PNC Bank 2012 Annual Report Download - page 166

Download and view the complete annual report

Please find page 166 of the 2012 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

|

|

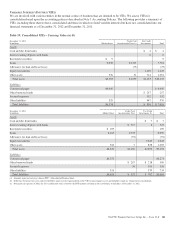

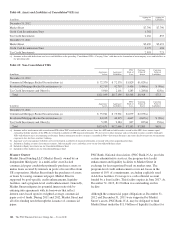

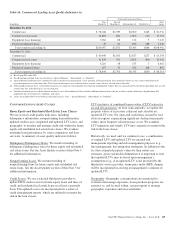

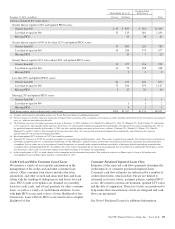

Table 65: Nonperforming Assets

Dollars in millions

December 31

2012

December 31

2011

Nonperforming loans

Commercial lending

Commercial $ 590 $ 899

Commercial real estate 807 1,345

Equipment lease financing 13 22

Total commercial lending 1,410 2,266

Consumer lending (a)

Home equity (b) 951 529

Residential real estate (c) 845 726

Credit card 58

Other consumer 43 31

Total consumer lending (d) 1,844 1,294

Total nonperforming loans (e) 3,254 3,560

OREO and foreclosed assets

Other real estate owned (OREO) (f) 507 561

Foreclosed and other assets 33 35

Total OREO and foreclosed assets 540 596

Total nonperforming assets $3,794 $4,156

Nonperforming loans to total loans 1.75% 2.24%

Nonperforming assets to total loans, OREO and foreclosed assets 2.04 2.60

Nonperforming assets to total assets 1.24 1.53

Interest on nonperforming loans

Computed on original terms $ 212 $ 278

Recognized prior to nonperforming status 30 47

(a) Excludes most consumer loans and lines of credit, not secured by residential real estate, which are charged off after 120 to 180 days past due and are not placed on nonperforming

status.

(b) In the first quarter of 2012, we adopted a policy stating that Home equity loans past due 90 days or more would be placed on nonaccrual status. Prior policy required that these loans

be past due 180 days before being placed on nonaccrual status.

(c) Nonperforming residential real estate excludes loans of $69 million and $61 million accounted for under the fair value option as of December 31, 2012 and December 31, 2011,

respectively.

(d) Pursuant to regulatory guidance issued in the third quarter of 2012, nonperforming consumer loans, primarily home equity and residential mortgage, increased $288 million in 2012

related to changes in treatment of certain loans classified as TDRs, net of charge-offs, resulting from bankruptcy where no formal reaffirmation was provided by the borrower and

therefore a concession has been granted based upon discharge from personal liability. Charge-offs have been taken where the fair value less costs to sell the collateral was less than the

recorded investment of the loan and were $128.1 million. Of these loans, approximately 78% were current on their payments at December 31, 2012.

(e) Nonperforming loans exclude certain government insured or guaranteed loans, loans held for sale, loans accounted for under the fair value option and purchased impaired loans.

(f) OREO excludes $380 million and $280 million at December 31, 2012 and December 31, 2011, respectively, related to residential real estate that was acquired by us upon foreclosure

of serviced loans because they are insured by the Federal Housing Administration (FHA) or guaranteed by the Department of Veterans Affairs (VA).

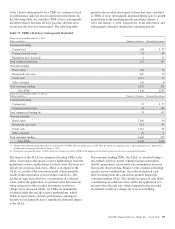

Nonperforming loans also include loans whose terms have

been restructured in a manner that grants a concession to a

borrower experiencing financial difficulties. In accordance

with applicable accounting guidance, these loans are

considered TDRs. See Note 1 Accounting Policies and the

TDR section of this Note 5 for additional information. For the

year ended December 31, 2012, $3.1 billion of loans held for

sale, loans accounted for under the fair value option, pooled

purchased impaired loans, as well as certain consumer

government insured or guaranteed loans which were evaluated

for TDR consideration, are not classified as TDRs. The

comparable amount for the year ended December 31, 2011

was $2.7 billion.

Total nonperforming loans in the Nonperforming Assets table

above include TDRs of $1.6 billion at December 31, 2012 and

$1.1 billion at December 31, 2011. TDRs returned to

performing (accruing) status totaled $1.0 billion and

$.8 billion at December 31, 2012 and December 31, 2011,

respectively, and are excluded from nonperforming loans.

These loans have demonstrated a period of at least six months

of consecutive performance under the restructured terms. At

December 31, 2012 and December 31, 2011, remaining

commitments to lend additional funds to debtors in a

commercial or consumer TDR were immaterial.

The PNC Financial Services Group, Inc. – Form 10-K 147