PNC Bank 2012 Annual Report Download - page 191

Download and view the complete annual report

Please find page 191 of the 2012 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

|

|

nonaccrual loans, loans held for sale, commercial mortgage

servicing rights, equity investments and other assets.

We characterize active markets as those where transaction

volumes are sufficient to provide objective pricing

information, with reasonably narrow bid/ask spreads and

where dealer quotes received do not vary widely and are based

on current information. Inactive markets are typically

characterized by low transaction volumes, price quotations

that vary substantially among market participants or are not

based on current information, wide bid/ask spreads, a

significant increase in implied liquidity risk premiums, yields,

or performance indicators for observed transactions or quoted

prices compared to historical periods, a significant decline or

absence of a market for new issuance, or any combination of

the above factors. We also consider nonperformance risks

including credit risk as part of our valuation methodology for

all assets and liabilities measured at fair value.

Any models used to determine fair values or to validate dealer

quotes based on the descriptions below are subject to review

and independent testing as part of our model validation and

internal control testing processes. Our Model Risk

Management Committee reviews significant models on at

least an annual basis. In addition, we have teams, independent

of the traders, which verify marks and assumptions used for

valuations at each period end.

Assets and liabilities measured at fair value, by their nature,

result in a higher degree of financial statement volatility.

Assets and liabilities classified within Level 3 inherently

require the use of various assumptions, estimates and

judgments when measuring their fair value. As observable

market activity is commonly not available to use when

estimating the fair value of Level 3 assets and liabilities, we

must estimate fair value using various modeling techniques.

These techniques include the use of a variety of inputs/

assumptions including credit quality, liquidity, interest rates or

other relevant inputs across the entire population of our Level

3 assets and liabilities. Changes in the significant underlying

factors or assumptions (either an increase or a decrease) in any

of these areas underlying our estimates may result in a

significant increase/decrease in the Level 3 fair value

measurement of a particular asset and/or liability from period

to period.

F

INANCIAL

I

NSTRUMENTS

A

CCOUNTED

F

OR AT

F

AIR

V

ALUE

ON A

R

ECURRING

B

ASIS

Securities Available for Sale and Trading Securities

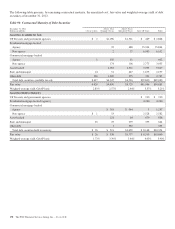

Securities accounted for at fair value include both the

available for sale and trading portfolios. We primarily use

prices obtained from pricing services, dealer quotes, or recent

trades to determine the fair value of securities. As of

December 31, 2012, 84% of the positions in these portfolios

were priced by using pricing services provided by third-party

vendors. The third-party vendors use a variety of methods

when pricing securities that incorporate relevant market data

to arrive at an estimate of what a buyer in the marketplace

would pay for a security under current market conditions. One

of the vendor’s prices are set with reference to market activity

for highly liquid assets such as U.S. Treasury and agency

securities and agency residential mortgage-backed securities,

and matrix pricing for other asset classes, such as commercial

mortgage and other asset-backed securities. Another vendor

primarily uses discounted cash flow pricing models

considering adjustments for spreads and prepayments for the

instruments we value using this service, such as non-agency

residential mortgage-backed securities, agency adjustable rate

mortgage securities, agency collateralized mortgage

obligations (CMOs), commercial mortgage-backed securities

and municipal bonds. The vendors we use provide pricing

services on a global basis and have quality management

processes in place to monitor the integrity of the valuation

inputs and the prices provided to users, including procedures

to consider and incorporate information received from pricing

service users who may challenge a price. We monitor and

validate the reliability of vendor pricing on an ongoing basis

through pricing methodology reviews, by performing detailed

reviews of the assumptions and inputs used by the vendor to

price individual securities, and through price validation

testing. Price validation testing is performed independent of

the risk-taking function and involves corroborating the prices

received from third-party vendors with prices from another

third-party source, by reviewing valuations of comparable

instruments, by comparison to internal valuations, or by

reference to recent sales of similar securities. Securities not

priced by one of our pricing vendors may be valued using a

dealer quote. Dealer quotes received are typically non-

binding. Securities priced using a dealer quote are subject to

corroboration either with another dealer quote, by comparison

to similar securities priced by either a third-party vendor or

another dealer, or through internal valuation in order to

validate that the quote is representative of the market. Security

prices are also validated through actual cash settlement upon

sale of a security.

A cross-functional team comprised of representatives from

Asset & Liability Management, Finance, and Market Risk

Management oversees the governance of the processes and

methodologies used to estimate the fair value of securities and

the price validation testing that is performed. This

management team reviews pricing sources and trends and the

results of validation testing.

172 The PNC Financial Services Group, Inc. – Form 10-K