PNC Bank 2012 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2012 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

|

|

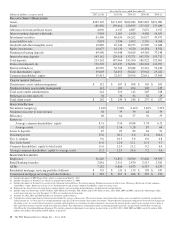

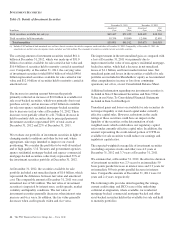

Residential mortgage revenue decreased to $284 million in

2012 from $713 million in 2011. This decrease of $429

million, or 60 percent, was largely due to a higher provision

for residential mortgage repurchase obligations of $761

million in 2012 compared with $102 million in 2011, partially

offset by an increase in loan sales revenue driven by higher

loan origination volume.

The higher provision for residential mortgage repurchase

obligations in 2012 reflected expected further elevated levels

of repurchase demands primarily as a result of changes in

behaviors and demand patterns of two government-sponsored

enterprises, FHLMC and FNMA, for loans sold into agency

securitizations. The recorded liability for residential mortgage

indemnification and repurchase claims was $614 million at

December 31, 2012. See the Recourse And Repurchase

Obligations section of this Item 7 for more detail.

Service charges on deposits grew to $573 million in 2012

compared with $534 million in 2011. This increase reflected

continued success in growing customers, including through

the RBC Bank (USA) acquisition.

Net gains on sales of securities totaled $204 million for 2012

and $249 million for 2011. The net credit component of other-

than-temporary impairment (OTTI) of securities recognized in

earnings was $111 million in 2012 compared with $152

million for 2011.

Other noninterest income increased by $.4 billion, or 38

percent, to $1.5 billion for 2012 compared with $1.1 billion

for 2011. This increase was primarily due to $267 million of

gains on sales of approximately 9 million Visa Class B

common shares during the third and fourth quarters of 2012,

as well as higher revenue associated with private equity

investments. We continue to hold approximately 14.4 million

Visa Class B common shares with an estimated fair value of

approximately $916 million as of December 31, 2012. Our

recorded investment in these remaining shares was

approximately $251 million at December 31, 2012.

Other noninterest income typically fluctuates from period to

period depending on the nature and magnitude of transactions

completed. Further details regarding our trading activities are

included in the Market Risk Management – Trading Risk

portion of the Risk Management section of this Item 7. Further

details regarding private and other equity investments are

included in the Market Risk Management – Equity And Other

Investment Risk portion of the Risk Management section of

this Item 7, and further details regarding gains or losses

related to our equity investment in BlackRock are included in

the Business Segments Review section of this Item 7.

For 2013, we currently expect both noninterest income and

total revenue to increase compared with 2012.

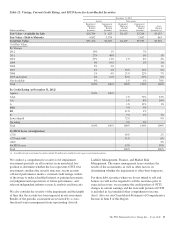

P

RODUCT

R

EVENUE

In addition to credit and deposit products for commercial

customers, Corporate & Institutional Banking offers other

services, including treasury management, capital markets-

related products and services, and commercial mortgage

banking activities for customers of all our business segments.

A portion of the revenue and expense related to these products

is reflected in the Corporate & Institutional Banking segment

results and the remainder is reflected in the results of other

businesses. The Other Information section in the Corporate &

Institutional Banking table in the Business Segments Review

section of this Item 7 includes the consolidated revenue to

PNC for these services. A discussion of the consolidated

revenue from these services follows.

Treasury management revenue, comprised of fees and net

interest income from customer deposit balances, totaled $1.4

billion for 2012 and $1.3 billion for 2011. Higher deposit

balances along with strong growth in commercial card,

lockbox and traditional products, including DDA, wire and

ACH, led to the favorable results.

Revenue from capital markets-related products and services

totaled $710 million in 2012 compared with $622 million in

2011. The comparison reflects higher merger and acquisition

advisory fees and strong customer driven capital markets

activity.

Commercial mortgage banking activities include revenue

derived from commercial mortgage servicing (including net

interest income and noninterest income from loan servicing

and ancillary services, net of commercial mortgage servicing

rights amortization, and commercial mortgage servicing rights

valuations net of economic hedge), and revenue derived from

commercial mortgage loans intended for sale and related

hedges (including loan origination fees, net interest income,

valuation adjustments and gains or losses on sales).

Commercial mortgage banking activities resulted in revenue

of $330 million in 2012 compared with $136 million in 2011.

The increase in the comparison was mainly due to the impact

of recoveries on commercial mortgage servicing rights in

2012 compared to impairments taken during 2011.

40 The PNC Financial Services Group, Inc. – Form 10-K