PNC Bank 2012 Annual Report Download - page 164

Download and view the complete annual report

Please find page 164 of the 2012 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

|

|

N

OTE

4L

OANS AND

C

OMMITMENTS TO

E

XTEND

C

REDIT

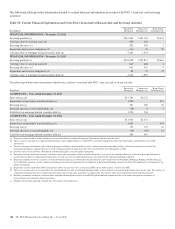

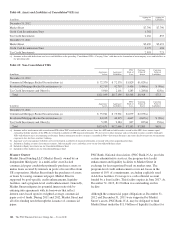

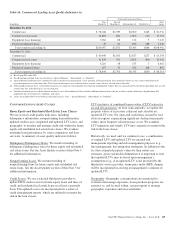

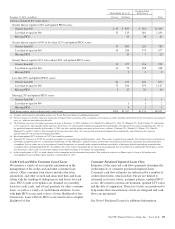

Loans outstanding were as follows:

Table 62: Loans Outstanding

In millions

December 31

2012

December 31

2011

Commercial lending

Commercial $ 83,040 $ 65,694

Commercial real estate 18,655 16,204

Equipment lease financing 7,247 6,416

Total Commercial Lending 108,942 88,314

Consumer lending

Home equity 35,920 33,089

Residential real estate 15,240 14,469

Credit card 4,303 3,976

Other consumer 21,451 19,166

Total consumer lending 76,914 70,700

Total loans (a) (b) $185,856 $159,014

(a) Net of unearned income, net deferred loan fees, unamortized discounts and

premiums, and purchase discounts and premiums totaling $2.7 billion and $2.3

billion at December 31, 2012 and December 31, 2011, respectively.

(b) Future accretable yield related to purchased impaired loans is not included in loans

outstanding.

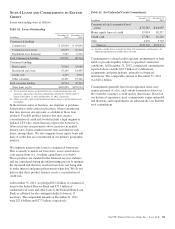

In the normal course of business, we originate or purchase

loan products with contractual features, when concentrated,

that may increase our exposure as a holder of those loan

products. Possible product features that may create a

concentration of credit risk would include a high original or

updated LTV ratio, terms that may expose the borrower to

future increases in repayments above increases in market

interest rates, below-market interest rates and interest-only

loans, among others. We also originate home equity loans and

lines of credit that are concentrated in our primary geographic

markets.

We originate interest-only loans to commercial borrowers.

This is usually to match our borrowers’ asset conversion to

cash expectations (i.e., working capital lines, revolvers).

These products are standard in the financial services industry

and are considered during the underwriting process to mitigate

the increased risk that may result in borrowers not being able

to make interest and principal payments when due. We do not

believe that these product features create a concentration of

credit risk.

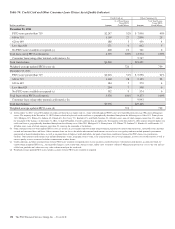

At December 31, 2012, we pledged $23.2 billion of commercial

loans to the Federal Reserve Bank and $37.3 billion of

residential real estate and other loans to the Federal Home Loan

Bank as collateral for the contingent ability to borrow, if

necessary. The comparable amounts at December 31, 2011

were $21.8 billion and $27.7 billion, respectively.

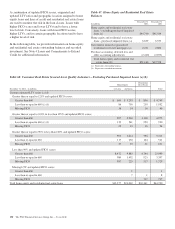

Table 63: Net Unfunded Credit Commitments

In millions

December 31

2012

December 31

2011

Commercial and commercial real

estate $ 78,703 $ 64,955

Home equity lines of credit 19,814 18,317

Credit card 17,381 16,216

Other 4,694 3,783

Total (a) $120,592 $103,271

(a) Excludes standby letters of credit. See Note 24 Commitments and Guarantees for

additional information on standby letters of credit.

Commitments to extend credit represent arrangements to lend

funds or provide liquidity subject to specified contractual

conditions. At December 31, 2012, commercial commitments

reported above exclude $22.5 billion of syndications,

assignments and participations, primarily to financial

institutions. The comparable amount at December 31, 2011

was $20.2 billion.

Commitments generally have fixed expiration dates, may

require payment of a fee, and contain termination clauses in

the event the customer’s credit quality deteriorates. Based on

our historical experience, most commitments expire unfunded,

and therefore cash requirements are substantially less than the

total commitment.

The PNC Financial Services Group, Inc. – Form 10-K 145