PNC Bank 2012 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2012 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

|

|

K

EY

F

ACTORS

A

FFECTING

F

INANCIAL

P

ERFORMANCE

Our financial performance is substantially affected by a

number of external factors outside of our control, including

the following:

• General economic conditions, including the

continuity, speed and stamina of the moderate

economic recovery in general and on our customers

in particular,

• The level of, and direction, timing and magnitude of

movement in, interest rates and the shape of the

interest rate yield curve,

• The functioning and other performance of, and

availability of liquidity in, the capital and other

financial markets,

• Loan demand, utilization of credit commitments and

standby letters of credit, and asset quality,

• Customer demand for non-loan products and

services,

• Changes in the competitive and regulatory landscape

and in counterparty creditworthiness and

performance as the financial services industry

restructures in the current environment,

• The impact of the extensive reforms enacted in the

Dodd-Frank legislation and other legislative,

regulatory and administrative initiatives, including

those outlined elsewhere in this Report, and

• The impact of market credit spreads on asset

valuations.

In addition, our success will depend upon, among other things:

• Further success in growing profitability through the

acquisition and retention of customers,

• Continued development of the geographic markets

related to our recent acquisitions, including full

deployment of our product offerings into our

Southeast markets,

• Revenue growth and our ability to provide innovative

and valued products to our customers,

• Our ability to utilize technology to develop and

deliver products and services to our customers,

• Our ability to manage and implement strategic

business objectives within the changing regulatory

environment,

• A sustained focus on expense management,

• Managing the non-strategic assets portfolio and

impaired assets,

• Improving our overall asset quality,

• Continuing to maintain and grow our deposit base as

a low-cost funding source,

• Prudent risk and capital management related to our

efforts to manage risk in keeping with a moderate

risk philosophy, and to meet evolving regulatory

capital standards,

• Actions we take within the capital and other financial

markets,

• The impact of legal and regulatory-related

contingencies, and

• The appropriateness of reserves needed for critical

estimates and related contingencies.

For additional information, please see Risk Factors in Item 1A

of this Report and the Cautionary Statement Regarding

Forward-Looking Information section in this Item 7.

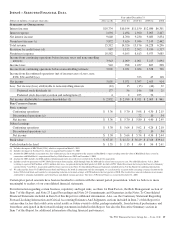

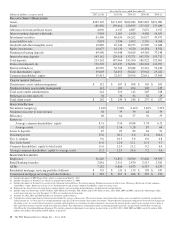

Table 1: Summary Financial Results

Year ended December 31 2012 2011

Net income (millions) $3,001 $3,071

Diluted earnings per common share

from net income $ 5.30 $ 5.64

Return from net income on:

Average common shareholders’

equity 8.31% 9.56%

Average assets 1.02% 1.16%

I

NCOME

S

TATEMENT

H

IGHLIGHTS

Our performance in 2012 included the following:

• Net income for 2012 of $3.0 billion decreased 2

percent compared to 2011. Revenue growth of 8

percent and a decline in the provision for credit

losses were more than offset by a 16 percent increase

in noninterest expense in 2012 compared with 2011.

Further detail is included below and in the

Consolidated Income Statement Review section of

this Item 7.

• Net interest income of $9.6 billion for 2012 increased

11 percent compared with 2011 driven by the impact

of the RBC Bank (USA) acquisition, organic loan

growth and lower funding costs.

• Noninterest income of $5.9 billion for 2012 increased

$.2 billion compared to 2011. The increase was

primarily driven by higher residential mortgage loans

sales revenue related to an increase in loan

origination volume, gains on sales of Visa Class B

common shares and higher corporate service fees,

largely offset by higher provision for residential

mortgage repurchase obligations.

• The provision for credit losses decreased to $1.0

billion for 2012 compared to $1.2 billion for 2011.

The decline in the comparison was driven by overall

credit quality improvement.

• Noninterest expense of $10.6 billion for 2012

increased $1.5 billion compared with 2011 primarily

driven by operating expense for the RBC Bank

(USA) acquisition, higher integration costs, increased

noncash charges related to redemption of trust

preferred securities and a charge for residential

mortgage banking goodwill impairment, partially

offset by the impact from higher residential mortgage

foreclosure-related expenses in 2011.

The PNC Financial Services Group, Inc. – Form 10-K 35