PNC Bank 2012 Annual Report Download - page 193

Download and view the complete annual report

Please find page 193 of the 2012 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

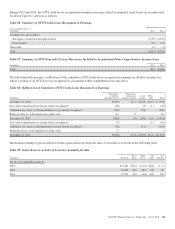

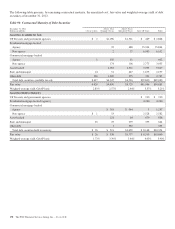

|

|

residential mortgage loan commitment asset (liability) result

when the probability of funding increases (decreases) and

when the embedded servicing value increases (decreases).

The fair value of commercial mortgage loan commitment

assets and liabilities as of December 31, 2012 are included in

the Insignificant Level 3 assets, net of liabilities line item in

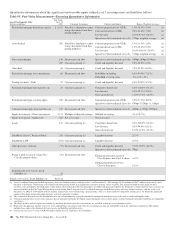

Table 95: Fair Value Measurement – Recurring Quantitative

Information in this Note 9. Significant unobservable inputs for

commercial mortgage loan commitments include spread over

the benchmark U.S. Treasury interest rate and the embedded

servicing value. The spread over the benchmark curve reflects

management assumptions regarding credit and liquidity risks.

Embedded servicing value reflects the estimated value for

retaining the right to service the underlying loan once it is

sold. Significant increases (decreases) in the fair value of

commercial mortgage loan commitments result when the

spread over the benchmark curve decreases (increases) or the

embedded servicing value increases (decreases).

The fair value of interest rate option assets and liabilities as of

December 31, 2012 are included in the Insignificant Level 3

assets, net of liabilities line item in Table 95: Fair Value

Measurement – Recurring Quantitative Information in this

Note 9. The significant unobservable input used in the fair

value measurement of the interest rate options is expected

interest rate volatility. Significant increases (decreases) in

interest rate volatility would result in a significantly higher

(lower) fair value measurement.

The fair value of risk participation agreement assets and

liabilities as of December 31, 2012 are included in the

Insignificant Level 3 assets, net of liabilities line item in Table

95: Fair Value Measurement – Recurring Quantitative

Information in this Note 9. The significant unobservable

inputs used in the fair value measurement of risk participation

agreements are probability of default and loss severity.

Significant increases (decreases) in probability of default and

loss severity would result in a significantly higher (lower) fair

value measurement.

Significant unobservable inputs for the other contracts for

derivative liabilities include credit and liquidity discount and

spread over the benchmark curve that are deemed

representative of current market conditions. Significant

increases (decreases) in these assumptions would result in

significantly lower (higher) fair value measurement.

In connection with the sales of certain Visa Class B common

shares in 2012, we entered into swap agreements with the

purchaser of the shares to account for future changes in the

value of the Class B common shares resulting from changes in

the settlement of certain specified litigation and its effect on

the conversion rate of Class B common shares into Visa

Class A common shares and to make payments calculated by

reference to the market price of the Class A common shares.

At December 31, 2012, the estimated fair values of the swap

liabilities are classified as Level 3 instruments and included in

Table 95: Fair Value Measurement – Recurring Quantitative

Information in this Note 9. The fair values of the swap

agreements are determined using a discounted cash flow

methodology. The significant unobservable inputs to the

valuations are estimated changes in the conversion rate of the

Class B shares into Class A shares and the estimated future

price of the Class A shares. A decrease in the conversion rate

will have a negative impact on the fair value of the swaps and

vice versa. Independent of changes in the conversion rate, an

increase in the future Class A share price will have a negative

impact on the fair value of the swaps and vice versa, through

its impact on periodic payments due to the counterparty until

the maturity dates of the swaps.

The fair values of our derivatives are adjusted for

nonperformance risk through the calculation of our Credit

Valuation Adjustment (CVA). Our CVA is computed using

new loan pricing and considers externally available bond

spreads, in conjunction with internal historical recovery

observations.

Residential Mortgage Loans Held for Sale

We account for certain residential mortgage loans originated

for sale at fair value on a recurring basis. We have elected to

account for certain RBC Bank (USA) residential mortgage

loans held for sale at fair value. The election of the fair value

option aligns the accounting for the residential mortgages with

the related hedges. Additionally, with the exception of

repurchased FHA insured loans which are accounted for at

amortized cost, we have elected to account for loans

repurchased due to breaches of representations and warranties

at fair value.

Residential mortgage loans are valued based on quoted market

prices, where available, prices for other traded mortgage loans

with similar characteristics, and purchase commitments and

bid information received from market participants. These

loans are regularly traded in active markets and observable

pricing information is available from market participants. The

prices are adjusted as necessary to include the embedded

servicing value in the loans and to take into consideration the

specific characteristics of certain loans that are priced based

on the pricing of similar loans. These adjustments represent

unobservable inputs to the valuation but are not considered

significant given the relative insensitivity of the value to

changes in these inputs to the fair value of the loans.

Accordingly, the majority of residential mortgage loans held

for sale are classified as Level 2. This category also includes

repurchased and temporarily unsalable residential mortgage

loans. These loans are repurchased due to a breach of

representations and warranties in the loan sales agreement and

typically occur after the loan is in default. The temporarily

unsalable loans have an origination defect that makes them

currently unable to be sold into the performing loan sales

market. Because transaction details regarding sales of this type

of loan are often unavailable, unobservable bid information

174 The PNC Financial Services Group, Inc. – Form 10-K