23 L

EGAL

P

ROCEEDINGS

We establish accruals for legal proceedings, including

litigation and regulatory and governmental investigations and

inquiries, when information related to the loss contingencies

represented by those matters indicates both that a loss is

probable and that the amount of loss can be reasonably

estimated. Any such accruals are adjusted thereafter as

appropriate to reflect changed circumstances. When we are

able to do so, we also determine estimates of possible losses

or ranges of possible losses, whether in excess of any related

accrued liability or where there is no accrued liability, for

disclosed legal proceedings (“Disclosed Matters,” which are

those matters disclosed in this Note 23). For Disclosed

Matters where we are able to estimate such possible losses or

The PNC Financial Services Group, Inc. – Form 10-K 219